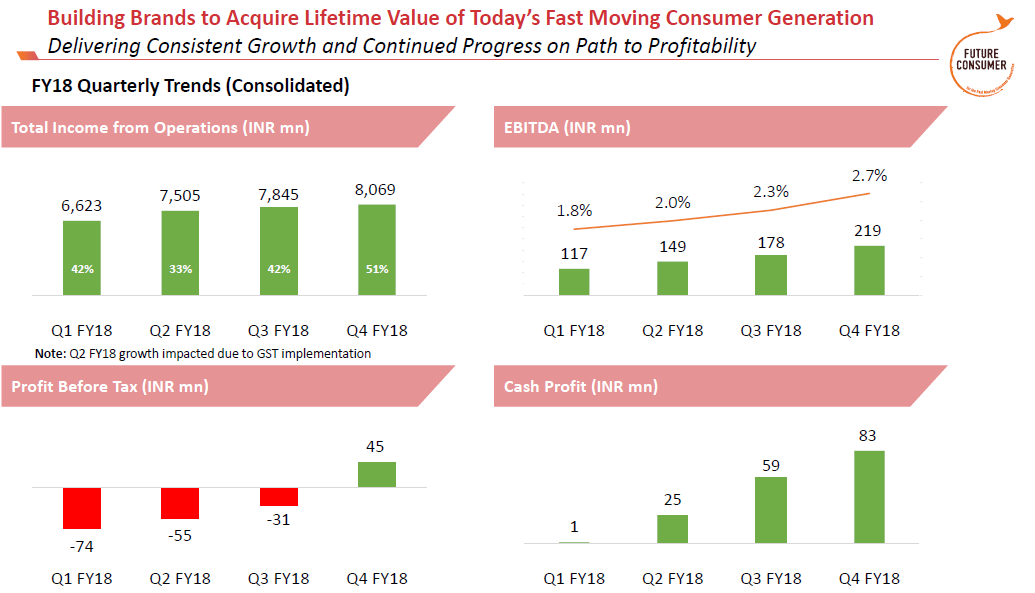

The last couple of years trend indicates that March quarter revenues are lesser than that of the December quarter. This time there is a slight increase QoQ

source - Q4 investor presentation

Q4 Numbers are much better than what looks optically. Company is moving towards profitability, albeit slowly. Since its volume game, it will take time to gain critical mass. But I think those who show patience with this stock will get rewarded disproportionately. Grocery is becoming highly attractive segment for all retail stores. FCEL provides that back end story for grocery purchasing.

Disclosure - forms 1% of my portfolio but interested to increase it in case of any fall in price

I am not able to understand that when company is growing with such a rapid pace then why this not making profit.

I seriously doubt about integrity of management and books they present to retail investor.

Vivek Vikram Singh

So by that logic you would also doubt integrity of flipkart and Amazon. Former hasn’t made a penny of profit while latter took extreme patience from its shareholders before turning profit.

I don’t think Biyani is any more honest or corrupt than an Anil Agarwal or Mukesh Ambani or even for thst matter Chanda kochar.

If you have any specific data points or analysis to present it would be quite helpful for fellow investors.

Thank you

Any idea though as to how they are planning to take these products outside their own retail stores. I havent really come across any of their products in the channels that I use for my own grocery shopping. I did see the Sunkist range of juices on Amazon but its just the product page - there’s no availability.

If I am not wrong, the Nilgiris chain of stores is a part of FCL and not Future Retail. In that case, which other retailer will agree to stock a competitor’s product range? ITC not having any of the supply chain and cash constraints has struggled to get going in the FMCG space so what is it that FCL is doing differently that will take them over the line?

It may be due to plastic ban in Maharashtra… All the stores have to change their packaging which will affect their business in the short term like demonetisation or GST

Regarding their products in north region they are aggressive as far as distribution outside their stores is concerned. Some of their products like Sangi’s kitchen , tasty treat are visible in Local kiryana shops. Although the demand is not high for their products but they are trying hard to get some space in local kiryana shops.

I think it will take some time to establish themselves against FMCG giants.

