SBI cannot be compared to these small niche entities . Ideally SBI needs to be compared to ICICI and HDFC

SBI is like Financial sector Mutual fund -

SBI has largest share of home mortgage higher than HDFC . It decides the market rates both for deposit and loans .

SBI has second largest share in cards and one of aggressive player in the same .

SBI is one of largest corporate and retail lender

SBI has huge AMC and its fund has moat that Government pension entities tend to prefer them over others . This gives them huge anchor base to lower cost as compared to others

SBI and other PSU have new moat of increasing pension payment float and direct transfer float .

This enables them to reduce cost …

The ONLY problem with SBI was Govt interference in loans sanction .

If this gets eliminated SBI & many PSU banks can be tough bank to beat as they are hardcore conservative , have low cost structure and excellent distribution network .

Even if PSU banks grow at market or even slightly higher than market for any time period - all NBFC and small private banks will lose out - They just can’t compete …

Yes large private banks may survive as they have diversified depositor and lender base …

I think the mistake we are making here is that we have somehow reached a conclusion that that if banks would grow then NBFCs can’t or won’t grow.

Fact of the matter is NBFCs cater to a different market or Borrower needs which a Bank cannot cater too. Ex - Loan Against Shares, Land Funding, Promoter Funding, Structured Deals etc. (For Banks as per RBI Regulation cannot fund against shares or fund land, they have restrictions in scheduling repayment structure etc).

Obviously NBFCs can’t grow as they were growing during the last 3/4 years as Banks had stopped lending and NBFCs were looking to grow their book for valuation purposes. (its not the fault of Edelweiss to raise capital when share prices are high).

For India to grow NBFCs have to grow and I am sure they would grow at a good clip (15 to 20% ) but obviously not at 30 to 40% growth rate. The ROE would remain healthy and good NBFCs would gain market share (their is a clear edge in terms of cost of funding for top NBFCs and Edelweiss is among the top names)/

General consensus for the last many years has been that business will move from public sector banking institutions to private sector banks or private NBFCs. Stress on the word general consensus! NO ONE believes that PSU banks will grab private financial insitution’s business over the long term.

Govt might re-cap the PSU banks now (and the stocks might bounce up) but they will be back to square one in couple of years as they cannot change the culture and sooner or later one govt or another will arm twist them into giving loans that should not be given.

I doubt private financial institutions have to worry about Public Sector Banks.

PS: I am sorry this post was not related to Edelweiss but then last few messages were generic enough to warrant this reply.

Hi - you are looking at loans in Retail section in corporate they would not fund and even in Retail the charges quoted by Banks for these loans are on the higher side (and not as low as they quote normally) and the delta between an NBFC and Bank becomes thin.

I personally have taken a LAS from Bajaj Finance which was offered at 50 bps higher rate than SBI with whom I have a demat with but due to service offered took the loan from NBFC.

Same is true for a lot of retail lending where due to better service it makes sense to take loan from NBFC.

RBI rule clearly prohibits Banks to lend against shares whereas NBFCs are allowed to lend against shares. Banks are lending only to retail against shares (which also maybe through other subsidiary companies, I would get back to you after speaking to friends working in banks).

The article just talks about value of shares being pledged to Banks - which they can take as additional collateral but they cannot lend against shares and also some of the shares can be for retail.

