Deepak Mittal of ECL Finance- Edelweiss briefs the $250 mn CDPQ investment deal

1 Like

Agree with the conclusion that Edel is cheap but why do you need to do the evaluation on FY18 basis. We are at the end of FY19 now. They have 5k cr book value currently and conversion will be at least 2 yrs down the line. Assuming 20% ROE and growth in book value gives me 2x book value at the time of conversion. Nothing compelling for Edel shareholders as such. Still it is very important that they are getting this cash at the time when industry is having liquidity and capital issues. They can hope to acquire some new verticals and also not hit the capital market for 3-4 yrs. This is a counter cyclical investment and could turn out to be a masterstroke if executed well.

Disc: Invested

1 Like

You could check the ppt they have provided for basic calc. This acquisition also involves internal restructuring and simplification of lending businesses. Pro forma business they are getting investment has 5k cr of book value as of Dec 2018 that’s why using FY18 nos. is not useful for calculation.

2 Likes

Hi

The right way of calculating what CPDQ is paying is as follows:

INR 1,800 Cr. (USD 250 Mn) investment is first in tranches -

Tranche 1 - Rs.1,100 Cr. (USD 150 Mn) right away

Tranche 2 - Rs.350 Cr. (USD 150 Mn) at the end of year 1

Tranche 3 - Rs.350 Cr. (USD 150 Mn) at the end of year 2

The investment would mostly in form of CCDs and carry a coupon for sure.

CPDQ would further have an option to convert at the end of 2 to 5 years (so i don’t think they would convert right away - unless share prices runaways)

Current Book Size is Rs.5,000 Cr. and assuming a mid teen ROE (overall ROE going forward shall come down so 15% - it actually can be a bit lower also as the most profitable business is the ARC which is not included)

| Year | Book Value | 15% Stake | P/BV |

|---|---|---|---|

| 0 | 5,000 | - | |

| 1 | 5,750 | - | |

| 2 | 6,613 | 12,000 | 1.8 |

| 3 | 7,604 | 12,000 | 1.6 |

| 4 | 8,745 | 12,000 | 1.4 |

| 5 | 10,057 | 12,000 | 1.2 |

This does not include the interest payment on the CCDs. I don’t think the CCDs would be invested at less than 10% and further I don’t think CPDQ would convert before the end of 5th year.

The deal is good as it ensures survival - hope they learn from their mistakes and grow (their real estate wholesale book has been managed very badly and market rumours are not very kind)

1 Like

Good analysis but few things to keep in mind. These CCDs generally carry USD interest rates not Indian ones so NIMs would expand for the retail segment. Still the conversion might not be more than 2x BV. Their current retail lending ROE is suppressed due to investments they are making.

I keep hearing about their real estate book but so far there is not a single blow up to create a big concern. Additionally, reduction in GST and recent tax rules for real estate sector will lead to recovery over the next 12 months. Unlike PEL, it has stayed away from luxury/very expensive housing. They are much more granular to cause any significant trouble. Its RE book was started 10 yrs back and is more seasoned than some recent ones like PEL. However, it will keep suffering perception issues for the foreseeable future as long as the RE sector doesn’t recover.

5 Likes

Hi Sumit

Working in corporate finance I am sure these CCDs would not carry Dollar Interest. They are investing in India - they would 100% ask for minimum 9.25% p.a.p.m. interest rate for a AA rated company.

Real Estate Book quality actually sucks - they have lended money to a lot of Tier 2 builders which are under tremendous stress.

Even though I don’t want to deflect this discussion to Piramal here - I would like to add they are a different beast - it has lended to the big guys and you don’t want to be defaulting on him (unless you want to close your real estate business as you would not be able to borrow again if you default on him, plus he has his construction arm which gives an edge which nobody values). Edelweiss does not have that edge.

Edelweiss is a good company and should be a long term compounder. But lets not let the valuations run away.

6 Likes

thanks for your perspective! we would know in due course may be in 2 more quarters what is the kind of actual hole in the balance sheet due to RE lending.

Another interesting development. Race for creating liability franchisee is on. Among three quoted here only Edelweiss will be an acceptable candidate to RBI if at all this happens.

