Quagmire

Investor presentation:

1 Like

Highlight of the concall -

“Postponing turnover target by 2 years from FY20 because third party products segment has not performed as per expectation”.

The 1Bn USD target by 2020 was too optimistic any way, I don’t see much of a reason to get worked up over when the company will get to that number. By my estimates I am fine even if it does not happen by 2025

The hard numbers are these -

Core business is being valued at under 6000 Cr after adjusting for the Finolex Cables holding

Dividend payout of 120+ Cr for FY2018

PAT of 300 Cr for FY2018

Almost all players are growing/expected to grow volumes in double digits over the medium term (3-5 years)

Since resin capex is unlikely to happen, FY2020 onward all resin consumption will be in house which means lower volatility in results going forward. This will also mean lower EBITDA margins in the long run but that in my opinion is a good trade off for lower volatility

Even after buffering for below average industry growth at 10% and more management gaffes in the conf calls, this looks like a safe bet now where the chances of losing money from here look minimal. I would not expect multibagger returns from here but 20% compounded over the next few years looks very possible. If one buffers for continued good performance of the Finolex cables story this looks even better

Below 550 I will be tempted to add more even though my allocation as per the initial plan is done. Let’s see where this heads from here

1 Like

any particular reasons for continuous downslide? I’ve heard that lead based pvc pipes are going to be banned going forward as part of an order given by ngt and moef has to come up with ways of implementing it, and i think finolex supplies such pipes. would this cause any considerable impact on revenues or on company’s opm?

disc : took initiating position in the company to track it and would increase after studying on it more, current valuations seem enticing but trying to figure out the future outlook

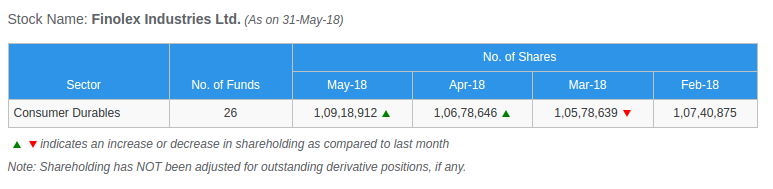

Mutual Fund holding of Finolex Industries has shown a increase in the last 2 months (i.e April '18, May '18)

Source: https://www.rupeevest.com/Mutual-Fund-Holdings/100940

I think that is more for drinking water pipes. The impact would be smaller compared to others catering majorly to housing market. Found the related snippet in a news article:

Responding to a parliamentary question on steps taken to monitor and curb usage of lead, the ministry had in February told the Lok Sabha that BIS, which has the mandate to prescribe standards for quality of products, has prescribed standards, including use of lead, for unplasticised PVC pipes for potable water supplies; chlorinated PVC pipes for potable hot and cold water distribution supplies; positive list of constituents of PVC and its co-polymers in contact with foodstuffs, pharmaceuticals and drinking water.

Finolex Industries Q2FY20 Earnings Call Highlights

Participants:

- SIMPL

- Kotak Mutual Fund

- Edelweiss

- Jefferies

- Axis Capital

- PCG Asset Management

- Investec

- Sumangal Investment

- IDFC

- Deep Financial Consultant

- HDFC Securities

- ICICI Bank

- BNP Paribas

Business Overview:

- Revenue at Rs 577 crore vs Rs 543 crore YoY

- EBITDA at Rs 82 crore vs Rs 125 crore YoY

- PAT at Rs 103 crore vs Rs 76 crore YoY

ConCall highlights:

- Pipe segment reported 8-9% CAGR in last four years; company is targeting 12-14% growth in current financial year

- PVC pipe is the leader among the plastic pipe. PVC pipe market is growing at double digit. Market size of plastic pipe is around Rs 28,000-30,000 crore; PVC pipe itself is around Rs 20,000 crore

- PVC market size will increase to 2.2-2.3 million tons by the end of this fiscal from 2 million tons of last year

- Finpipe is adding many SKUs for fitting range

- CPVC: Q2 volume at 2280 MT, up 11% YoY. Revenue at Rs 68 crore, up 28% YoY. H1FY20 volume up 22% and revenue up 39%

- Column Pipes: Volume at 458 MT vs 476 MT; revenue at Rs 5.6 crore vs Rs 5.6 crore

- PVC price at $900/MT vs $973/MT; EDC price at $317/M vs $332/MT; Ethylene price at $780/MT vs $1242/MT and DCM price at $735/MT vs $733/MT

- PVC/EDC delta has improved to $583/MT from $490/MT on sequential basis. Current quarter spread is around $590/MT