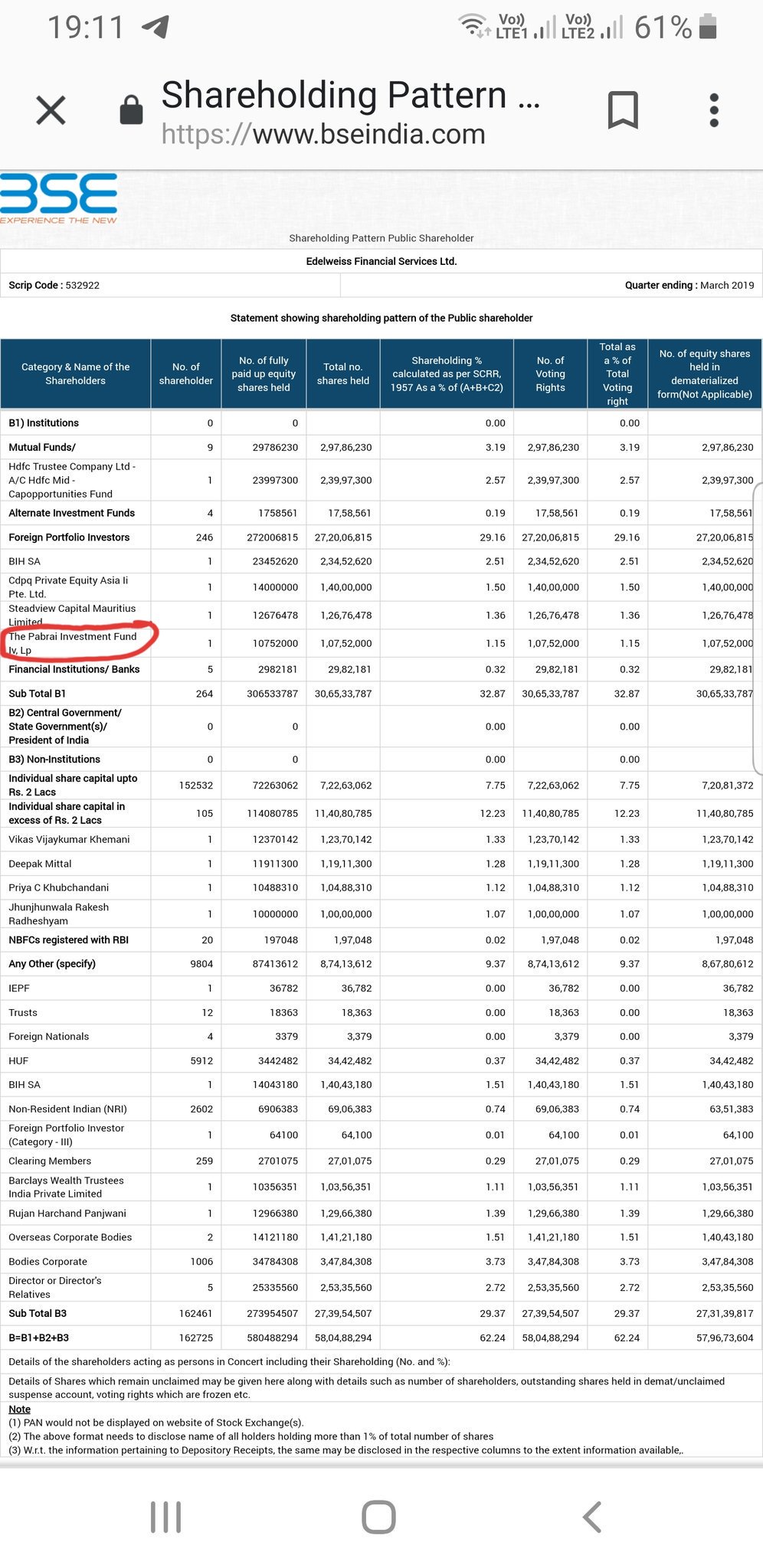

Sorry to put this information here - but i just could not stop comparing these two information

Edelweiss Reported its highest profit of Rs 1400 crores ( PBT ) and 890 crores (PAT) crores in 2018 …

In comparison - a small insignificant unit of SBI growing at 30% + 800 crores- Uses latest technology & fintech tools - Again if NDA past track is observed PSU can gain significantly under their rule.

From ET news …

“We are using chatbots, artificial intelligence and robots to do our repetitive jobs,” said Hardayal Prasad, CEO at SBI Card. “We are preparing for a card less world. In the last 18 months since GE has exited, we set up our own infrastructure and brought back our core platform to India without losing sight of growth. We are growing at 31% in terms of number of cards against the industry growth of 25%. We have gained market share and now have 18.3% in terms of spends.”

Prasad expects the company to clock a profit before tax of more than ₹1,000 crore in the fiscal year ended March 2019, up 20% from ₹776 crore reported in fiscal 2018, riding on rising card sales to the open market outside SBI branches.

