You should take owner earnings and divide it by market cap to get the yield they are talking about. The simple way is to use FCF instead and calculate the yield - FCF/Market cap. In my experience if you find FCF yield of 10%+ then that is worth investigating as an opportunity. In the depth of recession or when the good company is hit by some temp adversity you do find such opportunities. Dividend yield is very poor measure to assess the returns. FCF (or owner’s earnings) is better measure. This is the cash that is available to distribute to owners, if the management decides, without impacting ‘current levels’ of sales.

2 Likes

If the PSB stocks are trading below stated book value then it is because that book value is not sustainable or trustworthy. If non performing assets are high then that loss is covered from the net worth (book value) of that finance company. If the market suspects increasing NPAs and hence future erosion of the net-worth then the stock will trade below networth/book value. It doesn’t matter if the EPS growth is high or low in that case.

For finance businesses these things are very critical:

- Quality of assets and credit/lending standards- as depicted by NPAs, Asset-Liability management etc.

- Adequate Profitability - ROA and ROE (which is derivative of cost of funds and ROA)

- Earnings growth- this should be the last one and least important in three. Single minded focus on earnings growth can get you in trouble in finance stocks. Conservative & cautious management is preferred over the growth at any cost kind approach.

Not that if the ROE is low then the equity is diluted to fund the growth of disbursements. But some equity dilution is expected to fund the growth in finance companies. It is not bad per se.

1 Like

I talked about their way of calculating Owner’s Earnings. Owners Earnings and FCF are different. Please go in depth and then answer.

Sethuraman,

I am also talking the same. I urge you to read it very carefully and also understand owner’s earning concept as espoused by these guys, warren buffet and Grrenwald etc. They all talk the same though in different words -

"We calculate a business’s worth using a methodology known as the “owner earnings yield.” This is defined as

owner earnings—or excess cash earnings—divided by enterprise value. To arrive at owner earnings, we begin with pre-tax operating income, remove non-operating sources of income (e.g., gain on sale of assets and amortized pension gains), adjust for the difference between depreciation and true maintenance spending, and charge the income statement for options granted, inflated pension assumptions, etc. "

It is the money the owner can take out, if he wants to, after taking care of routine maintenance capex.

The calculation starts with operating profit. You add back book depreciation amount and then subtract the maintenance capex. This is the amount that is needed to maintain the production volume at current level. Then subtract tax calculated based on statutory rate etc. They also do other adjustments for one off profits, costs etc to get more normalized figure. The attempt is to gauge the normalized figure that can be maintained for some time. Looks like they calculate at enterprise level and hence divide by EV to account for debt.

Also for your information… if you take trouble to do such calculations you will find that the owner’s earning earning figure comes close to FCF often calculated as Net cash from Operations - Capex. Often times this is quick and rough way to calculate this figure. Again depending on whether OCF contains interest or not …you are either dealing at enterprise level or equity level.

The Davis guys try to find opportunities where this Owner earning/EV yield is at least twice that of 10 year risk free govt bond rate. Not at all easy and not available all the time. But don’t make blanket statement that such opportunities are not available from time to time.

I am presenting a contra view in this discussion. Negative on Banks & HFCs and positive on Credit rating & Insurance companies.

Banks :

Mr R Balakrishnan has written a very good article in Moneylife on “Valuing Bank Stocks”. He argues that the private sector banks are probably overvalued and public sector banks impossible to value. His basic thesis is that given the low ROEs from the banking sector (the best bank gets about 20% ROE), we are paying way too much for banks where the asset quality is presumably good. PSBs suffer because if the true bad debt recognition happens, there may not be any earnings left to compute ROE. Other stalwarts like Ramesh Damani and Porinju Veliyath also have a negative view on banking sector.

But that is not the only reason. IMHO, the economy is yet to turn the corner, the ground level situation is not good - people are not committing new investments, coupled with worsening bank balance sheets because of recognition of NPAs ……… I believe all the banks have so called bad/restructured loans in their books. Once it is classified as NPA (of course, not all of it…), the provisioning increases, denting the Net Profit. This process has begun (albeit after the deadline set by RBI Governor), which will continue for several quarters. I feel banking sector will undergo some pain in the near term.