- Finpipe’s current capacity 370,000 MT, which is running at 65-70%

- Agri and non-agri mix at 70:30; company is working to increase the non-agri share

- PVC prices drops around 3-5% in recent months which will result into some inventory losses in coming quarters

- Fittings to piping ratio for agri is around 7-7.5% while for non-agri the ratio is around 15% (in value terms)

- SKUs: PVC- 400 for pipe and 1000 for fittings. CPVC- 37 for pipe and 175 for fittings

- Finpipe would add another 60-70 SKUs for CPVC

- Domestic market size for CPVC around 150,000-180,000 MT. There are four major suppliers of CPVC raw materials in India; two from Japan, one each from Europe and US. China and Korea supply around 40,000 MT

- EBIT Margin in PVC pipe is around 8% while for CPVC it is 12%

- India imports more that 50% of PVC resin requirements

- PVC/DCM delta for the quarter at $165/MT vs $240/TM

Capex:

- Capex for full year would be around Rs 100 crore

- Finpipe will increase the CPVC portfolio to 20,000 MT in next 3 years

1 Like

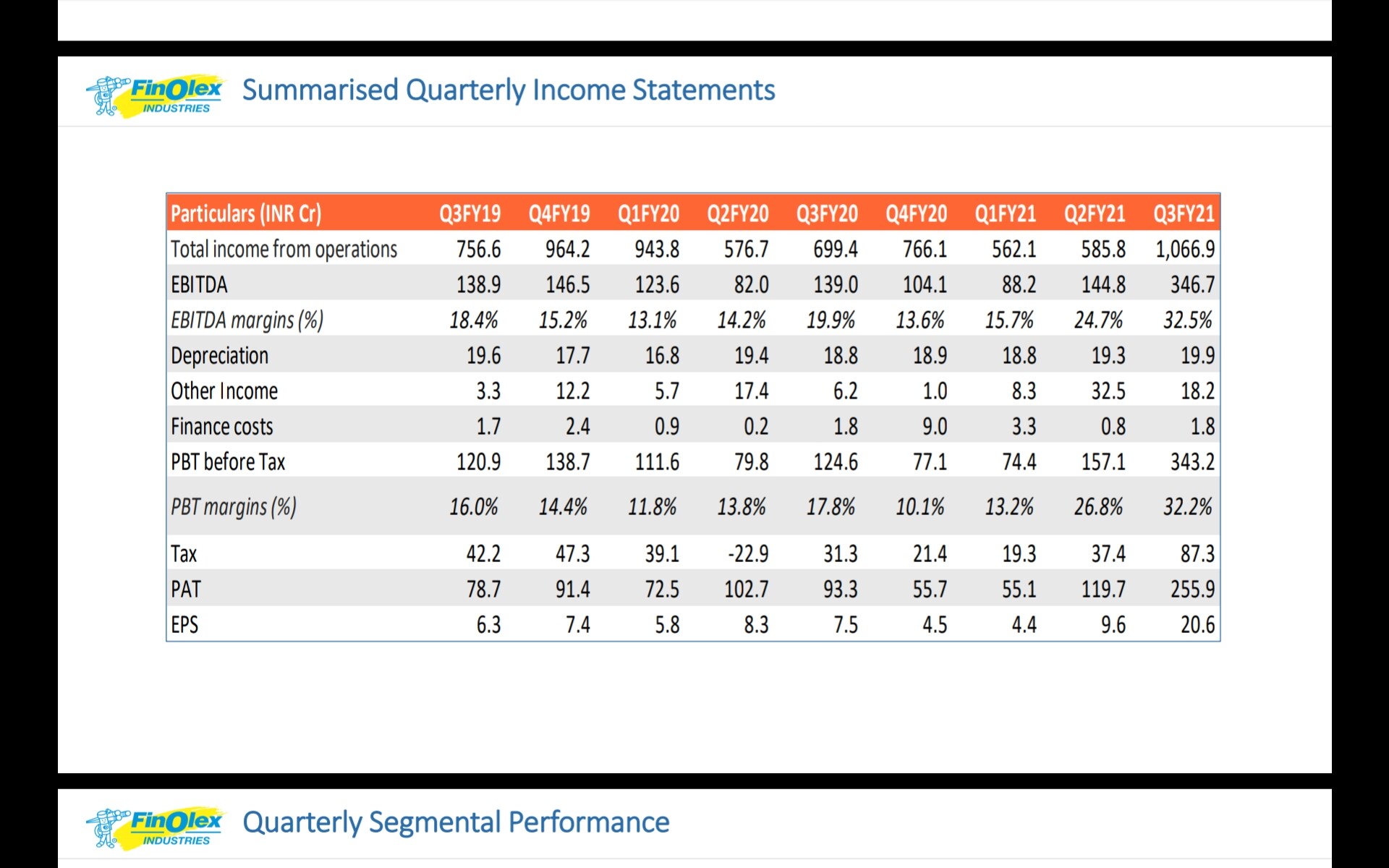

Q3FY20 highlights:

