This company will be a good Compounder of wealth …

Can you share the notes from the concall later if you are planning to attend?

Investor presentation Q4fy17

Few Concall Notes i could gather:

-

Management is confident of 20% top line growth till 2020.

-

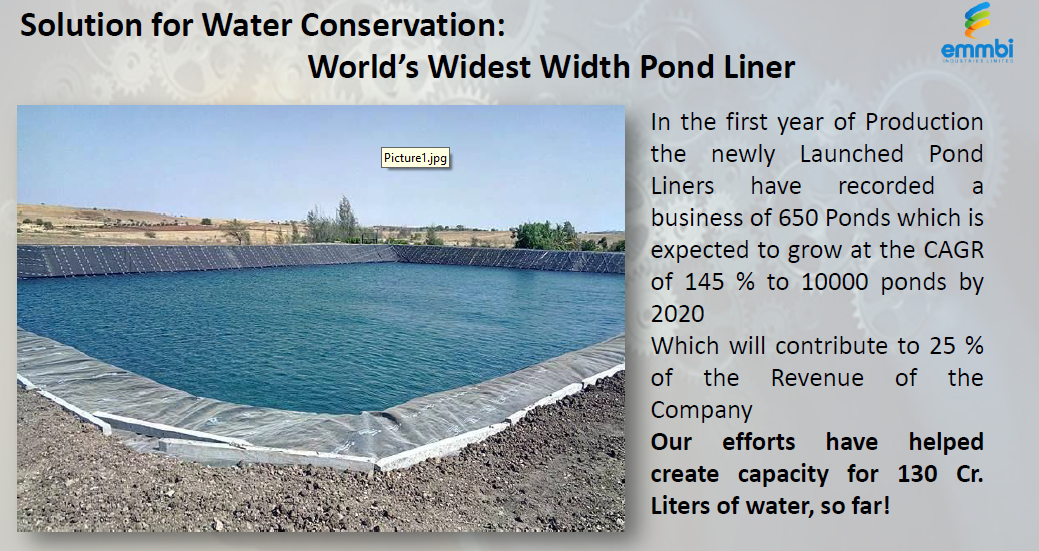

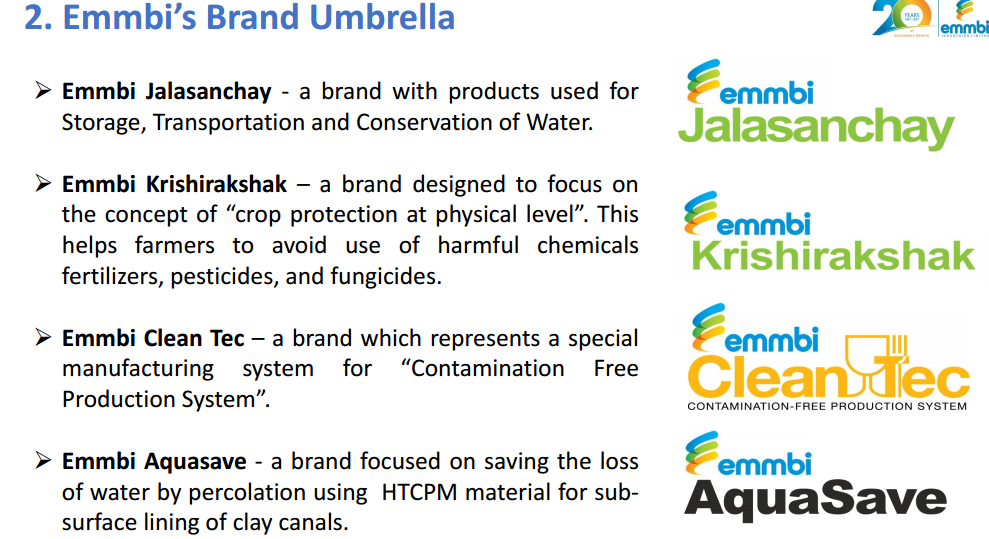

Jalsanchay Project Co is very optimistic on this front. they are projecting 140-150% CAGR growth in pond liner biz. Co has technological superiority over competitors for pond lining biz.