Size is not a factor as long as we are not talking of small players. So, I don’t care if SBI is big or not. What I care about is whether they can grow and can they do it profitably.

Both top and mid management leadership at many large PSUs is so poor that one wonders which world they live in. For example, I witnessed one senior guy in a large bank put a plan to capture retail payment market and I was so hard pressed to remind him of the elephant in room viz paytm.

I firmly believe in metrics driving behavior. A leader in a PSU is disincentivized to take risky or aggressive bets. He always has to look behind his shoulder whether a CAG report will send him to jail. And he gets zilch if his bets pay off. Why on earth would someone like that work hard and drive business? And to top thst, a babu in lutyens will keep reminding him who is the boss.

While some catching up has happened in technology, I don’t think people appreciate how radically the open banking world would be… All the advantages of being an incumbent would go away. That’s why Asia’s best bank DBS calls itself a tech company!!! Please read about their GANDALF strategy.

DBS was public sector bank that transformed itself . In financial services sovereign support is very BIG deal and size + diversification is important …

Now coming to being tech savvy …

We should look at NPCI ( public sector ) product - UPI and RuPAY … These have become market leaders in their category and shaken BIG MOAT players like VISA and MASTER CARD , all this in matter of 4 years .

SBI or other PSU - Management will be dumb is in the price - so any shifts will mean huge re rating .

But in case of private sector financial services - like Edelweiss or Piramal - they are expected to be smart - That is in the price - So any dumb decision will lead to huge de rating … That is what happened in Oct 2018.

But the whole discussion was on NBFC as sector - this sector should see price / time correction for 4 years - That was my view - we got distracted in PSU and NON PSU … I would like end this thread here …

'But the whole discussion was on NBFC as sector - this sector should see price / time correction for 4 years - ’

Why do you think that is the case in general (not NBFC in particular). Is it that in cases where this has happened it is due to the change in the economics of the industry / structural changes for the worse ? Real estate, Infrastructure, pharma etc seem to fall in that bucket. IT services in 2000s did not fall in that bucket and was due to extreme (3 sigma+ valuations).

Any reason by the NBFC business model has changed structurally in the last one year ?

Competitive Intensity : PSU banks & Corporate bank being back into action will increase competitive intensity in the sector .

Supplier Power : Credit to Deposit ratio for most banks is increasing , With recent incidence Debt Mutual funds inflows have reduced … This means reduction in money that can be given to NBFC for lending . Competition and cost of capital will go up even for good NBFCs

Customer power : As credit scoring improves , with Jan Dhan ( aadhar linked accounts ) & higher adoption of fintec by banks - they will not like to use via NBFC route to go for lending . There might some niche areas which banks may avoid but large segments like Housing , auto financing , durable financing, even loans etc can be taken over by banks . The niche areas like MFI loans in deep rural , loans to risker asset class ( like real estate developers , unsecured high risk loans , some SMEs ) etc will be continued to service by NBFCs .

Substitution : New players esp fintech can provide alternatives or increase customer bargaining power through comparison & commoditization of products . This will reduce profit margin of many of products without dramatically reducing risk

I am not trying to debate, but trying to understand your points better. so here goes

a. competitive intensity: Why do you think this has really changed ? NBFCs operate mostly in the retail segment and even though PSU could not grow the book, they had the option to reduce the corporate book and grow the retail one (while keeping the total book same or even shrinking it). PSU have a better CAR or lower NPA, but that does not impact the lending/underwriting for the retail sector. Has anything changed for them at the local level to improve this ?

b. supplier power : Has this not always been the case ? Any NBFC, MFI etc has always been disadvantaged compared to PSU and other banks. This is partly balanced out by the SLR portion. Inspite of this NBFCs have been grown all these years (even before the recent spurt). I dont think the differentiator for most NBFC was the rate of interest in any case ?

c. Customer power : Credit scoring, Fintech and other such data driven options are available in most developed market. Inspite of this niche financial players have flourished for different reasons. Why would NBFC not be able to adopt the technology and use it to their advantage too ?

d. substitution : Again this is more developed in US and china, and the private/ nimble players have adopted this better than the larger banks.

