https://www.bseindia.com/xml-data/corpfiling/AttachLive/2cc6e809-6531-45ec-a99d-c60f4be1d6d3.pdf

Hi @dineshssairam,

What does updated valuation calculation say now that the capex of 800 Cr. is announced and the first major assumption listed by you has changed.

What changes will come now going ahead?

Disc.: Forms 6.5% of my portfolio. Wanting to add more.

The Valuation I did was way back then. I need to Value Eicher Motors again to be decisive. I’m planning to, once Eicher Motors releases the Annual figures this year.

In any case, if you check out the figures in my Valuation, Eicher Motors was already spending more than 700+ Crores every year on Capex. I guess this would be a one-time doubling of Capex, which in my opinion will hardly move the Value of the company. We can try assuming that this Capex will increase Sales growth, which could possibly change the Value. But it’ll have to wait.

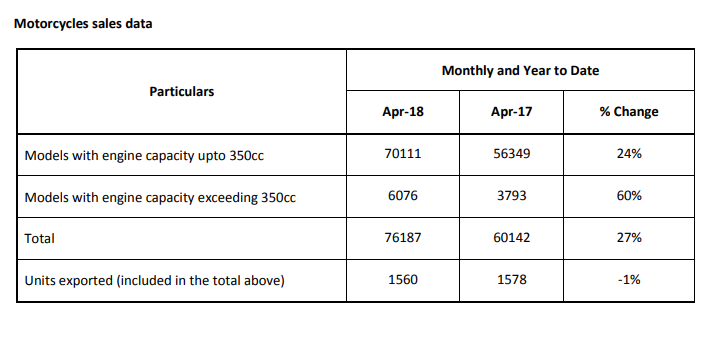

April 2018 MotorCycle Sales:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7b3553de-4803-42ff-bd89-bbfa6954d314.pdf

OutcomeBM.pdf (2.8 MB)

