Yes, that’s definitely not good. What I feel is that they are very new to con-calls, interacting with general public and are not very experienced to tackle each and every situation. Recent MMB board incident shows the same and in next con-call they mentioned that they don’t know how to react (they agreed it might be over reaction) and mentioned that they are also learning. In fact I would take that doing degree at this time in a positive way which might help in improving their management skills (though they might have not mentioned that way).

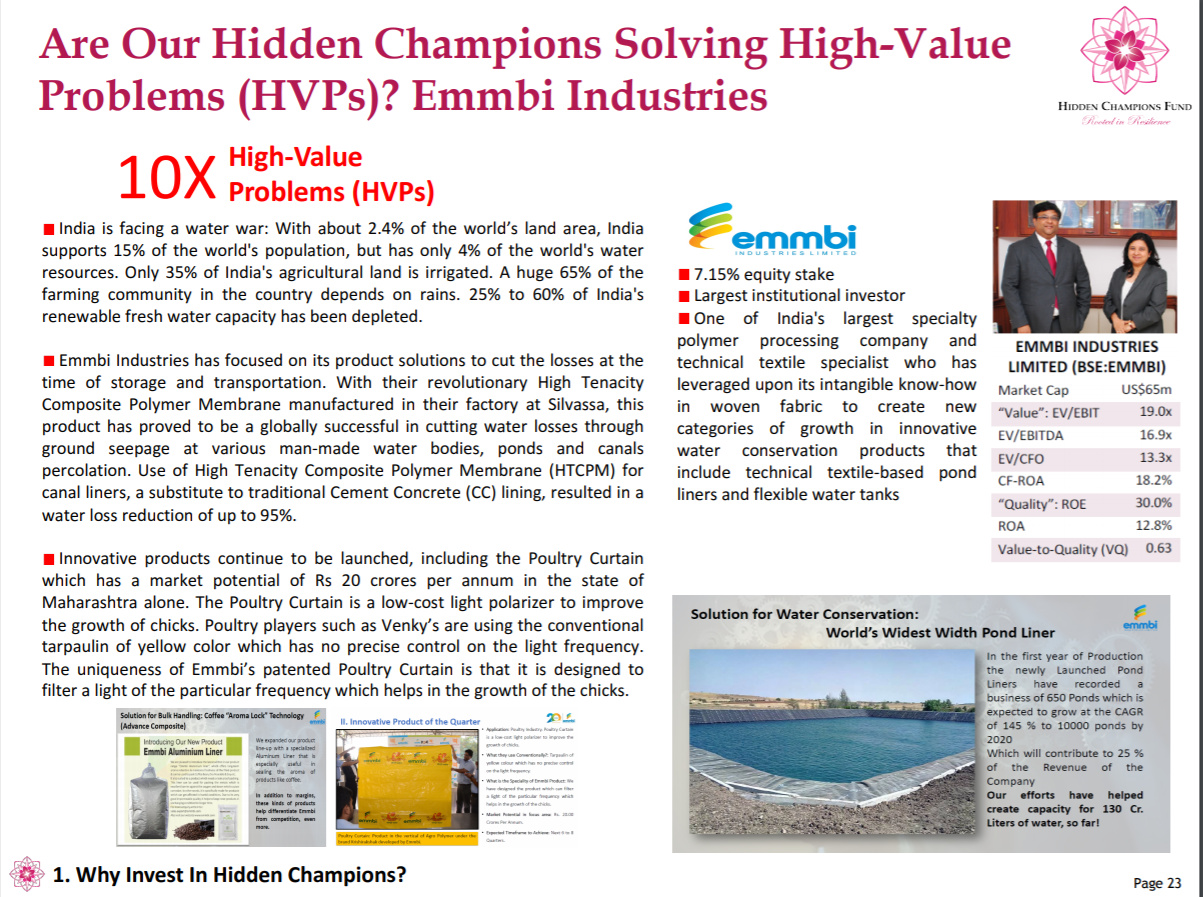

Though what I look at is their experience (almost 25 years of experience) and running the business started by themselves transforming from nowhere to a place where they have their reputation now. Sales increased from ~20cr 10 years ago to 200+cr now. What I like is more they are finding different applications for their product and continuously innovating and launching products at regular intervals. Though it might have not show immediate impact in revenue but will definitely show in future. In fact management has mentioned that they are going to produce one new product every quarter for next 6 quarters or so in one of the con-calls long back and I see that they are delivering it. For e.g. they have launched the coffee aroma bag, poultry cover etc. in recent quarters. They are currently researching in case by case basic but going forward I think they will be spending more money on R&D to design/innovate more products. Going forward the cash flows will definitely be improving as they are focusing on B2C through their krishirakshak & Jalasanchay divisions which the company can use to fund their R&D. I would definitely say they are focused, know what they are doing & learning along the way.

