This is from Polaris’s Q2 filings

Scroll down to page 22 for finding specifics on Multix

http://ir.polaris.com/files/doc_presentations/2015/Q2-2015-PII-Earnings-Presentation-F.pdf

Key takeaways

MULTIX

Multi-Role Personal Vehicle

3 models to start

511cc diesel engine

MSRP ~ $3,600 - $4,500

Street legal in India

~30 dealers at launch

>200 by 2020

Start of production end of July 2015

Target market potential >60 million people

Small/micro business owners in India

Signed July 2012

50/50 Joint Venture in India

$27M Polaris investment to-date

Factory in Jaipur, India – 200,000 sq. ft.

JV expected to be profitable by 2018

1 Like

I also like the second slide in the presentation where with CEO 31 experience, they also indicate share price growth during his tenure with the company.

Coverage in ET today

Great Show by Eicher on RE and CV front.

On analysing number in details. Undestand that growth in RE is more in <350 CC as against >350 CC,

While in CV case, Bus segment has shown marginal growth with higher growth >16 tonnes trucks has almost double during September 2015.

My assumption is Volvo Truck >16 Tonne Eicher truck has better profitability and realisation vis a vis LCV and Buses. If anyone has view about same, please share.

Thanks in advance

Here are the filings

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/75749BF2_4454_4E5B_8A21_6C5B7BB00D0D_112820.pdf

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/A7647781_883D_4642_8D6D_F59CAF2F7347_120734.pdf

Eicher makes trading margin on Volvo trucks…so you are right on the realisation front but profitability will be lower.

updates on Green tax and traction on VC volumes during Sept

Royal Enfield opens showrooms in Madrid, Paris

1 Like

Eicher Motors: Royal Enfield’s volumes are expected to improve 55% y-o-y in Q2FY16 (Motilal Oswal via IndiaNotes.com)

Highlights:

-

With continued higher demand momentum, Royal Enfield’s volumes are expected to improve 55% YoY (19.6% QoQ) and margins are expected to remain strong at 27% (+200bp YoY).

-

We expect VECV’s volumes to grow ~19% YoY (decline 3% QoQ) on economic revival and higher fleet operator utilization, leading to replacement demand. VECV margins are expected to improve by 110bp QoQ to 8% on account of operating leverage benefits.

-

We anticipate ~36% YoY (6% QoQ) growth in consolidated revenue. Consolidated margins are expected to be 16.2%, up 280bp YoY (240bp QoQ). Consolidated PAT (after minority) would increase 61% YoY (~20% QoQ) to INR2.6b.

-

The stock trades at 52.7x CY15E and 29.9x CY16E EPS. Maintain Buy.

Key issues to watch for

- Update on demand and waiting period for Royal Enfield.

- New launches and timelines under Royal Enfield business.

- Update on current CV demand trends, discount levels and channel inventory.

1 Like

VECV sales encouraging for the Oct Month.

Royal Enfield on its Royal Growth Path.

Today facebook showed me this adv. about a dealer selling Royal Enfield close to Taipei (I live in Taipei)

https://www.facebook.com/RoyalEnfieldTaichung/?fref=ts

Makes me think, that the brand is travelling to places where company hasn’t even started selling officially. This is very promising development. Helps to seed the idea/culture and fan club around it.

It’s selling for almost 4x of India price, but Taiwan is known to have atrocious tax rates for bike imports so that could be contributing to it.

Taiwan has a huge leisure bike riders market. Mostly dominated by BMW’s, Harley,Triumph’s of the world.

This is really setting the stage for something very interesting.

Make me very happy !!

3 Likes

Eicher Motors Results out. Awesome!!!

The icing on the cake is the margin expansion of 200bps in EBIT from 10.9% to 13%.

The Standalone looks even more impressive -

margin expansion of more than 200bps from 23.4 to 25.7%.

The board has in principle approved taking the capacity of Royal enfield to 9 lac bikes by 2018. Current capacity approx 52000 bikes per month. comes around to 75000 bikes per month.This is double from the 4.5 bikes targeted for sale now. Strong demand and swelling orderbook.!!!

The good part is the VECV has turned around this year after few years and has grown with the Heavy duty trucks growing the highest. LMCV also shown growth. Buses has been a drag.

Lot of activities on the export front. The new Store in US to be opened in the H12016. US subsidiary headed by Rod copes.

2 Likes

I attended conference call. The decline in Waiting period for Royal enfield was main concern due to which price have declined. At current market price, the stock is trading at trialing Twelve month PE 55 (EPS Rs 305) of around TTM profit growth of around 48%. I find stock attractive but given the significant decline in market, I would not be suprised if stock goes down below 16000/-.

Discl: I hold Eicher shares and my views may be biased. Investor shall do their own due diligence before investing.

2 Likes

Any update on Multix?

Concall Details in brief:

- Expect to sell in FY16 - 6.2 lac RE motorcycles.

- New model to be introduced in FY16 and another one in FY17.`

- Total 9 lac bike capacity by FY18. This includes availability for the year and not end of the year.

