Nothing changed in recent past but only sentiments. Why Edelweiss is hammering seriously? It has unique difference compare to simple NBFC - (1) ARC (2) Wealth Management (3) Life Insurance , etc. Excellent management proved by more 15 years of excellent growth and profitability. I thinks this is good opportunity if you believe India story where BFSI is crucial for projected GDP growth.

This bad time will consolidate sector and company with excellent underwriting and management will grow faster than past !!

Disc - started buying at this attractive level (waiting since long !!)

I think that this scenario will bring excellent entry points for NBFC sector.

My personal opinion is that nothing of this will matter if you look 5 years in future… Only thing matters is that good companies will continue to perform over long periods of time…

Everything is forgotten within 3 years…

e.g. Demonitisation, GST impact, Trump in White House, Brexit, Greece scenario, etc… which is long long list…

Disc: Invested and increased position.

Be cautious since the fall is extraordinary and it has fallen relentlessly. Mr Rashesh himself is saying that lending biz will be slow going forward and raising funds from banks is problematic. No doubt this is cheap on historical basis but one needs to keep his/her mind open. Liability side of the equation needs to resolved for the market to return the favour. Additionally, earnings in Q2 will differentiate men from the boys. Market will hammer down everyone and reward those who perform eventually. I would not be in hurry to increase my holding here.

Totally agree and that will give signals of good companies along with good entry points.

The Promoter holding has been on a steady decline for many quarters

This is not because the Promoter is selling stake but because of the steady dilution. This is normal for financial institutions but Edelweiss’s case is a bit different as a bulk of these are ESOPs.

What got my goat the last time I looked at this company was the ESOPs I mentioned here and here.

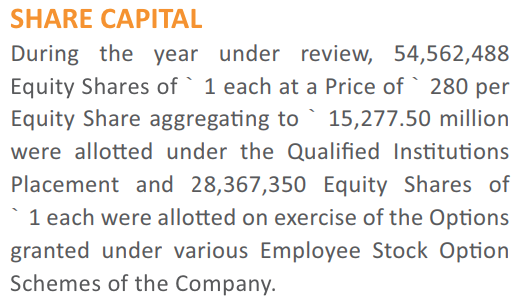

Looks like 2.8 Cr Equity shares were allotted in FY18 on exercise of options

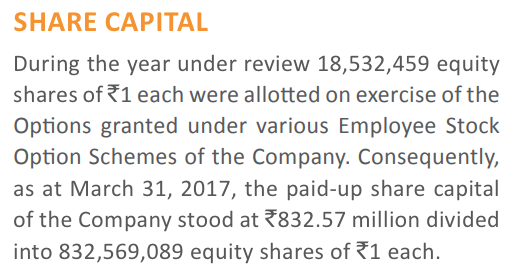

In FY17 it was 1.8 Cr.

This seems to have been much lesser in the earlier years

Looks like the company and employees made hay with a QIP (5.4 Cr shares at Rs.280 is 1527 Cr) and stake disposed/pledged going by the disclosures. I still believe these skew the P/L in terms of accurate reporting of Employee costs. At least that’s what kept me away primarily the last time.

They also have added employees very aggressively , currently their employees strength is 10K plus and are adding regularly and their target is to have around 12k by end of this year.

So may be it’s increasing with addition of new employee.

That’s purly a guess …have not checked or validated it basis data.

Good news…stability in growth, improving margins and improving asset quality

Check the below link  ️:slight_smile:️

️:slight_smile:️

There are 2 key issues (i will not call them concerns because I believe they can and given management expertise probably will be dealt with);

a) Rising cost of funds will definitely hit Edelweiss, I have heard from a reliable source that already their latest round of funding was 2% higher than the previous one and this was just before all this turmoil. Post this it would definitely be higher for the entire industry.

b) High exposure of business to capital markets, unlike a Bajaj finance Edelweiss’s excellent RoE is heavily dependent on capital market linked businesses, the AMC, wealth management etc. With capital markets being what they are and given they will possibly take time to recover, this end of the business may stay a bit depressed.

Some excellent analysis has been done by @Anant on the bond portfolio but tough to get a handle on how serious that situation is, if there is contagion investors are probably screwed but one can maybe give benefit of doubt to management given past record.

However it seems to me most of those concerns are more than captured in current valuation. I mean these prices we seem to think the industry is having some Lehmann moment. I mean IL&FS all said & done the problem is more of a cash flow mismatch and immediate term liabilities from what i understand are some 7000 odd cr in a total debt of 91000 cr. What is the probability of systemic contagion for an amount 7000 cr in a situation when you have shareholders like LIC!! (sarcasm intended).