They are low cost suppliers with superior quality.

They have created ecosystem arround this project.

a. Like certification course to get skilled distributors n partners

b. tie up with banks for financial helps to farmers

-

Capex is almost completed in the tune of 25 Cr, may be some additional 5cr maintenance capex required for next 2 years

-

They have almost increased capacity by 40% with this 25 Cr capex.

-

Co is targeting for 20-25% CAGR growth over long term.

. -

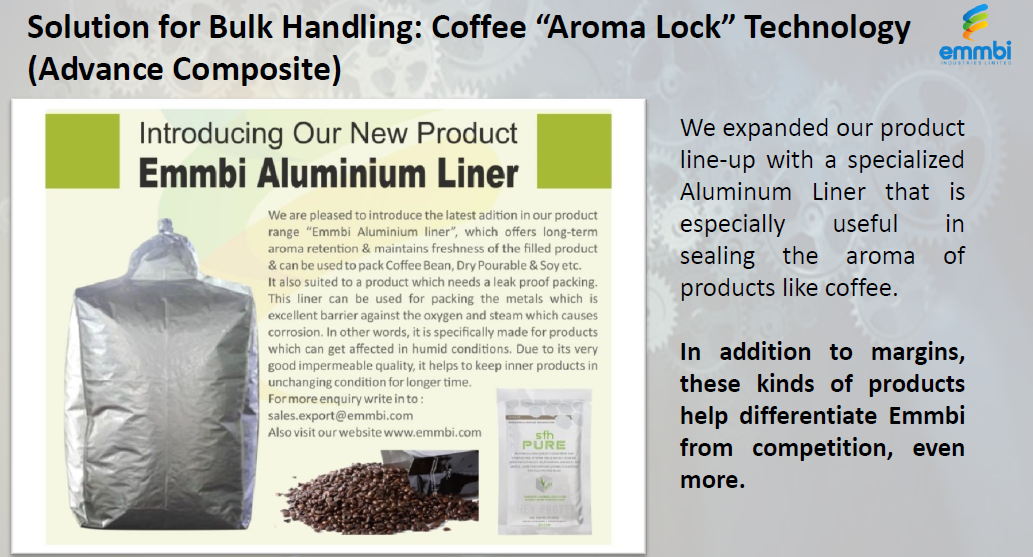

New products with strong R&D give them edge over competitors.

-

Pharma & packaging biz is high margin and mostly export oriented. They have already started biz with few of US cos.

8 GST: GST tax slab is 18% which does not affect co. as their prev tax was around same levels.

2 Likes

KR CHOKESY and ICICI extended their targets to 208 and 205.

1 Like

“Emmbi Industries Limited Q4 FY17

Earnings Conference Call”

