The results declared by Finolex Industries have been extremely beyond expectations . Comparing on quarterly performance Whilst the increase in volume of Resin YoY has been just 9.2 percent this has led to almost an 132.7 percent increase in EBIT. If the half yearly performance ( for Resin ) is compared ( YoY ) the increase in EBIT is a staggering 217.6 percent. The rise in Resin prices have boosted the bottom line and will continue for a few more quarters. The investor presentation appended. Investor Presentation.pdf (6.0 MB)

2 Likes

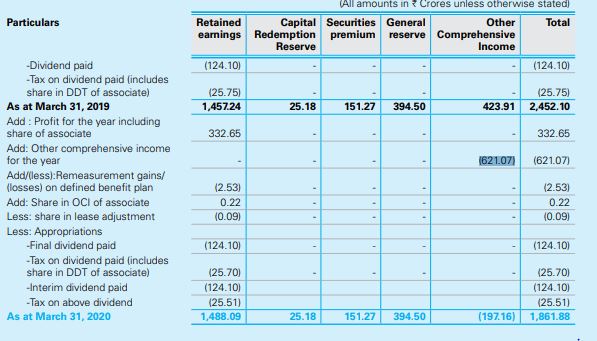

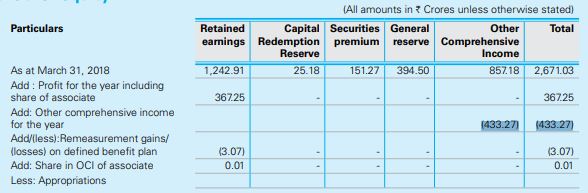

I noticed something unusual about the Other Equity section of Finolex Industries , During 2018 and 2019, their equity reduced even though they were posting profits, when i went to the notes of accounts, i saw

In 2018, they recorded 400 crores loss in other comprehensive income( because of reduction of value of equity), and in 2019 they recorded 600 crore loss in OCI because of same reason, but in Asset side, they have no investments apart from mutual funds, is there something i am missing?

2 Likes

They are also part promoters of Finolex Cable. so may be it is because of its market price fluctuations.

Prashant

Thank you for the help.

u will get the info in AR 2021 in the investments section

1 Like

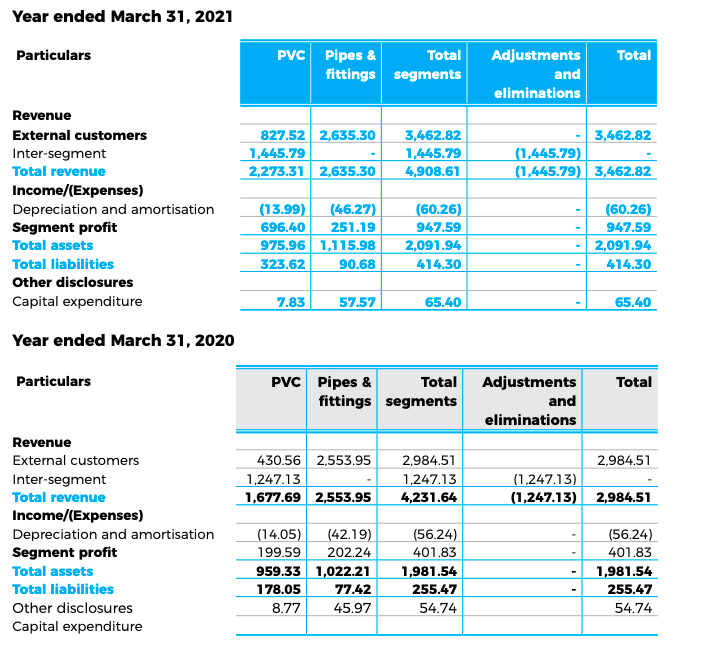

I was trying to calculate segment-wise profit for the company. Found below in FY21 Annual Report

For FY21 :

Pipes and Fittings

Revenue: 2635 and Profit : 251 which gives Margin(%) ~ 10%

PVC

Revenue: 827 and Profit : 696 which gives Margin(%) ~ 85%

Had this been case, why is the company focusing on shifting to Pipes and Fitting when they have such amazing margins in PVC ( Did similar calculations for previous years; getting margin ~50%)

Would be really helpful if someone can guide me if margins needs to be calculated differently

Two points here

- PVC margin calculation is wrong. You have to calculate margin with total revenue of that segment. Considering only external customer is wrong.