HFCs : As I have written earlier in Hitesh bhai’s thread, I continue to get negative inputs from friends based in HFCs regarding new mortgage business. Several thousand apartments are lying unsold and the realty sector is in bad shape. However, Balance transfer business continues at brisk pace which ensures that HFCs and banks fighting with each other for lower rates thereby driving NIMs down.

Credit rating companies : The Kingfisher fiasco has raised a question mark on banks’ ability to asses / appraise the loan proposals. IMHO, there will be an ever increased demand for customer ratings by recognized rating agencies. To the best of my knowledge, some of the well run pvt banks have internal rating process by their Credit/Risk Depts. Not sure about the same with PSBs. So I see an opportunity here for increased business for rating companies. Not to mention the low capital requirement, excellent ROEs, good dividend track record and good FCF they generate.

Insurance companies : There is only one pure play listed insurance company as of now and I am positive on the long term potential of this sector because of under penetration in Life Insurance and increasing awareness about Health Insurance (because of rising healthcare expenses).

So, the consensus view is that the banks & especially PSU bank’s loan book is in trouble. And there is no way of knowing how bad the situation is.

IMHO this is precisely the opportunity that @Donald was alluding to when he started this thread.

Because of this common thinking - call it consensus/analyst view - the bank stocks are beaten down. The question now is, amongst these are there any bargains to be had - some stock/s beaten down well below the intrinsic value? Can we research/analyze these - separate the wheat from the chaff?

Analyzing a banking business is beyond my current level of expertise. Are there any experts on this forum that perhaps can chime in with their thoughts on the direction one should take to tackle this problem? I am willing to put in the effort.

P.S. The article you mention is behind a paywall…if possible can you please post a copy somewhere that I can read.

Thanks Donald and others for this discussion.

My take is slightly different. I think because of the high levels of leverage involved in the BFSI sector, this is an extra risky area to take educated bets on - simply because of the elevated level of leverage, the management / owner quality because all the more important. And it’s not just the quality, but also the intent / incentive structure etc, where these decisions can pull down the entire financial institution.

So, while yes, financial institutions can be great compounding machines (The story about getting your daughter married with HDFC shares), one needs to be extra careful with these companies because of the very high dependence on management quality.

Cheers

The power of compunding is not grasped in high growth buinesses, specially when equity raise happens at high P/B levels. Human mind/nature can not intuitively grasp it.

For instance SKS looks optically expensive at 25P/E buit given the growth just one year out FY17 P/E is 18 as per my estimate. Even adjusted for normalized tax FY18 P/E would be 24x. Satin Credit FY17 P/E would be a mere 13x. This is for a super high growth business with a high ROE!

There is no activity on this thread for more than 540 days.

I thought let me rejuvenate with a new title.

Post Demonetisation and GST formalisation of economy with a new scope for AMC & Insurances has started.

As these are low working capital, high ROE and ROCE businesses there is a huge scope for this industry.

A discussion on this topic is felt necessary.

Presently the MF industry is receiving 15-20% financial savings.

Previously this figure was less than 12%.

Sipping culture has increased.

Will this result in tsunami? If yes who will be the gainers?

Members can share their inputs.

There are multiple reasons why more and more saving money is moving to equities via AMC. So yes, they seem to be in a sweet spot. I am not sure if this is a usual phenomenon as economies mature. Lending rates decrease and so do deposit interest rates. And more savings start to move into markets. If it does then surely AMCs/brokerages and platforms like BSE/NSE/CDSL kinds are up for a good time.

That said, a market fall and sustained downfall can flight of capital out of the equity. Right now, We are witnessing a transition may be.

3 Likes

Whats the take on GIC Re going tobe listed in next week.?

GIC Re will be a major beneficiary of crop reinsurance scheme of Modi govt and will continue till 2019 n beyond.

Views Invited

1 Like

Just wanted to understand on why LIC accounted for over 50% of the bids fro GIC Re.What are they fore-seeing that they are investing 7k-8k crore where market response is tepid for this IPO.

My logic is LIC have to follow instructions from finance ministry to support PSUs

Thanks

Ashit

Managed to do some ground work on this - essentially looking at the non lending segments within the financialization theme.

