This stock came up last year in my screener due to 2 reasons 1. High momentum 2. Accelerated growth. As I started to get into details some reminder of past circling around me, let me put down the details here. You take a call accordingly:

Point No 1: Web of company structure and peculiar telephone numbers

I don’t understand why company is running a flash website. You won’t see any Indian faces on website. Lots of bombastic statement with capital letter used.

It provided two numbers to contact +91-22-24044876, +91-22-24082689. There are two numbers for Daman as well.

Look out for Mumbai telephone directory- Fiberweb India, Block No 2, Ground Floor, Kiran Plot No 128, Bhaudaji Road, Matunga-400019. Second number belongs to Pravin Seth (CEO/Chairman of company) having same address. I found it bit unusual for a company to provide CEO number directly, still it can happen for a small company or may be telephone number is taken in big boss name.

Now the twist Promoter list includes Sheth family and few Agarwals. Also one Gayatri Pipes and Fittings is promoter. But do note few years before other than Sheth’s rest were classified as public category holding substantial shares.

This company Gayatri Pipes and Fittings also share the same address as chairman address. The chairman (inactive now?), still transactions had gone through at the time of holding place of profit) and his wife holds directorship position.

There is another listed company named Kunststoffe Industries share the same address and same telephone number. Obviously belong to same promoter. Of course nothing wrong to have multiple companies sharing same telephone number and address. But to me it was unusual. I wanted to find out more. By the way in this company also Gayatri Pipe is a major shareholder, this time tagged as public including Soniya Sheth.

Point No 2: Grand revival, largesse and magical turnaround

As I mentioned earlier company used to have a negative networth and reported to BIFR and came out of it couple of years back and then roared to profits. There is more to meet the eye. Gayatri Pipe a Private Limited company which apparently have a common address and common director with company and have a 25 lacs paid up capital. This company had provided a term loan (without any interest!) of 100 Cr plus secured by immovable properties of 54 Cr book value only. And with a stroke of midnight Gayatri Pipe decided to waive off the loan, here becomes Networth positive and company is out of BIFR. Interest was never calculated on these loans, it could have run to 50-60 Crs alone in 5/6 years.

Apparently where was this 100 plus cr spent, here is the answer may be:

Go back to 2010-11 Annual Report. This is the year Gayatri Pipe gave 113.87 Cr secured loan. And ironically 73.52 Cr loan with Foreign bank becomes zero. Possibly Gayatri Pipe funded to settle this loan. Get cheap foreign loan and then do what?

I was more inquisitive to know as how did the turnaround happened? By improving the operations? By financial restructuring?

The company have an operational profit baring 3 years. It’s actually 2 years the losses were troublesome i.e. 2007 and 2011. Let’s grind back to 2011 to understand the story behind 82 Cr expenses.

In the year 2011 there has been an extraordinary expenses of 39.52 Cr. A schedule 2A created to state this, Exceptional items debit 103.61 Cr, exceptional items credit 64.09 Cr. And this is what company has to say in Director’s report.

Quote.**The regular activities of the Company during this period resulted in a profit of Rs.68.72 lacs as against profit of Rs.40.14 lacs last year. However considering extraordinary items the loss for the period amounted to Rs.38.84 crores. This is from 2011 AR.**Unquote.

I zeroed on PLBS to dig more. Increase secured loans by 105 Cr and decrease in unsecured loan by 75 Cr. A company with 40 Cr accumulated fixed asset and a turn over of less than 50 Cr all along, what it was doing with this whopping money? As I mentioned earlier largely loan to BHF Bank repaid. Again what was the loan from foreign bank used for? Fixed assets has been decreasing for last 10 years, no investments, CWIP. It was beyond me to understand.

By the way watch for other asset number 52.76 Cr in 2017 AR. This is almost 3 times more than previous 10 year average.

Point No 3: Shareholders and rotation

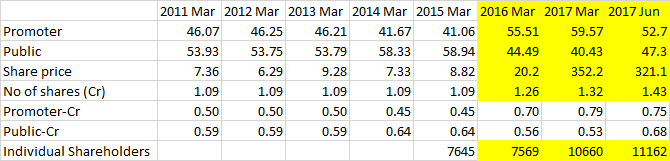

35 lacs shares has been added since last 6 years, good news is promoter’s share increased more overall in comparison to retail. How? By offline allotment to Gayatri Pipe being part of settlement.

Gaytari Pipes get classified as promoter and with offload of shares by them promoter holding is coming down rapidly.

Story is changing now- 15 lacs shares distributed to public category when price range was between 320-350. Where as 25 lacs shares added by promoters within price range of 12-20.

Closely watch for next shareholding disclosures, retail pie should go up more.