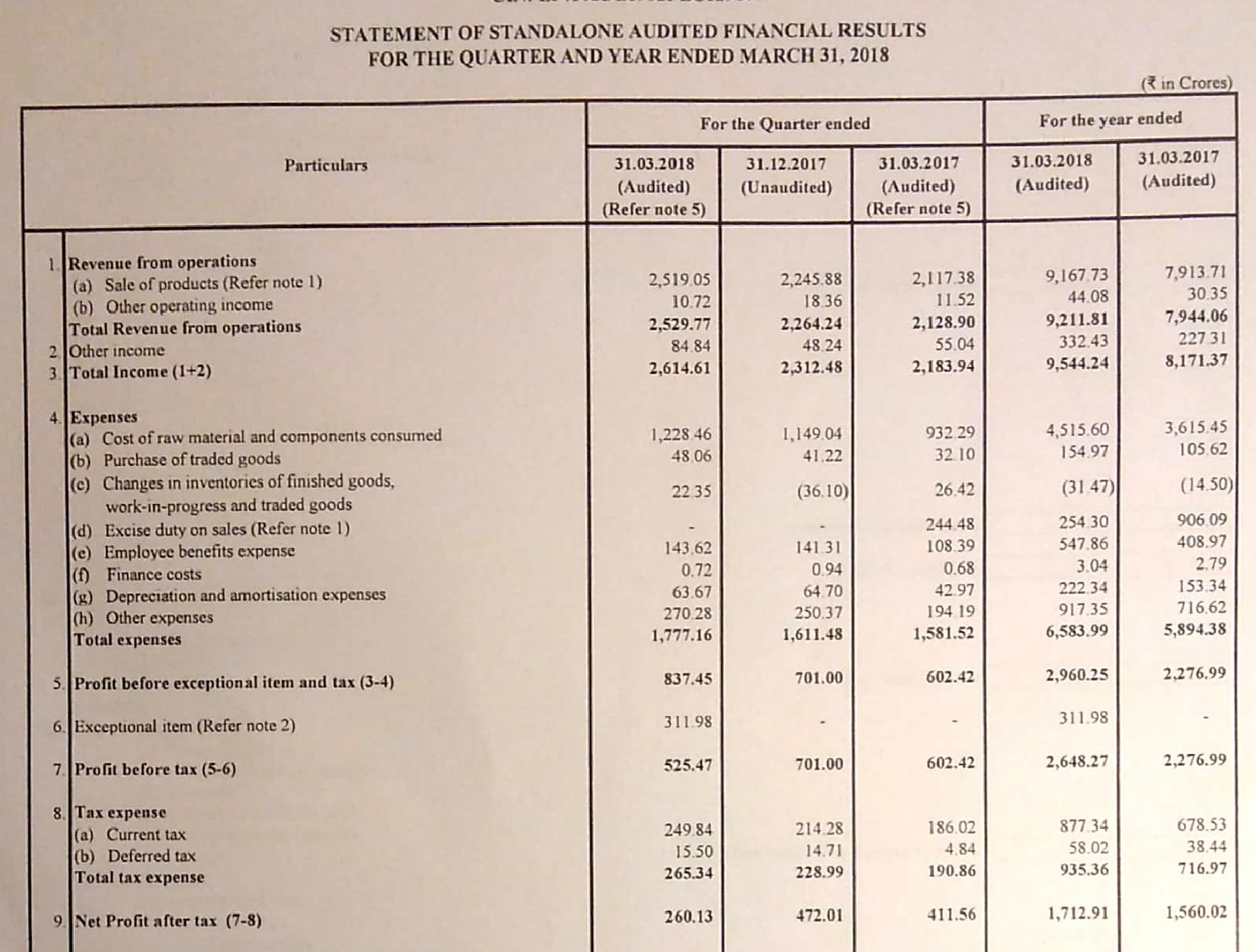

Standalone numbers:

Good results which has became flat because of the loss booked for closing down Eicher-Polaris (Multix) operations.

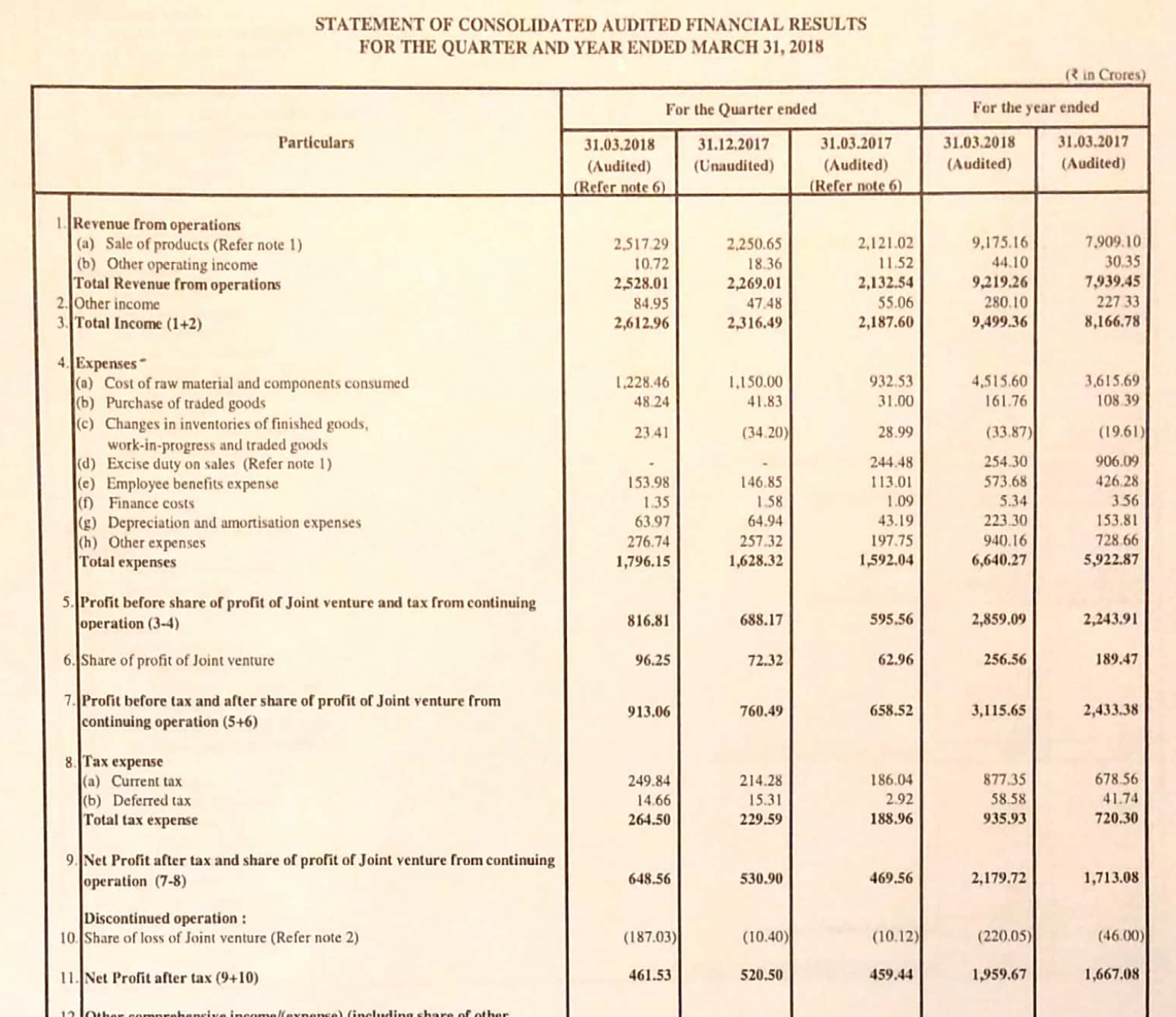

Consolidated numbers:

In case anyone’s interested:

RE out with another variant of the Classic. This one is a limited edition, so definitely will add ‘Collector’s value’ to its owners.

