GIC Re-Unique insurance play?

GIC is India’s premier reinsurance company, a PSU enjoying 60% market share in India’s reinsurance market in FY17 (up from 45% in FY16 and 43% In FY15) and underwrote business from 162 countries. 95% of premiums are earned from the non-life space primarily in fire, motor, health and agriculture reinsurance. As per IRDA mandate, it is mandatory for insurance companies in India to cede a minimum of 5% of their risks to GIC (this has come down from 15% in FY13 to 5% now) and GIC also has a right of first refusal when it comes to Indian insurance companies seeking reinsurance.

As quoted in ICICI Lombard’s DRHP-“Additionally, under the IRDAI’s regulations, GIC Re, which is the only Indian re-insurer with the minimum credit rating required to gain this preferential status, has a right of first offer for all reinsurance ceded by an Indian non-life insurer. Hence, we may not have control over the amount of reinsurance we cede to GIC Re.” (GIC’s current credit rating is A-, they would need to work to improve this since foreign markets would likely require a rating of A or above to be competitive)

These regulations thus becomes a source of competitive advantage for GIC.

The Indian general insurance industry is underpenetrated and accounts for only 0.8% of GDP with an industry size of Rs 1.28 lakh crores. This is slated to grow at rates of 15%+ for the next few years.

The reinsurance market size was estimated at Rs 38800 crores in FY17 and is expected to reach Rs 70000 crores by 2022.(Going by H1FY18 numbers it is going to grow even faster than this)

Key success factor for the business- Warren Buffett puts it best-“An insurance business has value if its cost of float over time is less than the cost the company would otherwise incur to obtain funds. But the business is a lemon if its cost of float is higher than market rates for money."

How does GIC do on this test?

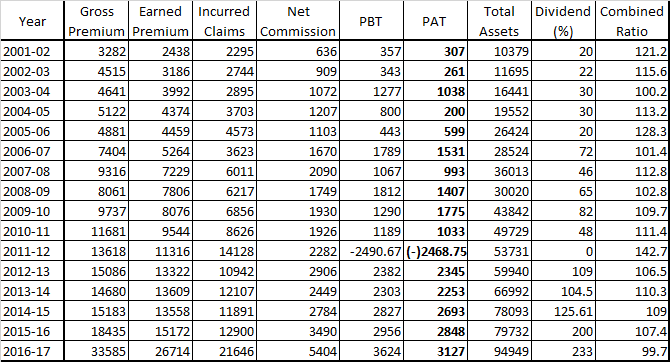

GIC had combined ratios of 100.16%,107.03% and 108.86% in FY17,FY16 and FY15 respectively.This has since come down further to 99.4% in H1FY18 thus meaning GIC has now achieved underwriting profits.

Underwriting Analysis:

Combined ratio upto FY16 suggests that cost of funds was 7-8%(this is in line with money market rates).However, since last 18 months, there has been a significant improvement with combined ratio coming down to 100% in FY17 and 99.4% for the 6 months ended 30th September,2017.

Further digging reveals that this is primarily due to strong growth in earned premiums in agriculture segment (Premiums grew from Rs 915 crores to Rs 8250 crores, accounting for 31% of earned premiums in FY17 vs 6% in premiums in FY16).

Combined Ratio in agriculture segment was only 92% (vs 169% in FY16 and 113% in FY15) The underwriting profits in this segment were Rs 550 crores [vs (678) crores in FY16] This swing of Rs 1200 crores helped post significantly lower combined ratio on overall basis. It must be noted that GIC has now reinsured 30% of gross cropped area in India and that 77% of agricultural insurance has been reinsured with GIC.

ICICI Lombard’s DRHP spoke of the fact that GIC was the only reinsurer offering reasonable premiums for agriculture, hence all insurance companies have reinsured agriculture risk with GIC. This makes GIC risk prone in the event of a drought. Management claims that they have spread this risk nationwide and since there won’t be a nationwide drought according to them such risk is lowered.

It remains to be seen whether they can sustain the overall combined ratio at these levels especially since motor, health and fire insurance, the three segments accounting for approximately 21%, 21% and 13% of earned premiums respectively in FY17, all had underwriting losses.(Combined ratios of 114%,110% and 104% respectively). Even more worrying is the fact that these have been the only growing segments in the last 5 years. Other segments such as liability and engineering which have shown consistent underwriting profits have barely shown any growth in the last 5 years.