May 22, 2017

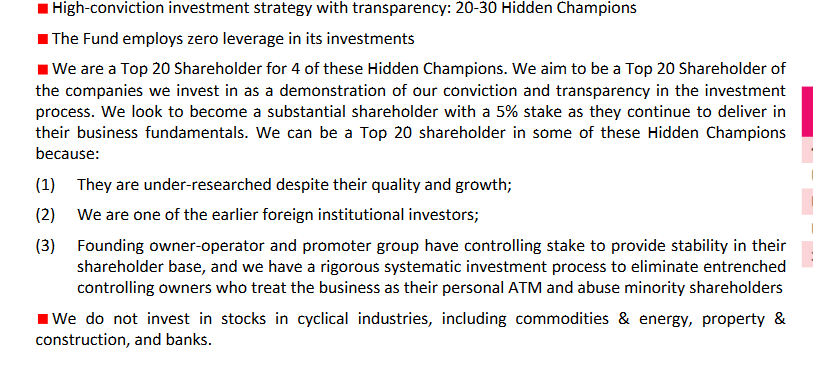

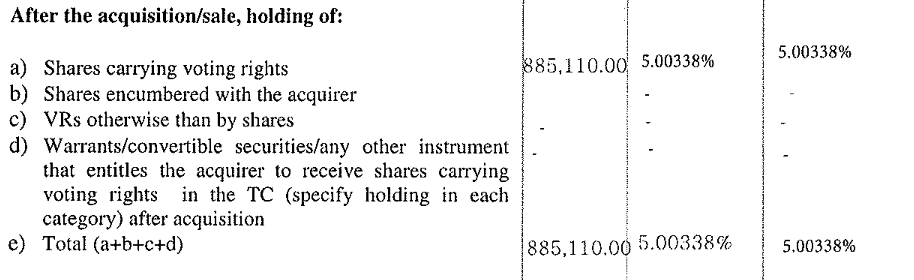

Hidden Champion Fund , a Mauritius based FII has started acquiring a substantial amount of stake in Emmbi. As per SHP 03/17 they have a stake of 1.54% vs 3.96% now.

I have looked at this fund and found out they pick under research quality companies with them being one of the first foreign investors present.

Here is what the Fund says about Emmbi:

They want to be a Top-20 share holder in all of the hidden champions they find and want to have 5% stake in each of them.

From the report it looks like Emmbi has planned set of product launches

What do people think about it’s future prospects?

Here is a link to their presentation: https://8iholdings.com/wp-content/uploads/2017/07/Hidden-Champions-Fund_PrivilegedClients.pdf

4 Likes

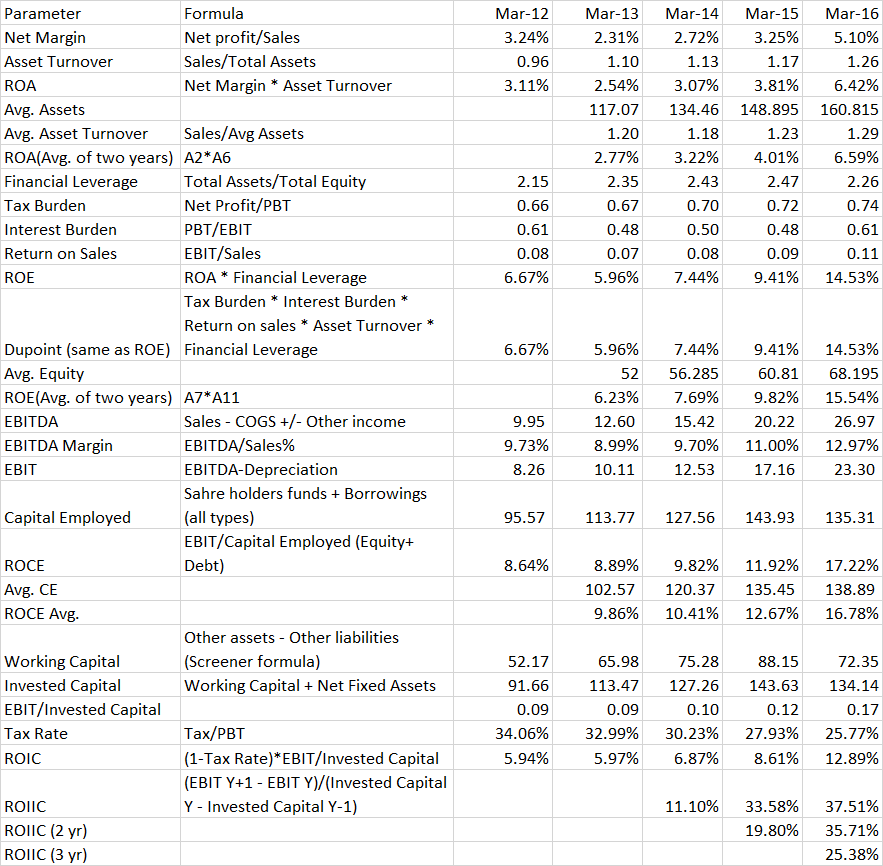

There is no surprise that Hidden Champion Fund has entered this. I have collected various return ratios for the last 5 years and on all fronts the ratios are improving. FY-17 is not updated as I don’t have the full data (Need to wait for IR).

Here is the data:

People who are tracking Emmbi, let’s let’s do a more detailed discussion on it’s business, competitive analysis, opportunities etc.