This is a detail report from MOSL which might help in understanding FCL future growth.

https://www.motilaloswal.com/site/rreports/HTML/636565282038142624/index.htm

Thank you - good read. But it missed what I think is the most critical aspect. Viz - how do they intend to get their products with other chains. Today it’s negligible.

Second - I’m getting increasingly worried about the capex requirement if the growth plan unfolds anywhere near the promise. They are highly leveraged already - so, funding the growth seems difficult.

About the first point I think they already have the largest retail chain in India so product distribution and upsale is not an issue but yes there was no clear strategy from the management for cross selling. But I don’t know if any other FMCG player have disclosed any such strategy as of now?

About the 2nd point yes the leverage is high and for this there are investment arm like Premji Investment , Amazon India and also a Chinese Investment arm is very much interested in this business so I don’t think fund for capex requirement will be a problem even though it is and will be very high in near term.

I am attaching a research on Growth sectors by Jatin Khemani. Please go through the Pulses section where he mentioned that total industry size is 2 lakh cr, growth rate is 5% and unorganized players are having 98% share of it. So I believe the opportunity is huge and this company is still in a very nascent stage with a strong distribution network and credible promoter.

This implementation for FCL I personally believe is a big thing to give them a business moat by giving agility and speeding time to market the agri procurement and food business. Since major challenge in a agri procurement business is to manage the perishable items which if not processed well in time will lead to major waste.

Looks like promoters have pledged the shares.

Future Coonsumer AR 2018.

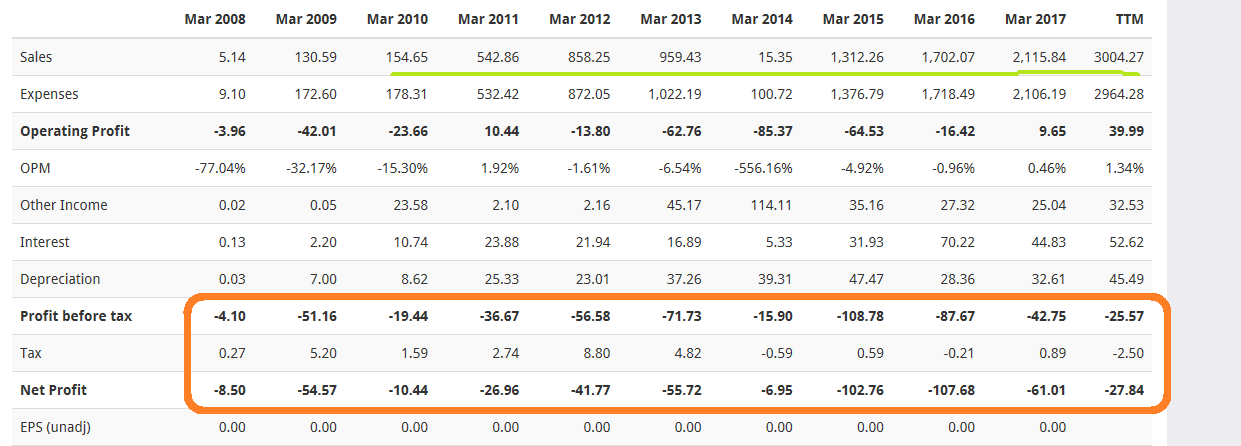

The following statement of Writing off of whopping 286 crores+ …would it clean the BS ?

In order to give true and fair view in the books of accounts

of the Company, it is proposed, subject to obtaining of

necessary consents and approvals, to utilize an amount of

2,86,90,40,797/- out of the amount of 3,14,27,82,392/-

standing to the credit of the Securities Premium Account of

the Company as on 31st December, 2017 by writing off the

Accumulated Losses amounting to ` 2,86,90,40,797/-. The

Notice convening forthcoming Annual General Meeting

includes the proposal for the said Scheme for Capital

Reduction.

As far as my limited knowledge about this aspect is concerned it seems to be a positive step.

Kindly, help me to understand its implications ,whether it is just an accounting entry or it will really help in clean up of bal sheet.

Thank you