My reason for listing the above is to try to understand what has been the change in the competitive dynamics for the NBFC sector as a whole versus the PSU/Large banks. I am really not able to find a new factor. Deposit cost has always been a disadvantage, which NBFC have compensated via operating in niches, under writing better and have better distribution and service standard.

I am not trying to come up a reasoning for the recent drop in valuations which may or may not be justified. What i am trying to understand is what has really changed in the financial services space that will allow the PSU banks to regain their competitiveness.

Same information can be viewed differently depending our own experiences .

Many NBFC had done well when stuck to their niches … incl Edelweiss … But post 2015 , every one wanted to be Financial superstore … That is going beyond their stated strength . This often leads to huge learning losses which has still not been unveiled accordingly to me .

Now coming to points on

Competitive intensity will increase both from private and psu banks – As large players start becoming aggressive small payers need to rest otherwise they will get crushed . Why these guys did not focus on retail by reducing corporate books - they did which one see their retail book gr was as impressive as NBFC in many case … but management bandwidth is limited - You cannot run with hand fast if your feet are hurt … Now slowly these banks can focus on growth … with legacy issues getting sorted out .

While at this time NBFC has some legacy issues like loans to wrong developers etc to be sorted off . That will reduce their focus on growth

Supplier Power :

NBFC has been disadvantaged in money supply - but when stock price is going up - Your money raising option is more - and hence you can still access finance more easily then when it is going down . In QIP dilution will be higher , in portfolio sales margin will be lower etc … Conversion of virtuous cycle to vicious cycle in financial services very fast …

Just one bad cycle of 2008 destroyed competitive edge of ICICI bank over other banks , we have 100s of NBFC fail in 1995 - 1997 cycles .

I can go on on… But key for any NBFC is to survive next one year without any accidents . If they do - in next cycle they again can do well …

I think what people are missing out is the management capabilities AND willingness to drive competitive growth.

Rashish shah has lived through worse competitive disadvantages for decades and grew edelweiss to what it is. Similarly for few others. He was the first to spot ARC oppty and they have been quick to rework business models like agri commodity when required.

My point is that I simply don’t see that capabilities and more importantly desire to outshine in public sector at least. You just need to meet some of the GMs to know what I mean.

And as Charlie Munger said - incentives is #1 thing to fix in management!

Another factor we have to consider in this NBFC vs Banks debate is the interest rate cycle. When interest rates are cut it benefits the NBFCs more than the banks. Banks have access to CASA funds which are not sensitive to rate cuts and increases by RBI, you get 4% (or 6% in some cases) for savings and 0% for current account irrespective of the repo rate. For a NBFC a rate cut benefits most of its liabilities but a Bank depending on its CASA ratio gets maybe only 50% of the benefit. If the inflation is going to be benign and if the rate cuts continue NBFCs can still do well otherwise Banks will have the advantage

Banks and NBFCs is eternal debate and yet both have survived through cycles.

There are many differences in banks and NBFCs ( Even banks have nurtured NBFCs for their lending which is difficult in banks book, HDFC has HDB, Indusind bought bharat and has Leyland finance, Fed bank has fedbank financial services).

Strategically both Banks and NBFCs are important to economy and this is phenomena world over not only in India.

Still large part is credit deprived, SMEs credit needs are huge only banks wont be able to cater to the needs.

Banking system as a whole is stressed of capital, NBFCs largely are flushed with capital.

Liability cycle is structural issue and is going to hit the country ever 3/5 years, 2008. 2013, 2018 generally lasts for 3/6 months.

NBFCs are focussed while its difficult for a bank to focus (Considering too much to handle including treasury operations, cost of raising deposit, compliance cost etc.

Banks are pull model while NBFC is push model to customers. NBFCs are door step banking banks have not been able to cater to door step especially in rural areas.

Few NBFCs have focused niche and differential product offering - eg Bajaj (consumer finance) and Edel (largest player in Esop financing).

For Edel particularly it has developed great ecosystem of both credit and investment products. NBFC, ARC, Broking, IB, MF, Insurance and Wealth management.