Disclosure: Emmbi is largest holding in my portfolio and forms ~19% of my overall pf.

2 Likes

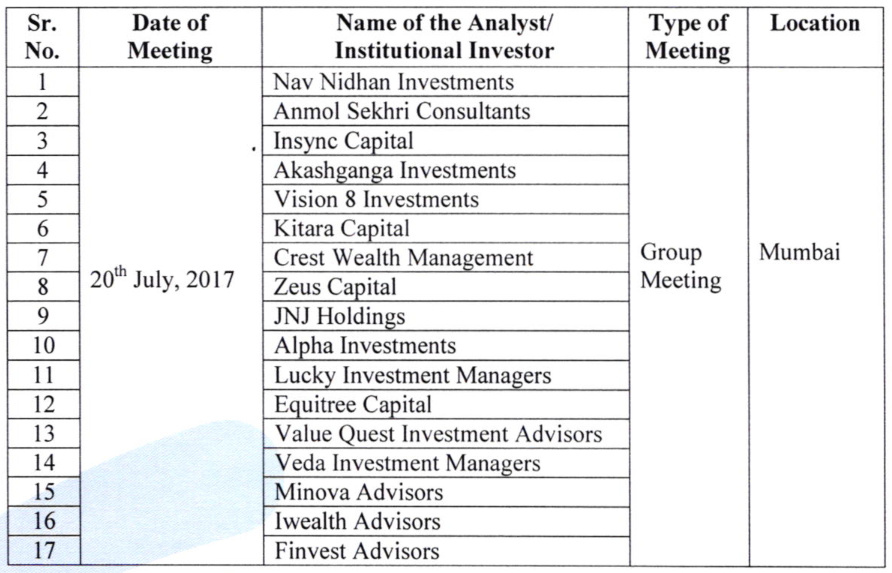

It’s great to see lot of institutional investors are meeting the management. We should definitely see increase in FII/DII stake in Jun-17 SHP.

Funds managed by great people like fundoo professor (Sanjay Bakshi), Alpha invesco are in the list of people who are meeting. Alchemy capital already met management in which RJ is one of the co-founder.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/bd79b3a5-2cb0-4f85-a955-1122c299edd4.pdf

http://www.bseindia.com/xml-data/corpfiling/AttachHis/b20f4cb7-15f4-4b23-a9fe-3dc5fcb1d4c8.pdf

http://www.bseindia.com/xml-data/corpfiling/AttachHis/2cd92ae6-7df4-4e76-a34b-da116d26cd52.pdf

Isn’t at the inflection point?

3 Likes

As they mentioned in the their fund prospects HIdden champion now acquired more than 5% stake in Emmbi. It was 3.96% on 06/17 SHP.

Latest announcement on BSE:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/B92FC9F9_CEED_4BEE_8666_E2A4B165A9BF_085301.pdf

Also, lot of institutional investors met Emmbi during last couple of months. Will look for 09/17 SHP which reveal if any of them has entered Emmbi.

Waiting for results on 14th August. Couple of interesting things to look at:

- How is pond lining business going on? They have started Emmbi Watcon as a subsidiary for doing govt. contracts in pond lining business.

- Impact of GST on inventory.

- There is no update on their Food & Pharma upgarde facility. They said it will be operated from June 21st. What happened to that and why there was delay?

1 Like

Good set of numbers from Emmbi.

Q-o-Q comparison is not encouraging. Could be due to couple of issues:

- Emmbi revenues are spread like 45:55(H1:H2).

- Pond lining business just started and might have not fully reflected in the results,

Q1FY18 Concall Notes

Few imp points

- As @rkothuri said results Q-o-Q are not great, management said results should be compared yoy basis due to seasonality of the biz.

- As Q1 being weakest qrtr for co and GST added further downfall in the numbers, now everything is working post GST next quarters co will do well.

- On products front co is doing good in pond liner biz and will look for expansion beyond Maharashtra and Rajasthan after Q3. which will improve quarterly nos.

- Clean wool is new product they have developed with approx market size of 360 million…co is very well investing and developing its R&D arm.