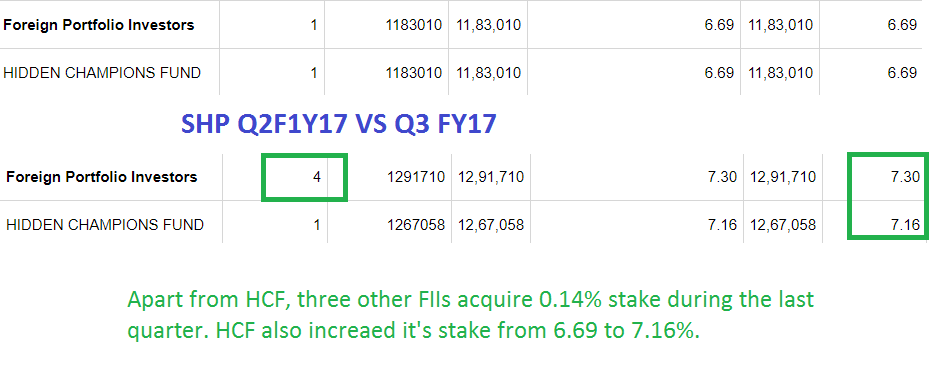

I think this could be the reason why even Hidden Champion Fund is acquiring good amount of stake even after they have mentioned that they want to hold only 5%. They are currently holding more than 7% stake.

Latest snippet from HCF brochure:

As I said in my above posts I am very new to stock markets, might have very fundamental mistakes in my analysis and ready to learn from others. Others, please feel free to update your views & guide me in right direction.

Most people do not ask this question, would you have bought this stock if Hidden Champions Fund does not have any position in this company? Are we biased by their entry?

Definitely not. When I started buying HCF has not even entered it. I have bought Emmbi in a sip fashion for very little amounts and accumulated it. Though it’s encouraging to see FII participation which will boost individual investors like me. As people say find a gem which no institution is holding and sell it every other guy holds and recommends. I definitely won’t be selling at this point of time and look forward to its story. BTW, lot of institutional investors are talking with management and we won’t be surprised if we see new names entering it.

What are the factors that could impact the earnings of this company?

Can share the research reports of pond liners market?

I had found this article on the internet. Let us dig deeper. We have to identify the market size of the products that Emmbi offers.

http://www.plastemart.com/news-plastics-information/global-pond-liners-market-to-reach-us$2-32-bln-by-2025/46168