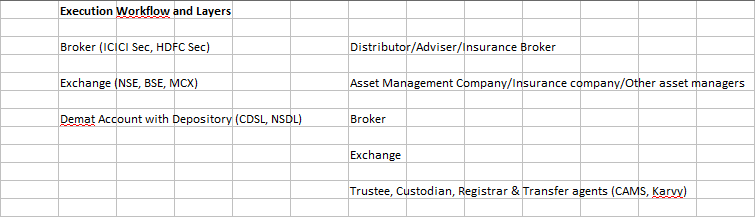

I always like to look at the complete industry value chain for a start and identify some basic categories before looking at specific companies. Reason being this gives me a 20,000 ft view of the industry growth rate, basic economics and dynamics, where the profit pools are currently and how they are likely to evolve.

Here’s a representation of how the segments are stacked up (on the lines of how a technology guy would try to represent the architecture of any solution) -

Now to size each of the categories -

-

Depositories - NDSL and CDSL combined revenue of 380 Cr and PAT of 165 Cr. No wonder the industry structure is consolidated here since the profit pool is limited and is not large enough to entice a new entrant. It is likely to stay that way for a long time since the key value addition here is reliability and efficiency in exchange for a hygienic price.

-

Exchanges - NSE and BSE combined revenue of 3400 Cr and PAT of 1340 Cr. Obviously a very profitable segment but then will continue to be consolidated for the same reasons mentioned above. The upfront regulatory and technology costs are too high and it will not be easy to take market share away from incumbents

-

Broking (including prop trading) - Adding up the turnover numbers of NSE and BSE, Cash turnover is approx 83,00,000 Cr which translates to an ADTO (Average Daily Turnover of approx 32,000 Cr). In the F&O segment combined the turnover is a notional 1649 lakh Cr but this is the size of the position. The underlying premium number would approx be in the range of 14.5 lakh Cr per annum. Working with these numbers, the size of the broking segment is likely to be in the range of 16,000 Cr per annum as of 2018, PAT is likely to be in the range of 4000 - 4500 Cr.

This segment has a big enough profit pool and does not have high entry costs, hence most of the new entrants have been into this segment. One should also expect to see more disruption here since the layer closest to the customer which offers the easiest profit pool should get attacked more. Industry structure as expected is an oligopoly with the top 5 brokers accounting for < 50% of the market, most of these brokers are backed by banks which serve as cheap customer acquisition channels for them.

-

Asset Management - MF AUM of 21,00,000 Cr as of March 2018, segment revenue of approx 18,000 Cr and PAT in the range of 5000 Cr once you scope in for the PMS and AIF segment as well. Once again the profit pool is large enough for new players to consider entering, however not all AMC’s are profitable since cost structure (other than distribution costs) are the same irrespective of what the AUM is. We have a long tail of players here which are getting consolidated at a healthy rate. Top 5 AMC’s (once again most of them backed by banks/large corporate houses) account for > 50% of the AUM

-

Wealth Management - Approx 8,00,000 Cr of AUA with revenue base of approx 8000 Cr and PAT of 2500 Cr. This has traditionally been the most dis aggregated segment since entry costs are next to nothing. Successful wealth managers will continue to branch out on their own till the pricing becomes such a challenge that this trend reverses. Large players here are once again backed by NBFC’s or Banks. Technology here is a real disuptor and is happening as we speak, once should expect a lot of advisors to become obsolete (especially in the sub HNI segment) since distribution, execution and reporting can all be better done through technology than via employees

-

Insurance - Annual inflow into insurance is approx 4,20,000 Cr. Analyzing this segment is relatively complicated due to the terminology and the actuarial science involved. Due to the underwriting component and the probabilities inbuilt into the business model, this will always be a dicey investment decision - akin to investing in lending entities. Hence my preference is to stay away from this segment till I get a hang of how to look at this

Looking at baseline growth rates -

- FD with Scheduled commercial banks has been growing at 15% between 2004 and 2018. This encompasses a complete cycle of boom, recession, rate hikes and rate cuts. This is baseline growth rate for the financial economy in India - 15% on the face of it is a very healthy growth rate

- MF AUM and Wealth management AUA has grown at 22%+ over the same period

- Inflows into Insurance appears to be growing in the 12-13% range from households

Long story short, the baseline growth rate for any of these segment is likely to outpace the GDP growth rate over the medium term. One could argue that banks will grow at a similar rate but other than insurance segment, none of the other segment have balance sheet risk involved. These are essentially low asset intensive, high ROE and highly scalable businesses. The only segment where the baseline is likely to be lower than this is in the depository segment since maximum throughput is likely to come from the bigger customers who already have demat accounts in place, while the depository will make a % fee per transaction, I cannot see too many non linear equations here which can deliver industry beating growth rate for a depository.