- PVC manufacturing is a backward integration process. pipes and fittings are their main business. They cannot do value add there and its is plain commodity business, there is no brand creation. Sometimes raw material creation part may have higher margin, but that may have some issues like scalability and cyclicality

1 Like

Do check the results of Q3 FY2015. PVC resin margins can be extremely volatile and very difficult to predict.

Pipes and Fittings is a branded secular business with a decent ROCE profile, PVC resin is a commodity business where the range of outcomes is very wide.

2 Likes

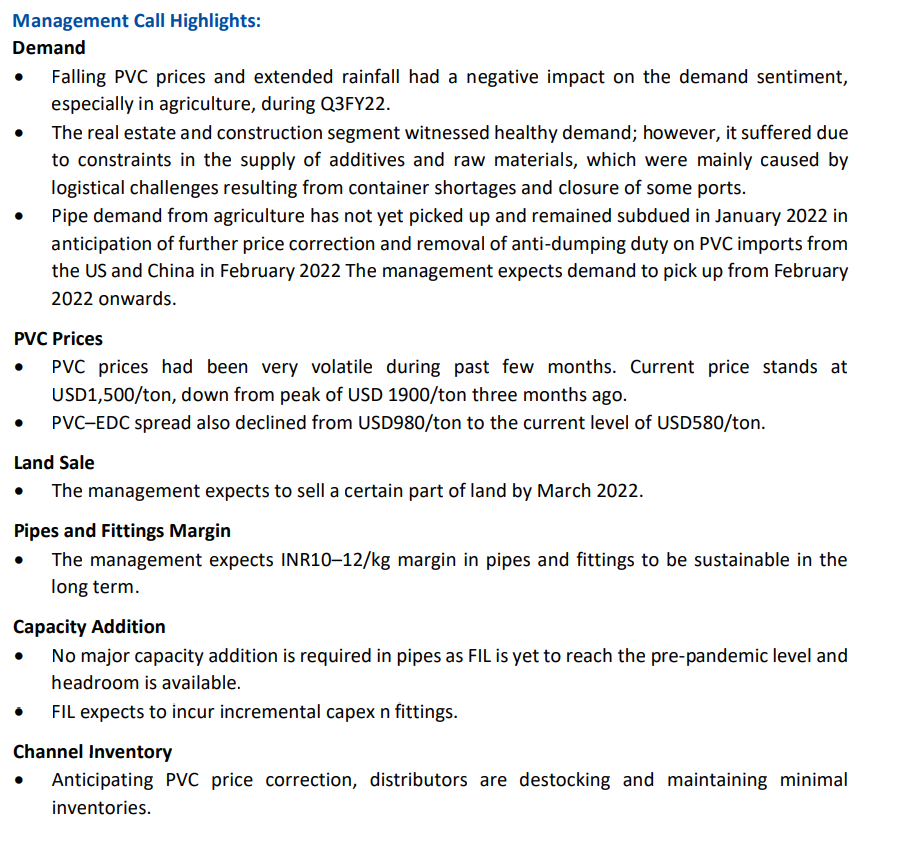

Q3FY22 Concall Highlights ( Please verify, there might be mistake in listening or Typing)

• There is good traction from real estate, while the Non-Agri and Agri mix is 60:40 in terms of value and in terms of volume it tends to be 65:35

• The Agri market is not yet opened up due to several reasons like uneven rainfall which have depressed the demand but the company is expecting the demanding opening up from Mid-February.