Point No 4: Funds utilisation and capital allocation

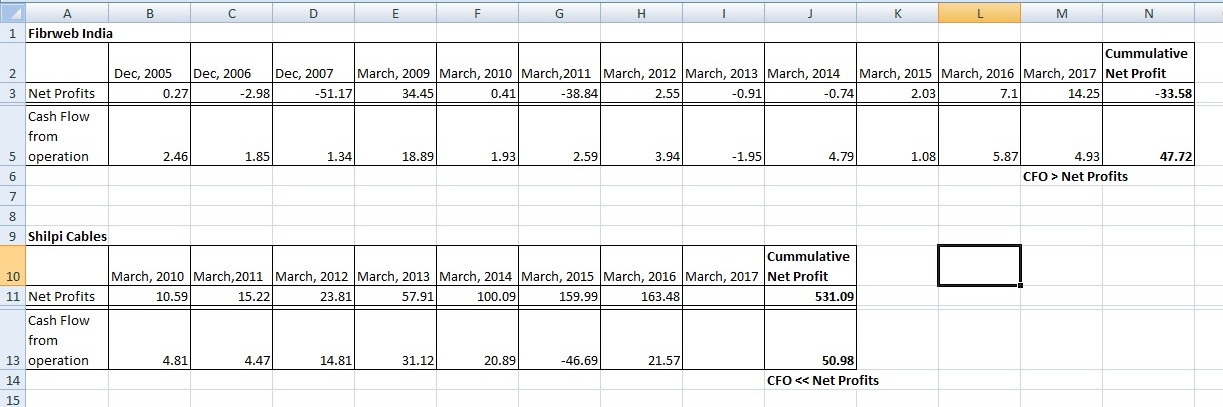

Year 2015-16: 7 plus crore was generated from profit left with 5.87 cr cash flow from operations. Despite company’s interest free status it has to sell fixed asset of 13 Cr around to repay the borrowings.

Year 2014-15: this time 2.03 Cr NP resulted a 1.07 Cr Cash flow from operations. Ironically no borrowings were required to be paid.

Year 2013-14: we had a negative profit of 73 lacs with positive cash flow of 4.29 Crs. How? Dramatic shift of working capital, trade receivables and loans and advances turned upside down! The working capital super performance was pumped to capex of 5.74 Cr. A loan taken from others (?) and working capital smartness resulted again to pay borrowers worth 9 Cr.

Please note the difference between cash flow from operations and net profit. Also, the borrowings repayment schedule (give one year, second year forget).

Point No 5: Numbers and KPI

If you look at KPI (ratios) be it efficiency, growth, cash flow there has been a phenomenal rise and turnaround in last couple of years. With so many interconnected dots my attention turned to related party transactions.

Except the borrowings management states no other major related party transactions occurred.

Let’s look at 3 of interconnected accounts i.e. payables, receivables and inventory.

Receivables has gone up by 2 and half times, trade payables has gone up. Inventory remain static irrespective of operations yet cash conversion cycle reduced this year (2017) thanks to payables which doubled and inventory halved.

From five points above I stopped out then. May be books don’t tell all, but I won’t still venture out with so many questions in my mind.

What discouraged me me finally before I close the file:

Point No 6: Word formation

I am sure all of us have red number of books of management communication. The cult is perhaps ‘Investing between the lines’ by Laura Rittenhouse. Now let me put some official announcements to stock exchange, you decide how often you see them. I am sure it would put Laura’s book to dustbin!

First the website, lots of capital letter words. Why?

A. 21 Sep- how many companies have informed stock exchange regarding brokerage report?

B. 28 Aug- Company Bags Very Prestigious EXPORT ORDERS of value added products for INRs 109 Million. What product, who is customer we don’t know? Somewhere it stated ‘BUYING AGENT’ in USA. Please note.

C. 12 Jul- Please find attachment regarding Company bags Very Prestigious EXPORT ORDERS for INRs 190 Million.

D. 16 May- Chairman boasts about super revenue growth and profit (forget to mention %, it says XX) and promise the future quarter to be brighter.

E. 23 May- Open flood gates of more profitable orders for your company. Will soar to greater height.

F. 07 Nov 2016- company speaks about book value. Book value is 50 for equity share of face value 10.

G. 07 Feb 2017- speaks about increase in EPS, interestingly also PE. This is what company has to say, ‘ with 3 months to go EPS is likely to be double the last years profit. Historically our industries are already enjoying 37/40 PE ratio multiple in market.

Please note for this financial year 62 communications have been dispatched to BSE, almost a stone away from big daddy Reliance Industries 70 communications.

Lastly 2 major drivers of growth:

-

Company speaks about 180 Cr order book, revenue reduced by almost 25-26% in June quarter 2017.

-

A capex plan of 100 Crs. Supported by funding? I guess interest free, or else interest cost

enough to knock out yearly profit. So far no interest expenses!

Now possibly I am not aware of what is going around in detail as I am not an insider. Yet I adore this forum, putting my points across. Lastly my wisdom says when unrestricted places pops up with multiple identification on internet better to stay away.

Disclaimer- not invested, unlikely to invest in future either unless something materially changes my workings and conclusion. Please highlight inadvertent error, will rectify.