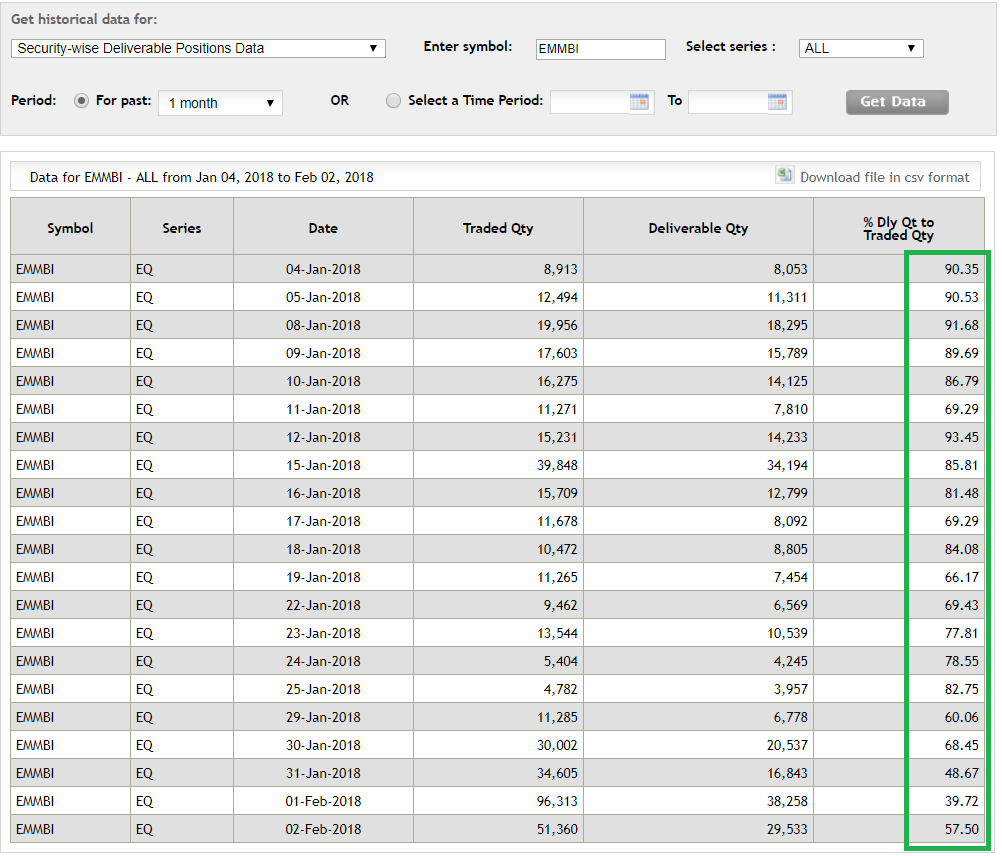

Looking at the delivery volume during January it feels like these FIIs are increasing their stake.

Emmbi’s recent presentation to HFC is good read:

http://www.bseindia.com/xml-data/corpfiling/AttachHis/ad1113f9-1545-4926-9c4d-1aad04633b9f.pdf

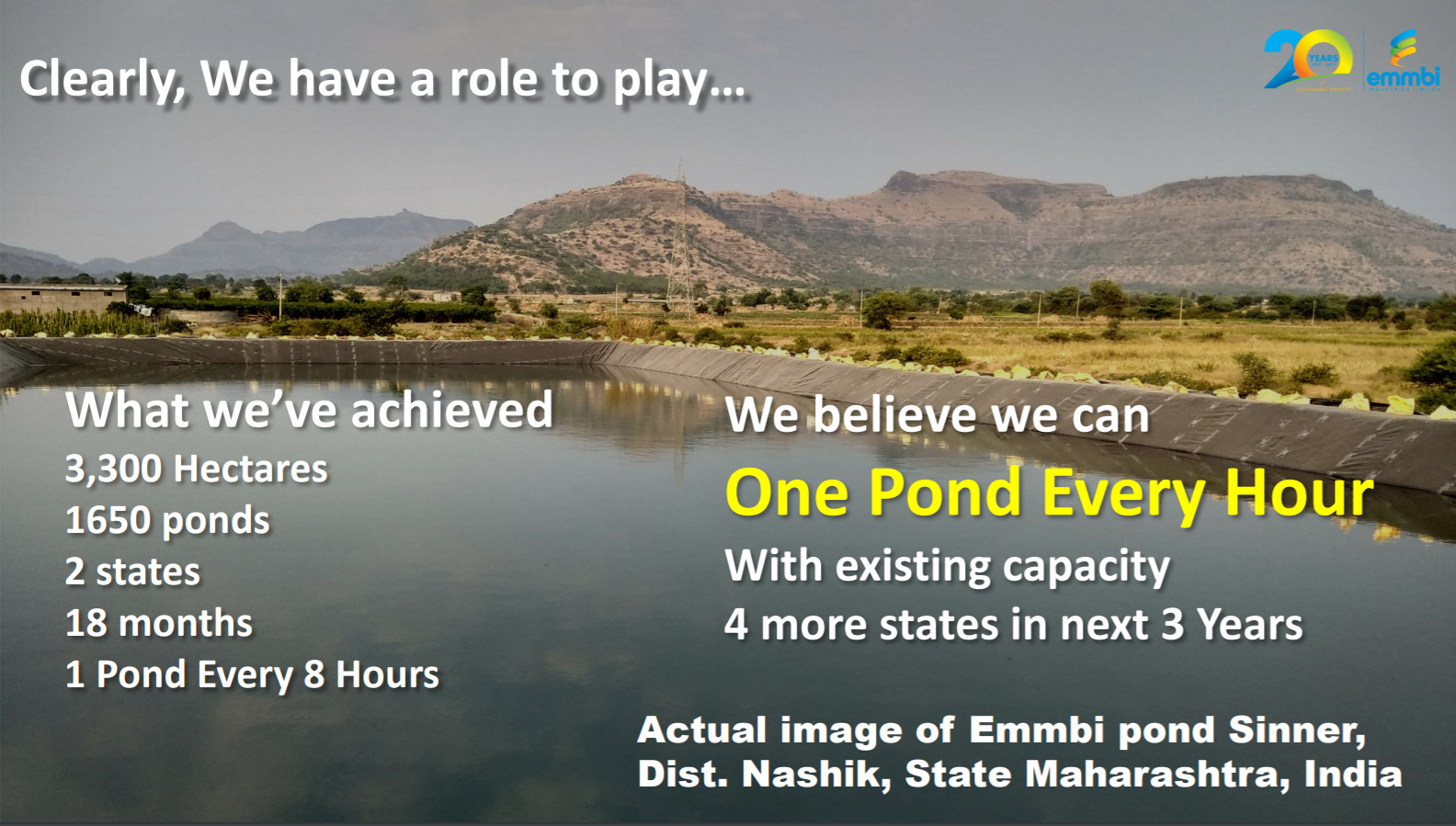

Some of the key take away points (on pond lining business):

- Already deployed 1650 ponds against ~640 add last year. So, they added about 1000 ponds in 10 months in this FY.