- Major overhaul in the design of the retail stores. Total 500 dealer/stores this year target and 5 stores/dealer average each month next year.

- More emphasis on"Soft-Sell" than “Hard-Sell”.

- Infra and hardware set up for the process. Huge benefit accruing because of this new design format. Able to attract huge footfalls when compared to “Traditional” Stores and also enabling to convert to Sales thereby increasing the orders!!!

- FY17 bike selling target between 6.2 and 9 lacs. i believe they should do 40% volume growth.

- Vallam Vadagal plant expansion going on. Oragadam will fuel the next leg of growth along with Vallam Vadagal. Tirivattiyur will be providing the exisiting functionalitites as is.

- 60% of sales happening from Top 20 cities rest 40% from others.

- There has been huge traction in the Tier 2 and 3 citites. Small towns which were selling 10-15 bikes are now seeing sales of 20-30. Hopeful of this growth going on…

- 10% of sales from first time users and youngsters. This was 1-3% few years before. This when converted is a massive growth. 3% on 3 lac sales in Fy14 comes aroung to 9K. This has moved to 40K-45K which is 10% of 4.5 lac this year.

- Huge work going on in the international market. US will have the first roll out from Wisconsin in H1 FY16. 2nd store opened in London. Madrid and paris also have RE stores now. Increased store count in colombia. Also entered Indonesia.

- Good growth in HeavyDuty vehicles. Light and Medium duty CV also recorded growth.

- Raw material cost has come down for RE especially since the falling commodity cost made to good use. Not so much when for VECV when compared to RE.

- Very much hopeful of replicating the success of India in developing markets like Latin American and South east Asian since there is a huge scope and huge market.

- There can be success like india, some markets may be not so successful and some markets may be better. The actual turnout will be clear after 5 years and all steps being taken to ensure success.

Export markets segmented to - developing nations and matured/developed markets.

There is a huge gap between 250-750 cc market and in the range of 3-4k dollar. Very less options available in this market and the company trying to fill this.

The waiting period is in the range of 1-4 months depending on the motorcycle models and has been reduced from 9 months in the peak time few years before and this is what company had also intended.

Overall liked the honesty, confidence of the management where they were even open in saying that there can be failures in some market , success in some markets like in India and there could be even better success than India in some markets.

FY16 will be a consolidation year. They want to increase the production to 50-52K per month average and will not be a straight line growth but skewed more to the end of the year with higher production. They want to stabilize the production/procurement/supply/vendor management first and then take it higher. Capex required will be clear in Feb annual meeting.

Disclosure: Invested. Investors pls do the due diligence before investing.

7 Likes

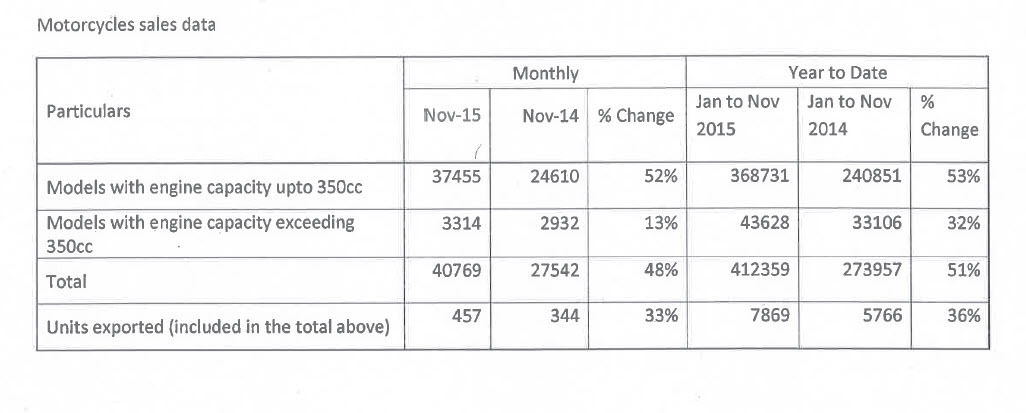

Chennai rains haven’t dampened anything

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/C1475C00_AB7E_4998_982D_A5E8B6D14219_103231.pdf

RE chugs along fine

52% M on M and 53% Y on Y

2 Likes

Find enclosed a good presentation updated in November 2015 by Eicher. I really love this. Hope you to enjoy this,

On monthly number, Last year diwali was in October while current year it was in November 2015.

In September 2014, RE sales was 28,020 which declined to 26,039 in October 2014 (-7.1%, MOM)

In October 2015, RE sales was 44,522 which declined to 40,769 in November 2015 (-8.4% MOM).

In Jan to November 2015, total sales is 4,12,359 which assuming even 40,000 sales in December 2015, would exceed 450,000 units for CY2015.

Let see how CV number get unfolded.

1 Like

You are at speed which meet BSE filing by the company. Do you share your server with BSE

Also, personally would look at total sales then only domestic sales, growth in which case marginally lower then domestic sales.

November 2015 presentation by the company to investor

1 Like