Trying to put some numbers to Eicher’s next wave of growth. I think there are two growth triggers in place for Eicher: Exports and 650cc bikes.

Exports:

Lets try to think on what kind of automobiles Indian families would have. As the affordability increases, how would their vehicles change. I have simplified it into five steps below. I understand it is a lot more complicated than that but believe this is a good step to start with.

- First vehicle: Basic 2W upto 125 cc

- Second vehicle: Basic 4W with length upto 4 metres

- Upgrade the 2W to 125cc to 250cc variant

- Upgrade the car to a longer one

- Upgrade the bike to premium 250cc+

Market for basic 2W upto 125cc is very huge, 1 crore motorcycles + 66 lakh scooters => 166 lakhs.

Market for basic 4W upto 4 metres is 75% * total number of car sales => 25 lakhs.

Market for 2W between 125cc and 250cc => 25 lakhs

Market for larger cars above 4 metres => 8 to 9 lakhs

Market for 250cc+ bikes => 8 to 9 lakhs

This helps me conclude that RE’s market is clearly saturated. And all the volume growth they would get would be from India’s growth story but not their niche / brand. Their niche / brand equity would just protect them. Their market share is already 90%-95%, so can’t capture more. From now on, we should expect RE’s domestic sales to move with the regular auto industry. The management clearly understands this and hence the reason on why they are after export markets and their 2030 vision fully focusses on being a global consumer automotive brand.

| Month |

|

Exports Share (fraction) |

| Jan19 |

|

0.02515783827 |

| Feb19 |

|

0.0409388472 |

| Mar19 |

|

0.03940425112 |

| Apr19 |

|

0.05951112454 |

| May19 |

|

0.03463147937 |

| Jun19 |

|

0.05582886234 |

| Jul19 |

|

0.09233182615 |

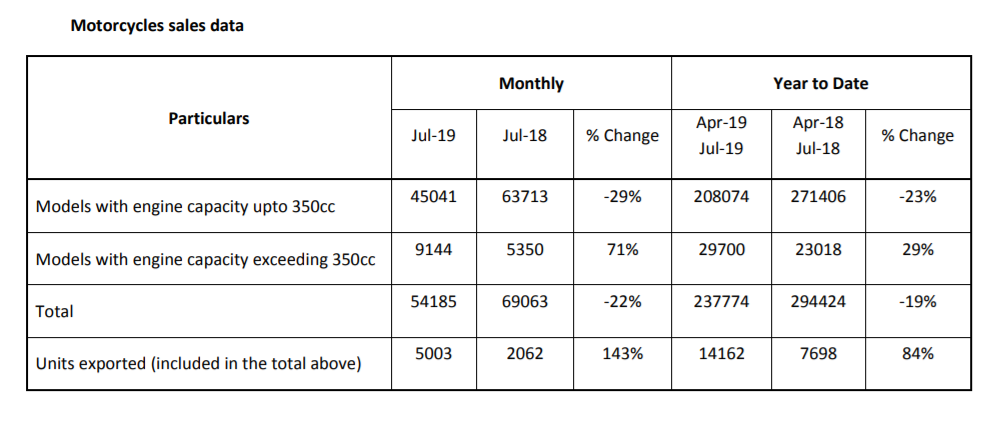

The performance in exports so far has been satisfactory and sales contribution to exports is increasing with time. If the 9% number from July is sustainable for few more months, then it means this is a good story we will be riding on.

650cc Bikes:

While exports is more about volume growth (though it can lead to value growth as well), 650cc bikes are more about value growth. 650cc bikes are priced at almost 2x of original bikes. So few years down the line, if we have 33% sales contributing to the top-line from these 650cc bikes with same number, then we are already sitting on 1.33 times current revenues.

| Month |

350cc+ Share (fraction) |

| Jan19 |

0.06583128155 |

| Feb19 |

0.08942998563 |

| Mar19 |

0.09799279972 |

| Apr19 |

0.1170024969 |

| May19 |

0.1048243575 |

| Jun19 |

0.1141774799 |

| Jul19 |

0.1687551906 |

Above trend is extremely encouraging. Its less than a single year and 16% sales (by volume) are contributed by 500cc+ segment to total sales in July. If this trend continues, we might sit on 33% volume sales from 500cc+ segment in FY21 itself.

Notes:

Market for basic 4W upto 4 metres is 75% of total number of cars according to Maruti Suzuki Chairman (read AR FY18).

Market for various cc bikes can be obtained by dividing RE’s sales with its market share in those segments. RE’s market share in those segments can be obtained in Eicher’s Annual Reports.

Disclosure: Initiated 2% position in Eicher Motors in last 30 days. Might consider buying more in the following months. Investor shall do his own due diligence before taking his decision and understand that this is not a buy / sell recommendation