- Currently doing 1 pond for 8 hours which they believe can go up to 1 pond per 1 hour in 3 years with current capacity with plans to expand from Maharastra/Rajasthan to 4 more states.

Leaving with one of the ponds they deployed from Jaislmer.

The growth is mainly funded through gearing and not internal accruals. We will have to find out how this company is managing its working capital going forward. These attributes will be tested during a down market.

1 Like

If you BSE, the traded to delivery quantity is smaller. I would like to understand how this stock offers a margin of safety at this price. New views are welcome.

Hi I am not sure if my guess is right as I have just started research on this company, but won’t pond linings play a role in aqua culture which is a boom industry these days. However, I didn’t see any material linking emmbi to aquaculture on my research, could you please clarify?

They have some products that cater to aquaculture. Beware of valuations. Their dividends are funded primarily through debt. Their CAPEX exceed their operating cash flows. An investor should not take comfort towards this fact. There are lots of better opportunities available in the market. Exercise caution.

1 Like

Thanks for the advice and perspective. Despite valuations and questions about management remuneration policy outlined above in the thread, the fact that this company serves a niche which has the potential to explode exponentially is what grabs eyeballs about this opportunity. However, the niche could easily be short-lived transient or deep rooted and longer term lucrative. Must confess I got misguided by niches earlier and lost capital on companies like praj, bilcare and alphageo. Hence thanks again will be highly wary and watchful here

Most new investors criticize experienced investors without experiencing a complete market cycle. Always invest with a margin of safety. If we say something has a niche, why it is not reflecting in the margins? How will the margins improve going forward?

These are something we do not have valid answers.

1 Like

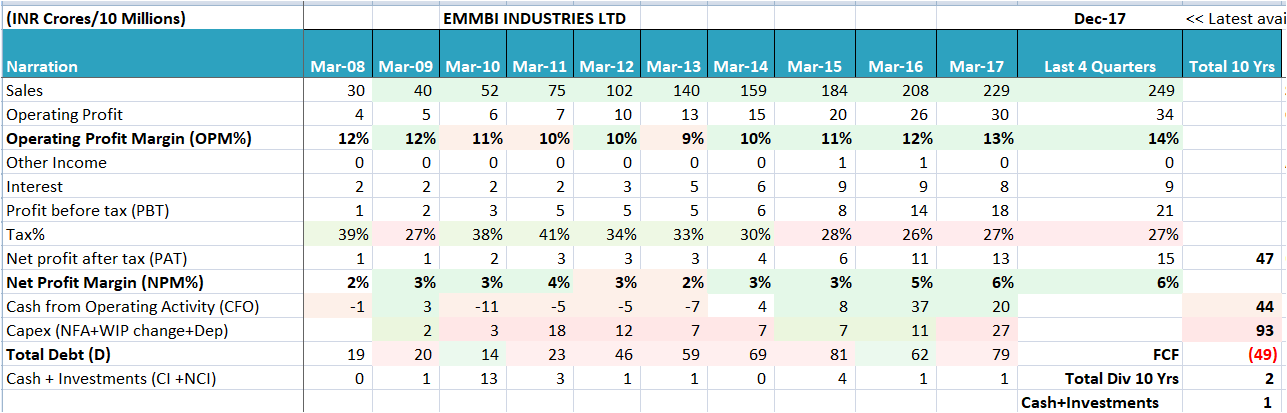

When I did an analysis of past 10 years, the company does not have a free cash flow. It is surprising how the company pays dividend when it does not have free cash flow. We need to get answers for how they are going to improve their margins and how the capital intensive nature of the business is going to change. I’m not a firm believer of niche or novelty. Show me a fine print with data, I will change my opinion.

Can you share your analysis?

CAPEX > cCFO

FCF < 0

Where are the dividends coming from?

Give me some concrete reasons how this company will survive in the down market?

How will the company improve its margins?

How will the capital intensive nature of the company change?

2 Likes

Kindly share the relevant data and analysis to validate your point.

Please see the sheet. “No free cash flow.”

Valuations are going to win the game. Leverage will harm during the down market.

I would recommend users to do their own homework. I have highlighted the red flags. It is up to them to make their own decisions.