3 Likes

4 Likes

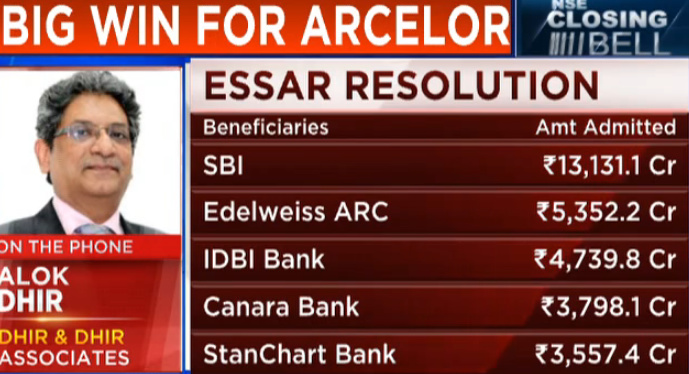

Four creditors with the largest exposures, namely Edelweiss ARC, State Bank of India, IDBI Bank and ICICI Bank, are part of the core committee that is taking the call on the behalf of lenders as the committee of creditors (CoC) has been technically dissolved after a decision to award the bid to ArcelorMittal was taken.

ArcelorMittal’s Resolution Proposal involves financial creditors getting Rs 41,987 crore out of their total dues of Rs 49,395 crore. Operational creditors, under the plan, would get just Rs 214 crore against the outstanding of Rs 4,976 crore

According to ArcelorMittal plan, Standard Chartered will only get Rs 60 crore against its claims of Rs 3,187 crore from Essar Steel.

3 Likes

adding another link… CDPQ giving very strong vote of confidence when they count Kotak, HDFC, Piramal and Edelweiss in the same league…

1 Like

2 Likes

The latest ICRA credit rating report makes for a really interesting reading. https://www.icra.in/Rationale/ShowRationaleReport/?Id=79354

They’ve tried to detail a case for downgrading the outlook from Stable to Negative, but in the process, actually talked about why Edelweiss should be able to thrive.

Edelweiss & most of NBFC had structural tailwind from period of 2012 to 2017 because of problems with PSU and corporate banks . This structural tailwind has completed its course and now is headwind for NBFC .

Most banks will try lending directly rather than through NBFC . This will mean higher competition from low cost players ( as banks have access to saving deposit which pays only 3 - 4% interest rate ) . In commodity business - low cost player has huge advantages .

The only difference that helps besides cost in lending business is CULTURE - Conservative culture . Hence cycle after cycle HDFC becomes stronger …

All new age NBFC are aggressive - one can see how many mistakes they make in bull market - This is cultural issue . Such companies will repeat these mistakes in every cycles … and get beaten up …

So one needs to be careful in paying up for NBFC . esp when P/B > 1 . and book value itself is subjected to lot of doubt due to potential NPAs

3 Likes

Although you have generalized for NBFCs, because you have posted your comment on Edelweiss thread, I checked the price movement of Edelweiss from 2012 to 2017 (tailwind period that you mentioned). Despite the tailwind that you mention the price of Edelweiss moved from aprox 35 to aprox 55 during that period. That price change might hardly point to any tailwind. The big move in price came only after 2017.

Point I am trying to make is, prices might over react and under react massively as compared to the larger macro moves in the industry and sometimes even a company.

The structural tailwind is for business … and not stock price which is dependent on other factors