-

Highest ever PBT (Rs.1,246 Mn) and PAT (Rs.933 Mn) realized in Q3 of any year

-

Total income from operations was at INR 6,994 mn for Q3FY20 down 7.6% against INR 7,566 mnin Q3FY19.

*** Volumes registered a decline of about 11% in PVC resin and Pipes & Fittings segments. The mainreason for the decline in volumes was extended monsoon season with cyclones thereafter.** -

EBITDA stood at INR 1,384 mn for Q3FY20 down by 0.4% against INR 1,389 mn for Q3FY19.

-

Profit after tax was at INR 933 mn for Q3FY20 up 18.5% against INR 787 mn for Q3FY199MFY20 highlights

-

Total income from operations was at INR 22,199 mn for 9MFY20 up 4.4 % against INR 21,271 mn in 9MFY19.

-

**After healthy volume growth of 18% in Q1, the volumes in Q2 and Q3 have declined due to heavy and extended monsoon and cyclones thereafter.**In spite of lower volumes, operating margins are better on account of better realizations and higher PVC EDC Delta.

-

EBITDA stood at INR 3,440 mn for 9MFY20 down by 24.9% against INR 4,578 mn for 9MFY19.

-

Profit after tax was at INR 2,685 mn for 9MFY20 up 3.9% against INR 2,584 mn for 9MFY19

Speaking on the performance, Mr. Prakash P. Chhabria Executive Chairman, said, “The global and Indian economy has witnessed volatile market conditions in the past few quarters which has impacted various sectors. However, I am pleased to announce that we have delivered another quarter of decent performance.”

“The proposed Union Budget FY20-21 which focused on growth and welfare of farmers, and rural economy is expected to add impetus to our performance in the coming quarters. Our focus is on implementing strategies to expand our footprint while serving our existing base.”

Attaching Investor Presentation for same

Disclosure: Invested small position

1 Like

Finolex Industries Q3FY20 Earnings Call Highlights:

Participants:

- Jefferies

- Equirus Securities

- Investec

- Anand Rathi

- Kotak Mutal Fund

- TCG Asset Management

- Phillip Capital

- JM Financial

- Dalal & Broacha

- SIMPL

- Sumangal Investment

Business Overview:

- Revenue for the quarter at Rs 699 crore, down 7.6% YoY

- Volume: PVC Resin volume at 59,154 MT, down 11.5% YoY; Pipe and Fittings at 52,815 MT, down 10.8% YoY

- PVC Resin EBIT margin at 20.1% s 16.7% YoY. PVC Pipes and Fittings EBIT margin at 7.9% vs 7.4% YoY

- PAT at Rs 93.3 crore vs Rs 78.7 crore YoY

- EBITDA margin has improved as Govt. increased custom duty on PVC resin from 7.5% to 10%

ConCall highlights:

- Agri pipe volume impacted as monsoon got extended till mid of November

- Despite slowdown in real estate sector non-agri division registered double digit growth during the quarter

- Agri pipe has declined by 11.8% while non-agri registered 15% growth

- PVC price at $8680/MT; EDC price at $279/MT; Ethylene price at $780/MT and DCM price at $740/MT

- Ethylene drops significantly in last 12-15 months from $1,000 to $780-790

- PVC EDC delta for the quarter was $589 vs $535 YoY; PVC to VCM delta was $128

- PVC EDC delta currently hovering around $560-565. EDC currently trading at $330, PVC at $890 and VCM at $790

- PVC price drops by Rs 5 in Q3FY20

- Old high cost inventories got exhausted in Q2 and company has stared importing fresh raw materials from Q3 onwards

- Finolex currently adding many SKUs for fittings

- CPVC volume for the quarter was 2,489 MT vs 2,281 MT YoY. Column Pipes volume for the quarter was 429 MT vs 845 MT YoY

- Fonolex didn’t increase CPVC price in one go when anti dumping duty imposed on Chinese and Korean CPVC, but post that increased prices gradually