• Update about the sale on land- part of the land will be sold, it’s been under the process of completion in due course and effect can be seen in March results.

• ₹10-12 per kg margins should be expected in the pipes segment

• Fitting revenue in FY21 is 150 crores

• There is high volatility in the raw material prices, the spread has also been narrowed down and there is dumping from China and other countries which have been affected to the bottom line.

$ Per MT Q3FY22 Q3FY21 Current Prices ( As on 27.01.2022)

PVC 1756 1235 1500

EDC 969 470 920

Ethylene 1068 843 965

VCM 1403 960 1210

• CPVC has performed very well while UPVC hasn’t done good and is expected to do better when demand opens up from the agriculture side.

•

Pipes & Fittings Segment ( Volumes)

Agri Non Agri

Q3- (-24%) ( QoQ) Q3- 4% QoQ

YOY - -5% YOY – 30%

• The total no of SKU’s are 2200+ and the total non-agri ( includes fittings) are 1200-1300+

• Distribution- Key markets and focused areas are south and west India while new growth is expected from the north and east India

• Capex- in Pipes there is no requirement for CAPEX

Fittings incremental Capex will be deployed

• Total Capex for the year is 100 crores in which company deployed 50-60 crores and rest will be deployed in the next qtr. 100 crores of Capex would be deployed in the next financial years as well.

• Advertisement spend is 1-1.5% of the revenue

• China PVC is trading at 1300$ while due to supply constraints they could adequately supply to other countries, while Asia pacific the rate is 1500$

• Volumes

• Agri- 100,000 9MFY22

110,000 9MFY21

• Non-Agri- 55000 9MFY22

42000 9MFY21

• There is a shortage on the supply side of adhesives, looking for alternative suppliers for various products

• CPVC duty is been expiring next month but the company is expecting to continue ( key point to focus on the macro event)

• Expecting 5-7% of correction of PVC

1 Like

Can anyone help me where I can find import duties for various commodities. I know there was a 10% duty on import of PVC resin. I am not sure if this is removed in the current budget or sustained. If removed this can adversely affect Finolex as they are backward integrated and produce their own resin. China has cost advantage of 200-300/MT on the resin.

Management is evading a proper response to use of 1300 Cr. They did say that they intend to give it back to shareholders, but did not give a timeline. They have been promising that for sometime.