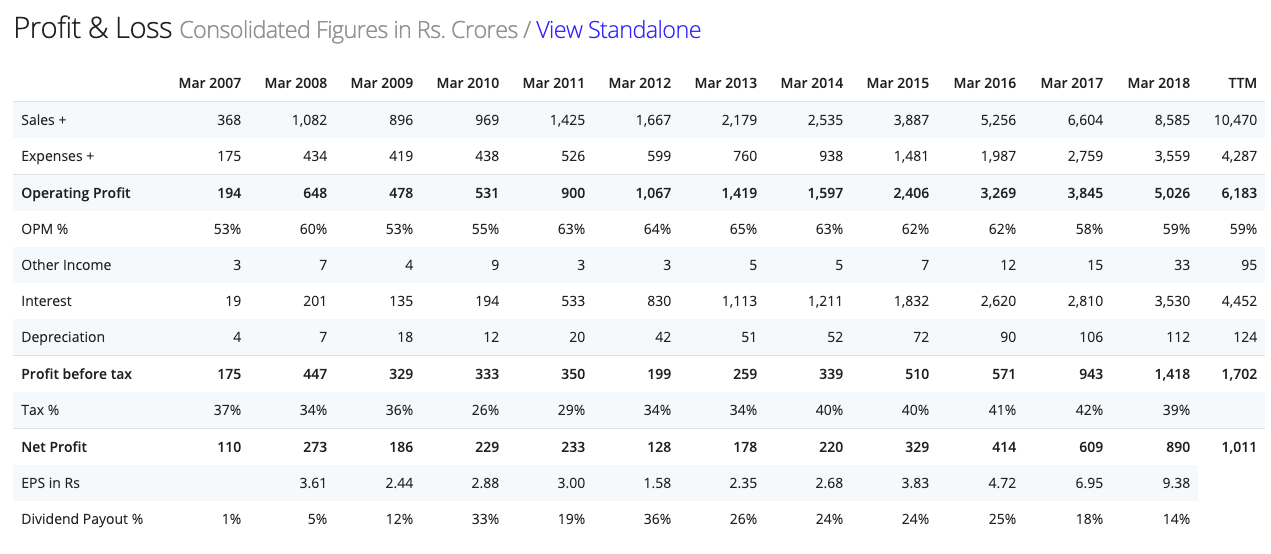

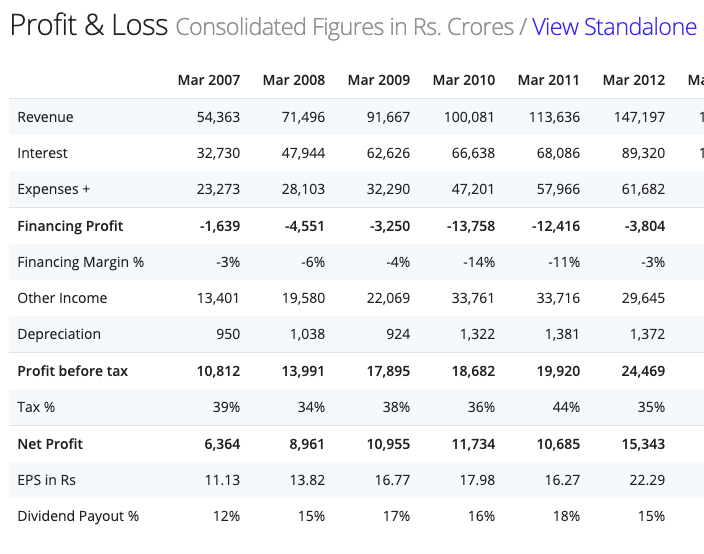

The Net profit of Edelwiss moved from Rs 128 cr in Fy 11-12 to 900 crs in FY 17-18

Also look at business growth from 2008 to 2012 - It was flat to negative …

Why becos at that time PSU banks were growing at brisk rate . Most PSU banks double their profits in this period and they were actively taking away share from NBFC and other banks . You can see from following comparative snapshots

Edelweiss

SBI

We need to understand there are some sectorial trends that help individual companies . This trends play for 4- 5 years on both sides ( on upside and on downside )

The above is analysis is for business - How stock price will move I have no clue …

4 Likes

Edelweiss long-term median P/B is around 1-2x. This during a period where the company was performing reasonably well in terms of accounting profits.

What happened post demonetisation looks like a pump-and-dump operation (Edelweiss is not alone here) where considerable dilution happened at elevated valuations. Exactly around a year post demonetisation (Q4, FY18) the mean reversion started and has been going on since. Even current valuations are expensive IMHO.

I looked at some of the subsidiaries finances along with @diffsoft sometime last year and what we saw was quite convoluted in what looked to me like circular lending among subsidiaries - especially among Edelweiss Commodities, Edelweiss ARC and ECL Finance. I continue to stand unconvinced about this business.

8 Likes

You might be doing a wrong comparison. Edelweiss had large capital market subsidiary which restricted its earnings growth during weak years of 2010-13 while they were also incubating other businesses. Their lending business still grew handsomely on a smaller base during the period you have taken for comparison. Regarding the current slump - it is a combination of liquidity issue and capital market weakness. A good portion of their earning still comes from verticals related to the capital market. A better comparison would be with IIFL or Motilal to an extent.

I am not doing a comparison of Edelweiss with SBI , but trying to state the point how sector performance impact firms performance and how sectors within financials move across in business cycles . ( pl read my last two posts - you will understand the context )

So while 2009- 2012 was PSU Banks era - when most PSU banks did pretty well on business and stock prices , 2014- 2017 was NBFC era when most NBFC did well on both business and stock prices .

We have to remember after a great performance for 4 -5 years the sector undergoes price and time correction for 4-5 years .

There are very few exception to this -

1 Like

I have thought hard on this topic. What if SBI and likes actually start to grow again. What if they catch up on digitalization. They have strong advantages that can’t be ignored. And then there’s mean reversion.

BUT, having seen some of these guys up close, I don’t think they will get a sustainable shift in business. Mind you, 1-2 years hyper growth can happen but not sustained. Simply because SBI and likes are poorly managed businesses with undue oversight from govts and no incentive for performance.

So my bet would be edelweiss, equitas, ujjivan etc.