- Domestic CPVC market is around 150,000-200,000 tons; 30-40% CPVC comes from China and Korea

- Finolex has tie-up with Lubrizol for CPVC resin and price revised annually at the beginning of calendar year. Price for the current year is same as last year

- Finolex has raised PVC prices by around 5% since January

Capex:

- Capex including maintenance capex for next financial year would be around Rs 100-150 crore

Guidance:

Finolex has guided 10-11% growth for agri pipes and 15-20% growth for non-agri pipes for nex financial year

4 Likes

Due to Force Majeure declared by its major VCM (vinyl chloride monomer) supplier during March 2020, the operations of the Company with respect to its VCM to PVC (polyvinyl chloride) route will be affected for 30 to 35 days. This would result into a shortage of PVC production of approx. 15000 MT. However, our EDC (Ethylene Dichloride) to PVC route production will not be affected.

Manufacturing and supplies of PVC pipes and fittings of the Company will also not get affected.

2 Likes

Good Q3 numbers

*Single digit volume growth but high realization with soaring PVC prices

*Possible tailwind with infra sector push

*Valuations reasonable

- should end year with 650-700 cr PAT is available at market cap of 8000cr, cash on books close to 1000cr,

*closer to ATH, good price volume action on Q3 results( 5lac+ delivery)

- Q4 is usually strong qtr as pattern, ebidta margin may moderate but expect around 25%+ as long term average, going forward with infra demand revival

Views invited, this thread is unusually quite, explains past few qtrs

Invested - initiated tracking position

1 Like

Moreover, Finolex Industries holds 14.53% share of Finolex Cables valued at around 830 crores.

1 Like

The share is also going to be split to FV of Rs 2 , as per the Board Meeting held on 01 Feb. The date is however not yet announced for split.

1 Like

It should ride the pvc boom for at least 2 more quarters

It is piggy banking on other pvc manufacturers as it does not have its own inherent strength

Finolex group continues in the news for the wrong reasons…

2 Likes

Could you please tell the source for this.

Very strong numbers by Finolex Industries.

Very strong performance by Resin segment with EBIT jumping up 250 percent on the back of substantial price increase in Resin.

Fall in volumes Year on Year by almost 16 percent in pipes segment mainly because of a tepid first half of the year.

The stock trades at a very attractive 14.5 PE vis-a-vis

Astral - 95 PE

Supreme Industries - 27 PE and

Prince Pipes - 34 PE.

Also from concall from competitors, the non-organized market is facing headwinds due to second wave and the 35 percent unorganized market share will fall further. This could result in the organized players growing at a much faster rate, with the PVC pipes industries expected to grow at 10-11 percent + market share gains from unorganized markets, the entire organized markets can grow from 13-15 percent and if the PVC pipe sustains that could result in re-rating of first Finolex and than possibly the other players.

Here are some of the reasons why I expect Finolex to do well, since a lot of points have already been covered in this thread, I will note down the main points.

- 14.35 percent stake in Finolex Cables is now worth 1140 crores. The stock has almost doubled in the last one year.

- 70 acres of land in Pune which when monetized can result in almost 300-400 crores.

- Finolex is the only backward integrated player with the manufacture of resin(the key material used in PVC pipes) and PVC pipes. The company utilizes resin for manufacture of PVC pipes and sells the rest.

- Cash and Carry model which results in debtor days of around 7, which is very impressive.

- Struggle of competitors i.e. Jain Irrigation and Kisan Moulds due to high debt and unorganized players.

- A dividend yield of 2.3 percent but possible 13-14 percent growth year on year for the next few years at a very reasonable valuation makes Finolex the best company to bet taking risk-reward ratio in the plastic pipes.

2 Likes

Investor Concall Highlights -

- Capacity of 3,70,000 metric tonnes for Pipes and 28,000 metric tonnes for Fittings. comfortable with the capacity for the next 2-3 years.

- Q1 will be bad due to Covid-19 but it will be slightly better than Q1 FY 2020/

- Agriculture business is contracting but non-agricultural business is doing well. PVC pipes Agriculture/Non-Agriculture split is 63%/37%. Consistently increasing non-agricultural business mix.

- Company is moving away from Cash and Carry Model and giving some credit only in the non-agricultural segment.

- Only 40% land in India is irrigated, demand has to come back once the pandemic is over in agriculture pipes in the long run.

- Company aiming to hit volumes of 2019 despite a poor Q1. That would be a volume growth of around 16-17%.

- Total SKU’s of 2100, 375 in CPVC.