These little variations they are doing on the Classic are really helping them up their margins as their ASP increases with no real added costs. All their latest variants - Redditch, Gun Metal Grey, Stealth Black and now Pegasus are helping in this.

Even the Thunderbird X is doing something similar for them.

Old wine in a new bottle strategy is working well for RE at the moment. And the marketing of these bikes is top notch too!

The RE story has not matured yet IMO.

Look at the BS data - negligible receivables & inventory, substantial customer advances. This shows strong demand momentum from market, which i believe should continue for 2-3 years atleast.

After that even if demand stabilize, it willstill be a cash cow with highest margins in auto segment.

Working Youth mentality transitioning from utility bikes to Big Brand bikes (same as iphones). People willing to spend more, adopting biking as a way of life & good road infra is another positive for whole auto segment, even Eicher CV segment will benefit.

This is how I look at it. There are very few companies in India that are looking to capture the global market with a unique and loved brand. Brand being the operative word.

RE has the stated ambition to be the global leader in middle weight bikes globally. If they are successful in capturing the global market over the next decade, I see the growth continuing and the valuations for the company sticking. They have started in the right earnest here and are aiming to have a run rate of exporting 50-60k bikes each month globally over the next decade.

And during this period when they are establishing their footing in the export space, they will continue to grow in India. Quite a few trends to support this - low penetration of RE in many Indian states. Considering the RE story started some 5 years ago - a lot of older RE bikes are coming up for replacement by their owners in the next few years, so newer variants of existing bikes and new launches should help here. Accessories as a business is still to hit scale, I’m sure it will over the next 5 years. If Maruti can sell so many cars and keep growing and are investing more to grow even further - I don’t see why RE can’t keep growing too (I make this comparison as both have dominant market shares in their own respective categories).

All in all, India doesn’t have too many companies and brands that are trying to compete at the global level. Here we have a solid Indian brand trying to do the same (with a more than able and competent management). I’m more than happy to bet on a company who sees the world as their market (with India being a core part of this strategy) as it is such companies that tend to do really well - think of Apple, Coke, Suzuki, Toyota, VW etc etc.

Disc: Invested and quite excited by the brand and both its Indian & global prospects.

Nicely explained!

i would like to add, there’s another part to RE story - VECV

This segment of Eicher is also poised to benefit majorly. Eicher is a moderate player in CV segment. With Road infra improving, implementation of GST(lesser road barriers), migration from railway(hardly improving) to road for goods Transportation… all these will favor CV co.

So its like hitting two birds with one stone.

Hi

One of the bikes of the yesteryears will make a comeback soon. This certainly will dent some bullet sales if executed well.

Rgds

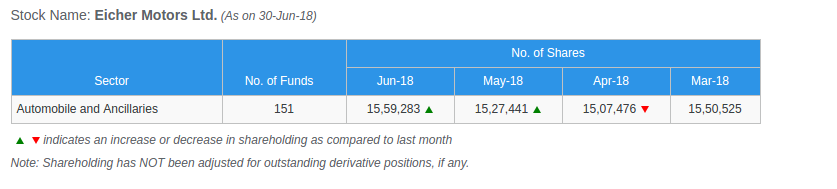

Mutual Fund Holding of Eicher Motors has shown a increase in the month of June.

Source : https://www.rupeevest.com/Mutual-Fund-Holdings/105200

Q4FY18 Concall:

Financial Highlights of EML

• For the quarter, the net revenue of the company is Rs 2,528 crores which is a 34% growth. The EBITDA is Rs 797 crores, a growth of 36% for the quarter. The EBITDA margins have gone up to 31.5%. PAT is Rs. 462 crores a flat growth over Rs 459 crores last year. Flat growth in PAT is due a one-time impairment of Rs 187 crores due to the closure of Eicher Polaris business.

• For the year, the net revenue of the company is Rs 8,965 crores which is a 27% growth. The EBITDA is Rs 2,808 crores which is a growth of 29%. PAT is Rs. 2180 crores which is a 27% growth.