We have come out of a bad loan problem many magnitudes higher and till yesterday all NBFC’s were darlings with excellent assets, stunning growth, 5-10 year story of taking away market share from PSU’s, riding the Indian consumer growth story, financialization story etc etc. Has any of this fundamentally changed, not really - only perception has…

Broadly while growth will slow, the real risk in Edelweiss IMHO is that while business will still do well but valuations may not in the short term. Just in the way post demonetisation Ujjivan and Equitas have not commanded the valuations they used to even though business has recovered because of the change in risk perception. So business may be impacted marginally but valuation may be impacted more substantially, but if one is willing to play a waiting game and add positions slowly (not catch the falling knife at one go), in 2-3 years this “crisis” may be a excellent entry point…

HDFC Bank has issued 24.84cr shares as part of ESO schemes in last 6 years bringing their stake down from 23.73% in 2010 to 20.93% in 2018. ESO schemes have been issuing decent chunk every year lately. Below is the screenshot for everyone’s reference:

Not trying to defend Edelweiss’ ESO practices. Just wanted to share the data so that we all have better look at how ESO schemes are being practiced at the best bank of the country (compared to Edelweiss) and interpret the data in a rational manner. I have seen similar practices at most NBFCs and private banks too.

@phreakv6 - would HDFC Bank’s ESO scheme practice (and ignoring all other factors) in last 6 years keep you away from it? You don’t have to answer if you don’t want to but I was just curious to know your comment here.

Thanks for bringing HDFC’s ESOS into the picture. I did not know this was an industry-wide practice. This does not make this any better in my mind though just because HDFC is doing it. I have a negative view towards financials in general as I explained in this post. I can understand ESOPs in start-ups but I did not expect to see these in mature businesses like these. I feel that a 1% dilution of market-cap if expensed in P/L under employee cost could skew valuations quite a bit. I don’t believe these incentives are required in the financial space which is already rife with enough bad incentives.

Financials have max weight age in Sensex and Nifty. Because they have created the max wealth till date in the country as a sector.

No other sector comes close to this level of wealth creation.

Guys simple question and correct me if my analysis is wrong:

Edelweiss raised money in troubled times at 11%, Bajaj Finance in the same time at 8.5% isn’t this separating men from boys.

In lending business this is huge GAP and all the more case to stick/move to Bajaj Finance

@ Raman - we would be comparing apples and oranges

We need to understand that the books are completely different. Bajaj Finance lends to Retail where market perceives lower risk and hence borrowing cost is much lower. Plus the parentage of Bajaj Finance is definitely a big advantage (you do get support from financiers if you are part of a big business house for example borrowing of Tata Housing and Godrej Housing is at least 25 to 50 bps lower than any other similar well managed standalone real estate companies)

Edelweiss has a corporate book (though it has now diversified the book to retail and is targeting a 50% retail book) and market rightly perceives that the risks are higher which is reflected in their borrowing costs (spreads of Edelweiss are lower but I am just comparing charges here)

Correct, for the same reason why not buy Bajaj finance than edelweiss as we are here to to make money than satisfy our EGOs isn’t it…Bajaj finance is leader of NBFC space and best stock available in this space…

Do you have any source to suggest Edelweiss raised @11%. I never saw this as confirmed news anywhere and I believe this is part of rumour mill. As far as I know Edel’s liquidity position is quite comfortable. Their balance sheet management unit is precisely for this reason. Bajaj’s consumer durable loans are for 6-8 months and hence there is no comparison.

If TCS is better than Infosys, does it mean Infosys is bad, or for that Matter any such comparison?

Edelweiss gets loan at 11% and Bajaj at 8.5% so we should buy bajaj, if that’s the logic it is totally flawed…

If it was so simple how could Edelweiss even exist, Bajaj Finance can capture all the Business of Edelweiss and why only Edeleweiss of all other NBFC’s in the market with that 2.5% or whatever Heads UP?

The two companies have different strategies and cater to different needs, this is not a Monopolistic market where a single player can capture all the market!

Yes if someone believes in highly concentrated Portfolio with only and only one stock per sector, he will need to evaluate what to do. But if someone takes a basket approach, he knows what is the right strategy.

I would love to buy Bajaj Finance (definitely a great business) but not at this market prices the price. Maybe at 1000 levels it’s worth a look.

Edelweiss is currently rated AA which would improve with time as they are diversifying its books with retail portion set to touch 50% of the book & with more cash on books (management after recent scare has indicated it would maintain 15% of the same from 10% currently) its rating would improve to AA+ / AAA and the cost of borrowing would automatically come down by 50 to 100 bps and help Edelweiss improve its ROE and ROA in medium term.

Further the free cash flow Edelweiss is currently making from it’s Non Credit Business is roughly Rs.400+ Cr. would allow it to grow its credit business with lower equity dilution.