The biggest risks I see are -

- Regulatory risk (which also acts as a strong entry barrier)

- Market Risk (when markets go into bear mode this affects the real business of these segments, something you do not see in other sectors)

- Constant threat of new entrants in some segments (because they are highly profitable and capital requirements are not high)

- Threat of technology led disruption (especially in wealth management)

For the time being we do not have too many listed companies in all these segments, my sense is over the next 3-5 years this will emerge as a large sub sector within financials.

Source for all the numbers quoted here - Triangulation from data in the public domain from the RBI and AMFI, revenue and PAT numbers from the respective annual reports and other company specific publications.

57 Likes

@zygo23554

That was a real good work of data assimilation… Thanks

Partly to your point no 6 above, some of the metrics which are useful in evaluating life insurance companies in particular are :

- Embedded Value(EV) - Roughly NPV of all future profits plus shareholders net worth. All companies report this in the annual report. The actuarial assumptions are quite standard across companies so is a good benchmark.

2)13 and 61 month persistency ratios of premium payers.

3)Value of New Business (VoNB) and VoNB margin: If EV tells you size of historical book, VoNB tells you size of business written in last one year.

4)Ratios like PE needs to be compared across peers and cannot be taken absolutely due to lumpy profitability.

A last side note - the business models of life insurance is extremely different from general insurance. With life insurance the customer is treated as a subscriber for the next 10-20 years. In general insurance you could change your car insurance vendor when your current premium period is over. There other metrics are applicable.

I hope this helps. Let me know if you need more info. I have collated sector specific metrics on a lot of industries, so would be happy to help.

2 Likes

This book was one of the books recommended to me in the context of financialisation.

Following are some interesting things →

Brokerage industry in US was a cosy club for 125 years where commission charges were fixed. On May 1, 1975 this changed, when commission was deregulated. Most players reduced charges for institutional customers and increased them for retail clients. Schwab chose a different path & can be said to born on this day.

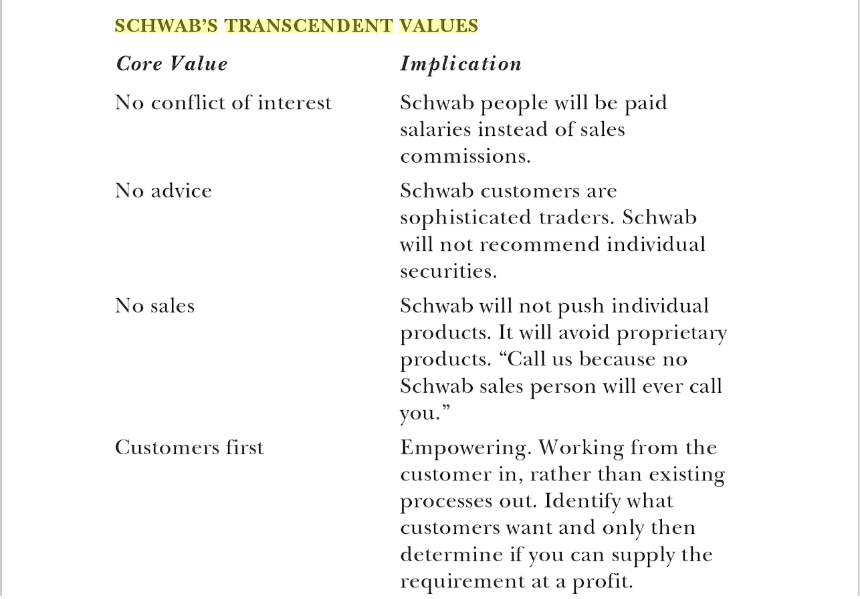

One learning for me was that - in brokerage/asset/wealth management/insurance industry - the risk of regulation would always be there (TER cut/trail model of commission are recent examples).