Thus, agricultural segment is primary driver of underwriting profitability and low combined ratios in FY17 (31% of earned premium) and H1 FY18 (46% of net premium) and it remains to be tested as to how robust this portfolio is and how badly it would be affected in case of a drought.

It must be noted that their DRHP states -“We paid premiums of ₹ 6,788.71 million (Rs 679 crores or 8% of gross premiums) for retrocessional coverage to mitigate the effect of potential large sized risks in our agriculture business line in Fiscal 2017. Our agriculture portfolio is covered under multiyear stop loss treaties with high rated reinsurers from international markets”.

Investment Portfolio Analysis:

The entire point of running an insurance or reinsurance business is to earn on the float.

The fair value of investments held by GIC Re is almost Rs 70,000 crores which have a carrying value of Rs 39000 crores(only equity investments have been marked to market on which there is a gain of Rs 30,000 odd crores)

Detailed analysis reveals that the company has been incrementally investing less in equities, with equities forming only 3% of incremental investments vs 14-20% in earlier years. The management seems to be cognizant of equity market valuations and thus seems to be taking some money off the table.

However, it was a little surprising to see the equity portfolio being very cyclical. The sector wise composition is as follows:

Financials-41%

Infra-22%

Mining & metals-16%

Petrochemicals-13%

Auto and auto ancillary-8%

(Some clarity on this would be helpful)

Fixed Income returns in CG securities, SG securities as well as debentures and bonds is in the range of 8-9% over the last few years which is in line with prevailing rates. More than 90% of the fixed income portfolio is in AAA/AA rated securities or sovereign player implying minimal credit risk.

The overall investment yield over the past few years has been:

FY17- 12.34%

FY16- 12.9%

FY14- 14.1%

Premiums Written:

There has been strong growth in the net earned premiums due to substantial growth in the agriculture space. The net earned premiums for the past few years have been as follows:

H1FY18-Rs 22,485 crores

FY17-Rs 26,715 crores

FY16-Rs 15,173 crores

FY15- Rs 13,559 crores

Profitability:

The profit after tax for the past few years has been as follows:

H1 FY18- Rs 1809 crores(Annualized FY18=Rs 3618 crores)

FY17- Rs 3,127 crores

FY16- Rs 2,848 crores

FY15- Rs 2,802 crores

As per FY18E profit, stock trades at a PE of 18-19.

Return on Equity has been strong. The ROE’s for the last 3 years have been:

H1FY18- 19.6%

FY17- 17.4%

FY16- 16.21%

FY15- 18.97%

ROE’s have been 16%+ in the last 3 years and gradually improving. Underwriting has also improved with overall combined ratios coming down to 99.4% vs 107-108% earlier driven by agriculture insurance premiums received.

Risk Factors:

Competition-The IRDAI has permitted global reinsurers to enter the Indian market. This will lead to an increase in competitive intensity. However, GIC seems to be protected by the right of refusal it is armed with.

Exposure to agriculture/crop insurance- Due to government focus via the PMFBY (Pradhan Mantri Fasal Bima Yojana) this segment has enjoyed breakneck growth with earned premiums growing from 6% of premiums in FY16 to 31% in FY17 and 46% in H1FY18. This segment has been showing low loss ratios as of now, but performance of this segment would be critical to future profitability.

Alternative Sources of Reinsurance- The low interest rate environment has led to pension funds and hedge funds entering the reinsurance market

Valuations:

Considering the good underwriting performance (needs to be watched closely) and investment returns being earned, the stock seems to be available at very cheap valuations.

At current market cap of Rs 67,000 crores, the price to book ratio (including the fair value change account) is only 1.35. This is very cheap compared to other insurance companies such as ICICI Lombard which trades at a price to book ratio of more than 7 times(not saying that they should have same valuations but just seeing the discrepancy).

As Warren Buffett explains in his 1998 letter to shareholders-The key determinants are: (1) the amount of float that the business generates; (2) its cost; and (3) most important of all, the long-term outlook for both of these factors.

Hence, looking at these parameters GIC looks to be a solid long term bet which could offer steady returns.

Disclosure-I am far from an expert in analyzing insurance and reinsurance companies and hence apologize for any unintended errors in understanding.

Look forward to seeing a healthy debate on the pros and cons of investing in the business.

Year "Gross

Year "Gross