1 Like

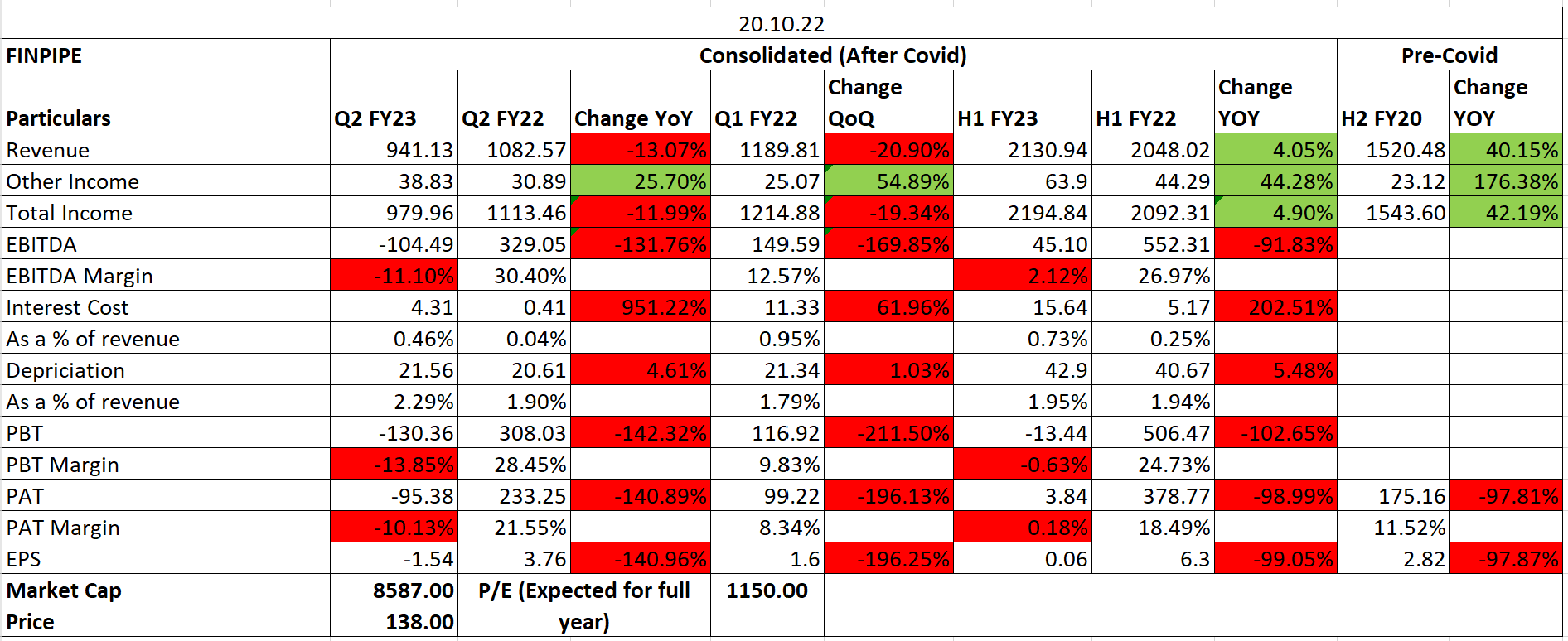

| - | Management guided that there will be a spill over effect of decline in raw material prices in Q3 FY23. The EBITDA has been severely impacted due to sharp correction in PVC prices against high priced inventory of raw material and finished goods leading to inventory loss of which a spill over is expected in Q3FY23 as well. |

|---|---|

| - | Demand has improved as price correction is there. And is likely to keep improving in the coming quarters. Volumes have also increased in this quarter and likely to continue in the next quarters as well. |

| - | Margins will remain under pressure in Q3 FY23 as well which will start normalizing from Q4 FY3. |

| - | The management stated it expects certain action from government on China dumping and expects slowdown in dumping post investigation on dumping. |

| - | Management expects to do capex of Rs2-2.5bn in FY23 and replacement capex of Rs1.5-2bn in FY24. |

| - | Q2 overall is a weak quarter due to monsoons and still there are better volumes than Q2 FY22. |

| - | Inventory Losses have made EBITDA negative. |

1 Like

Can anyone share how the cpvc pipe segment has been doing? I can hardly find finolex pipes in local stores compared to Aashirwaad and Astral.

Finolex is very much prevalent in Maharastra in my observation especially in pune and nearby districts.

1 Like

Thanks! Do you mean in cpvc pipe segment or agricultural pvc pipe segment?

Looks like management has waken up now. They are looking for revenue mix of 50:50 in pvc (agricultural) and cpvc (construction) segment. This would result in better margin visibility.

Key risk: CPVC segment have become hugely competitive. Barriers of entry are low and small players are entering the market.

Finolex management have been historically poor in marketing its cpvc products. So future lies in how they manage to create a brand awareness.

Current PE of 20 looks high due to poor margins (huge drop in cpvc prices). Margins may improve in future.

Nevertheless, Finolex is a cash generating machine - paying good dividends.

Any antithesis is welcome.

Note: Invested, 3% of my folio, since last 4 years

1 Like

Their commercial being aired now, is good.

They are focusing on longevity of their brand _ it has a good brand recall and undoubtedly oldest known brand in the segment. Hope it helps.

Disc:Invested