The companies which charge the lowest cost and those who charge much lesser than regulatory limits would always lead to huge disruption (e.g. Zerodha in Indian context).

This industry had & would continue to have many examples for unethical and unprincipled behavior. In such a scenario, following core values of Schwab is what helped it to be different from industry and the culture persisted. (at least for 2 decades+).

Some of these values need to be adapted for Indian context but some are really timeless.

Take no conflict of interest value, so many examples of this in India - ICICI MF buying ICICI Securities stock to bail out IPO, mis-selling of ULIPs by agents in pre-2014 era, heavy selling of MFs in the irrational phase of bull market etc.

While investing in any company in this industry, to judge it against some important core values forms a very important selection criteria for me.

Most of early business of Schwab was based on tele-calling, so the company was unsure about branch strategy. But to the company’s surprise, when it opened branches, the business in the area surrounding the branches boomed but the footfall to branches did not. The company learned that - people want to be perceptively closer to their money. There was something reassuring about seeing a real office. Most people came only once to open account and then did everything else on telephone.

Having physical offices would always continue to be important aspect of this industry and even banks. This is another important aspect to look for.

There was one problem with the branches though. The customer & local broker developed relationships & when broker left, a lot of customers also left. (I have heard stories of FD/MFs etc. moving from one company to another when relationship manager changes jobs). To prevent this, Schwab discouraged calling the same broker, calls were distributed across branches. To go around to mentality of treating customer as “client” in financial industry, Schwab hired people from outside of financial industry.

Another interesting product that captured the struggle between AMCs vs. distributors was Mutual Fund OneSource program of Schwab. The program did something simple - you could by MF of any AMC from a single account, no need to register with 10 different AMCs and deal with 10 different statements & formats. Schwab required a single account & provided a consolidated statement.

With this the balance of power started shifting to distributors from AMCs. Because a lot of work got reduced for independent financial advisors virous (IFAs), they shifted to Schwab. Further, as they could switch out a fund very simply - fund managers were on their toes. Schwab did not charge anything to customers to buy/sell MFs but fund houses paid Schwab just to get shelf space in Schwab MF marketplace. Schwab played further smartly as fund houses did not know the name of customers & hence could not do any cross sell etc.

Further, some of the one liners in the book really caught my attention and I enjoyed reading them.

- First we will be best & then we will be first

- The research reports are sometimes worse than worthless

- If you owe a bank 100$, the bank owns you. If you owe a bank $100mn, you own the bank.

- Different is not always better but better is always different

- Wall street is paid to recognize predictability and not breakthrough change

- Ordinary leaders have answers, inspired leaders have questions

One last thing that impressed me the most is Tom Seip’s speech at an off-site when he was passed over for the designation of President for an outsider candidate despite being a deserving candidate. So strong was the culture of Schwab and commitment of the employees, that he decided to stay instead of retire or find another job. His explanation of how he arrived at that decision is quite illuminating!

15 Likes

@zygo23554 - wondering if you have looked at bse ltd and specifically the bse starmf platform?

last financial year it processed about 3 crs txn. this year it would be between 5-6 cr txn. last year they were charging a blended rate of rs. 8. this year it should be between rs. 14-15.

putting all of this together the rev from the starmf platform last year was 30 crs should increase to 75-90 crs this year. that would actually be greater than the txn rev from the equity business for last year which was 80 odd crs.

in one of the con calls ashishkumar chuahan mentioned he would like to take up the rev per txn to rs 50. and process 15 crs txn annually. i guess this is possible over the 3-5 years.

https://www.bseindia.com/markets/keystatics/Keystat_MF.aspx

i guess, given your experience in this industry was wondering if you could share any insights you might have?

1 Like

@rishikeshs - Haven’t been able to take a look at BSE yet. Will get around to looking at stories like BSE, CDSL, MOSL over the next few months.

However I do know IFA’s who are using the BSE StarMF platform. From a user point of view if you have any specific questions you want me to run past these folks I could do that and post feedback

Hi @zygo23554,

it would be great if you could confirm the following observation with your friends.

- Is there is a huge shift in BSE’s attitude and are they professional and friendly to IFAs and serve them well ?

- Do they organise free training session for IFAs ?

- Is BSE the preferred platform for IFA’s ?

Thanks in advance for your time and effort.

1 Like