Financial Highlights of VE Commercial Vehicles Limited (VECV)

• For the quarter, the revenue is Rs. 3,300 crores, which is a 30% growth. The EBITDA is Rs. 315 crores, which is 51% growth. The EBITDA Margin has gone up to 9.5%. The PAT is Rs. 177 crores, which is 52% growth

• For the year, the revenue is Rs. 10,223 crores, which is growth of 17%. EBITDA is Rs. 905 crores, which is 33% growth. The PAT is Rs. 472 crores, which is 35% growth.

Segment-wise business updates:

Royal Enfield

• For the quarter, 2.26 lakh motorcycles were sold, which is a 27% increase over the same quarter last year. And for the year, 8.2 lakhs motorcycles sold, which is a 23% increase.

• 825 Domestic dealers and internationally 36 exclusive dealers, and 540 overall including all multi-brand dealers at the end of March 2018.

• Started a new store in Buenos Aires in Argentina for the first time last quarter

• Showcased new twin motorcycle to the world - the interceptor 650 and the Continental GT 650. They will be in the market this year.

• Excellent tractions for new Variants – BS4 compliant Himalayan Sleet and Explorer Kit and the Thunderbird X.

• Initiated new retail formats in the form of ‘Garage Café’. First Café opened in Goa. It provides environment for people to experience the brand. The company is working on expanding ‘Garage Café’ model in the future.

• Initiated a new pre-owned motorcycle store format, “Royal Enfield Vintage” where pre-owned, restored, refurbished motorcycles will be sold. The first outlet is opened in Chennai. This is a Franchise-model. Revenue of Pre-owned business will not reflect in the company’s revenue. It gets reflected in the dealer’s revenue. The Company plans to open ten more stores this year. Based on their performance, in the next ten years, the model will be scaled up to National Level.

There are many objectives for pre-owned motorcycle business, such as:

o to give customers a really good experience of buying a pre-owned Royal Enfield by pushing quality in the entire pre-owned motorcycle supply chain.

o maintaining strong residual value of motorcycles because resale price of Royal Enfield is an extremely important purchase criteria

o driving existing 350-cc customers to higher cc motorcycles – the twins. This is a great place for the customers to dispose of their single to buy twin

o new earning source i.e., spare parts

In the lines of Siddhartha Lal, Pre-owned motorcycle model “is not going to be a huge revenue spinner or profit spinner for Royal Enfield, but it’s more for brand and consumer experience”

Domestic Strategy:

One month in the last quarter, UP was the number one market for Royal Enfield. Over the next five to ten years growth opportunity in Royal Enfield will be from under-represented states (UP, Bihar, Madhya Pradesh, Rajasthan where Royal Enfield has 2 to 4% of the market share of all motorcycles).

Top down strategy of market penetration will be continued for improved market share in these under-represented states. First targeting the big cities - having a very strong distribution and multiple strong dealer points in big cities, creating the franchise, creating an interest and demand, create the ecosystem then fanning out into the smaller satellite towns and then going to the next level towns.

International Strategy:

Europe is still biggest market by far, but the growth opportunity is not as tremendously high, as in Thailand and Indonesia. Currently, the company has three stores in Indonesia, two in Thailand. These countries are the ones that’s most right for the growth story that company is looking for. Therefore more energy, resources, capital, team members will be put in these countries.

Apart from these two countries, currently the company is cultivating Latin American market for entry in the next one to three years. Ambition is to be a global brand.

Future Investments:

• New Chennai Tech Centre some part of it will be ready by this calendar year, and the rest of it by early next financial year.

• Rs. 800 crores capex for 2018-19 for Phase 2 of Vallam Vadagal plant near Chennai. The new Phase 2 of Vallam Vadagal plant will result in an annual production of 9.5 lakhs for the financial year 2018-19.

In the next 24 months, other than the new capacity additions, the focus area will be improving capacities through better productivity by better machining rates, lower rejections

VE Commercial Vehicles Limited

• In the quarter VECV grew by 33% versus the industry growing by 21%, outpacing the industry again

• Annual volumes were at 66,000 units in 2017-18 versus 58,000 units in 2016-17

• In comparison to last year, market share have been slightly lower in light and medium duty trucks (5-15 tonnes) and slightly higher in heavy duty trucks (16-49 tonnes).

• Notwithstanding the enormous pressures on discounts in the market, market share is flat

Future Investments

• An additional Rs 500 crores in capex in this year 2018-19 in VECV

Article says they are looking for Bike maker in Asia. TVS has tie up with BMW and Bajaj with Triumh. So this makes sense for Hero moto corp.