- R&D is more of demand oriented so they prevent excessive R&D expense.

- Main competitive advantage with Emmbi is " Excellent Product quality with excellent cost effectiveness. Till now they have been able to provide products at the lowest cost.

-

B2C segment has grown phenomenoly in this Q1 for co from 3% to 7%.

company had yearly target by FY18 end of 8-9% so they are surprised on this front. - Pharma facility is functional now. which will add to numbers from Q2.

Overall concall was good. To me with this results Emmbi is hold and add on dips.

Disc- Holding as significant part of PF from lower levels. so views are biased.

For me its 20% steady compounding story.

KRChoksey has come up with Q1FY18 result update with target price 214.

20170814_Emmbi-Polyarns-Limited_44_QuarterUpdate.pdf (689.3 KB)

1 Like

@drrakesh Thanks for sharing the concall notes. You covered most of the things.

Global pond liner market lists Emmbi in it’s research report and is only Indian company to get listed.

Q4 concall text: http://www.wovensackindia.com/Codeofconduct/KRChoksey-EmmbiIndus-Aug14-2017.pdf

FY17 AR is out and is here: http://www.wovensackindia.com/Upload/AnnualReport/Emmbi_AR17.pdf

1 Like

Not good news for EMMBI Canal Liners

Disc: Tracking Position Only

- Crude oil prices are rising which is bad news for the company

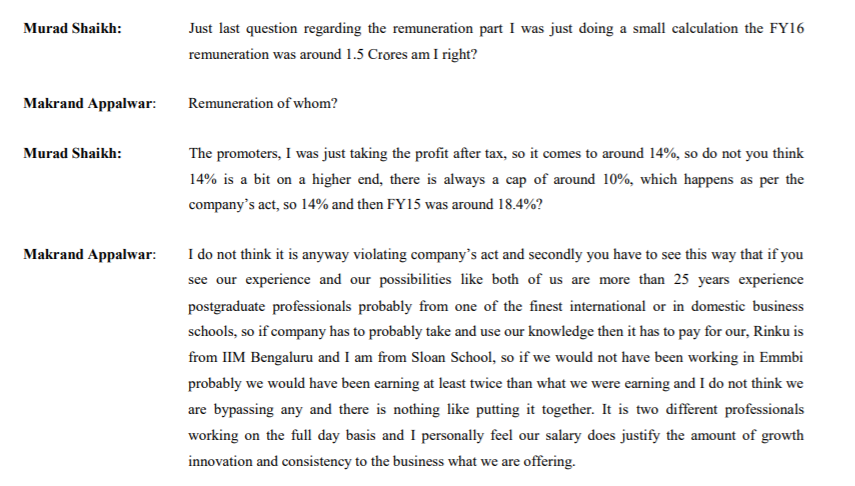

- Management remuneration is higher than 10% threshold which according to me is unjustifiable for a firm with that scale

- The company is hugely labour intensive, and it has to depend on leverage for doing caPEX.

Dr Vijay Malik has done an excellent analysis of this company. Please go to this link.

The analysis by Dr. Vijay Malik based on Himanshu Chajjer’s initial review is excellent.

Just my two cents: It is important to meet the MD and CFO(Husband-wife duo) to get candid answers to these questions.

After reading about the arrest-clarification and with no long term contract, there are a lot of caveats I would say before you decide to invest or even dabble in Emmbi.

I was evaluating this in August 2017 and then looking at these reports, decided not to pursue any further analysis.

Hope this frank evaluation helps.

Warm regards,

Nitin

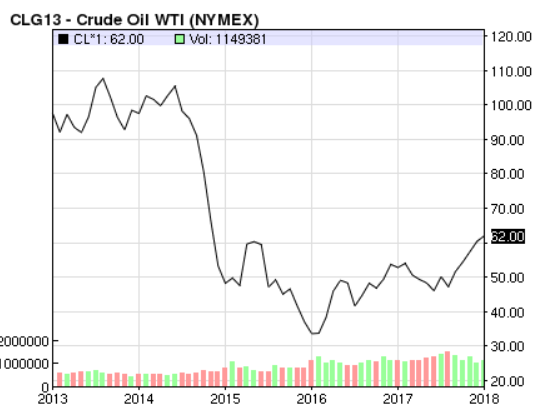

I believe as the oil prices are increasing. It is better to exercise caution than taking excessive risk. We have to understand how the management is going to tackle the rise in input costs.

