Most of the quoted debentures are listed on BSE (ABT, Saha etc) but have never traded there. There is no quote, no 52 wk H/L. In such cases how would ECL price them?

From what I understand the following things should impact the pricing of bonds:

– The G-Sec yield : In FY18 G-Sec yield moved from 6.87 in the beginning of FY18 dropping to 6.43 reaching a high of 7.6 and closing at 7.19. Most of the banks had MTM losses in the last 2 qtrs on their treasury. How did ECL finances’ carrying value of its corporate bonds change? Also despite yield hardening ECL finance had a 300 cr excess of market value compared to its carrying value. I guess they must be doing a real smart job here.

–Rating of the company : Haven’t gone through all the companies but it suffices to say that a good number of them have moved down and some also to D. Since ECL in its AR does not give the market rate of individual companies it would make sense to ask them for the carrying value of each line item. It is very difficult to imagine how carrying value has remained above the market value with yields hardening and rating downgrades.

–ALM, Current Assets & Current Liabilities: If one looks at the balance sheet in term of non-current liabilities vs long term assets and short term liabilities and short term assets it looks decent. It does not show much ALM concerns in short term (a year). The problem is when you look at the 7500 cr corporate debt Stock in Trade (which is in current assets) which is not maturing and the company can have difficulty selling off and is financed by short term borrowings one can see a problem building up.

–What happened in Q1 FY19: In Q1FY19 yields went up from 7.19 to 7.9 a 70 bps jump. Ideally there should be an MTM loss on the entire Stock in Trade portfolio unless some part was sold of. Going by last year’s rate it should be around 14% a quarter.

Finally in financials I understand trust is key since a lot of jugglery is possible in books, but I think these are pertinent questions and it would help if someone has asked/understood this aspect.

So, ECL fin is almost half of Edelweiss profits. And stock in trade is 36% of ECL fin assets. So, 18% of Edelweiss assets are these stock in trade.

Out of this 80% is in corporate debt.

So, 15% of Edelweiss assets are in corporate debt.

Let us assume, 15% of this debt defaults completely and goes to zero.

That gives us a 2% net impact.

Edelweiss fell 10-15% yesterday in one go. #JustSaying

I think you need to work out a little more math (& finance here), if the entire corporate book defaults Edelweiss net worth will be completely eroded. If 15% defaults as you are saying 2.25% of net worth gets lost but also the underlying ability to borrow and it will have to sell more assets to manage debt equity since it is levered around 6/8 times.

I am sure the entire corporate book will not default and assuming the underwriting is good most of it will not be impacted in the long term, the issue is more of short term liquidity and the mark to market adjustments which I guess has not happened.

Fin cos are leveraged cos. And the entire debt defaulting is ZeroHedge prediction for 10 years now for big countries like China.

Even ILFS debt is backed by huge assets and is more of a cash flow mis-match and not the company going bankrupt. It is govt cos that owe huge payments to Ilfs.

Usually MTM accounting is done if the bonds are held in AFS (available for sale) category. If however, it is held in HTM (held to maturity), then MTM accounting need not be applied.

Not sure about edelwiess split, but the categorization is done at the time of investing in the debt and there are rules around moving them between categories. HTM to AFS is allowed, but vice versa is not usually.

For ALM - look at slide 44 of the investor presentation , they have a fairly matched book and often this done via derivative instruments too. finally slide 47 also shows a 5500 crs liquidity cushion which is close to 9% of the balance sheet.

Long term viability of ECL Finance corporate debt: I am not suggesting any defaults here. I am just saying that I dont understand the quality of these but at the same time from the face of it most of the corporate debt looks low quality. At the same time I would assume there is significant underlying asset which can help recover incase of a default. The point of my most is not to any way suggest the long term outcome of this debt.

The points that I am trying to riase are:

The points I have raised are related to Short Term Assets and specifically Stock-In-Trade which is not maturing in short term. If these were HTM assets going by their maturity they should be held in Long term assets. IMO these should have MTM accounting.