In my view, the oil prices might go above $70 in H2FY18. There will be drastic impact if that is the case forward.

Yes, we have to keep an eye on raw material cost going forward.

I had looked at the crude oil prices vs raw material cost as a % of sales and see there is visible impact of crude price increase/decrease in RM cost though it’s not directly proportional to crude prices.

RM cost as % of sales. As you can see RM cost came down from 78% in 2013 to 69% in 2017 while crude came down from 100$ to 50$. In 2016 it came down to around 30$ but the RM cost is around 68%.

![]()

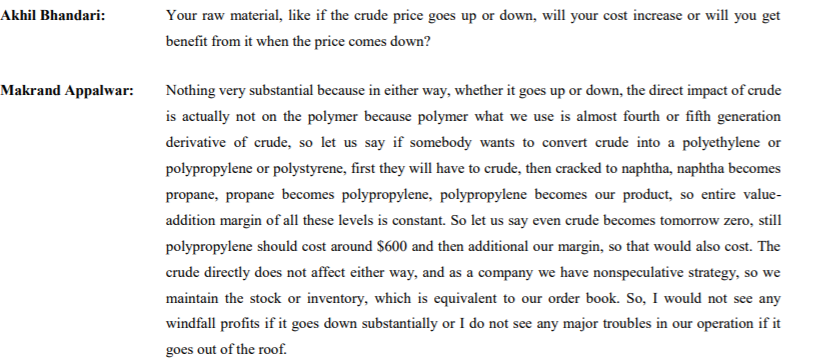

Here is what management has to say about it: (as per them it shouldn’t be much impact as their product is manufactured from 4th or 5th derivative of crude).

Source: http://www.wovensackindia.com/Codeofconduct/Transcript%20of%20Conference%20CallQ2.pdf

With that said I will definitely look at the raw material cost for Q3, Q4 & overall FY18.

Another interesting thing, last 10 quarters expenses as % of total sales around 86 - 88%. Operational excellence?

Here is what management has to say about it(though answers is not satisfactory). I am still trying to understand how these limits work.

Source: http://www.wovensackindia.com/Codeofconduct/KRChoksey-EmmbiIndus-Aug14-2017.pdf

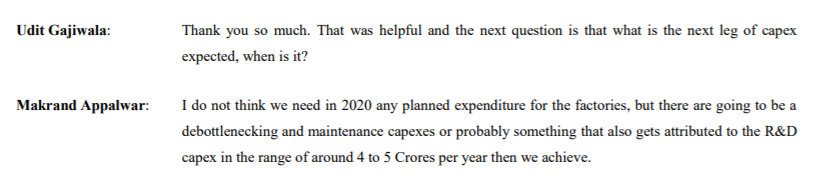

They have done capex of 22 crs. (15 - pond liner & 7 - clean room facility) and not planning to do any other capex for next 2-3 years apart from maintenance capex of 4crs.

Source: http://www.wovensackindia.com/Codeofconduct/Transcript%20of%20Earnings%20Conference%20CALL.pdf

Most of the data I have taken from management commentary and have not done outside research. Will continue to look at management promises and what they have achieved and probably come to conclusion whether whatever they are saying is correct or not.

Any other views are most welcome.

Disclosure: Emmbi is largest holding in my portfolio. Have started investing only couple of years back and might not looked at all parameters while investing. It will be very much helpful if others give their views.

1 Like

Still, I feel the management’s explanation towards higher remuneration is unjustifiable. We will have to see how the business goes forward. Personally, I would not prefer to buy this stock at this level because it does not offer any margin of safety.

He & his wife has done executive MBA kind of course in last 2-3 years and they themselves called from IIM and MIT… So irresponsible justification… How come such company with hardly any moat can command such valuation…Bull market main sab chalta hai

1 Like