Why is all the “super detailed digging for pitfalls” and “hunting for negatives” happening only when there is price erosion? This thread has been around for a long time and nothing exceptional has happened in the past few weeks/months except the 25% price correction, but it seems all the negativity are coming out only after the price fall.

It would have been great if these negatives were listed when the price was at 310 levels then the people who were not comfortable with the fundamentals would have got a decent exit.

Unfortunately when the price was going up, only things being posted were the praises for Rashesh Shah and how great the company is fundamentally.

I am not justifying what edelweiss is or is not doing. I am describing the account standard.

AFS and HTM classification of assets (Bonds, NCD are just a few example) is done at the time the asset is put on the books. It is based on the intent of the management and have to declared. The same asset can land in either buckets, but management has to make the decision at the time the asset is put on balance sheet. If an AFS asset has a change in value, the changes is passed through P&L. For HTM asset its a little more complicated where changes may be captured in OCI in some cases.

Management cannot change an asset from AFS to HTM on the fly if they suddenly start seeing losses in the portfolio. Banks were given special permission by RBI in the past to do this, to avoid them from showing losses.

The balance sheet classification which you mention is the duration of the asset. Both AFS and HTM assets can be short or long term based on the duration of the asset (or even the intent of the management).

On liquidity - it is usually defined as cash or equivalents/lines of credit. Atleast thats how it is defined. The same slide talks of liquidity as banking lines, FD and G-sec. I dont think they are considering corporate bonds

If we look at what was held in Stock In Trade in FY17 almost 56% of it was sold 46% was carried over. Would it not be fair to assume that Stock In Trade is AFS.

The company acquired debentures in the same company at significantly higher coupon (300 bps). On the face of it this looks like evergreening but may be management can have some explanation.

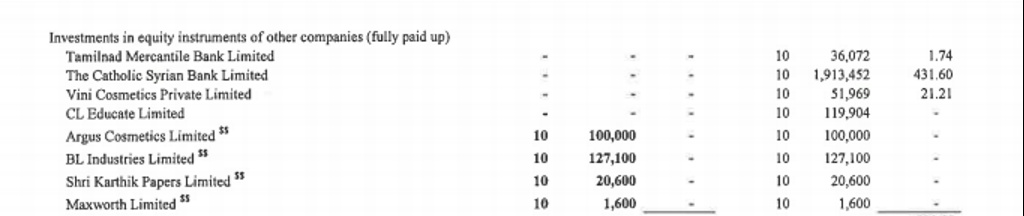

Another thing relative small but where MTM should have happened Edelweiss investment in Catholic Syrian Bank (CSB). Edelweiss bought 4% of CSB around 19 lac shares around 2010. This investment has been carried on the books of different subsidiaries of Edelweiss at Rs 225 a piece. In my opinion there is a case for significant diminution in value. CSB made a rights issue in 2015 at Rs 75. It was followed by dilution at Rs 120 and the book value at the end of FY18 was 105, now most recently a stake sale has happened at Rs 140 to Fairfax,

CSB investment was present in the books of Edelweiss Finance and investment last year not sure where it has been moved to this year.

@Anant, Gonibedu coffee estate is part of Cafe Coffee Day I think. I saw their name in the prospectus. So not much risk there.

Not sure about CSB, but figure looks small. Although I do have 1 question - Why did Edelweiss not subscribe to rights issue at 75? That would be a very silly thing to do on their part after investing at 225. Do you think we may be missing something? The above snapshot that you presented, is it for the last year? Because number of shares are still 19 lakhs, ideally they should have been more after rights issue. Also, I could not find Edelweiss name in the list of top 10 holder of CSB, ideally it should be there. Is it possible they have sold their stake?

Thanks for clarifying on Gonibedu as I said there could be possible business reasons but the point is to explore them.

On CSB: Around 2010 there were many institutions interested in acquiring CSB so that they can get a universal banking license and Edelweiss too was interested due to the same. Why Edelweiss did not participate in Rights isssue could be that they no longer had the strategic objective of becoming a bank.

Both the CSB rights issue and Gonibedu loan could have a valid business explanation. The concern is more in terms diminution in value of financial assets which probably has not been addressed properly.

With dilution done last year Edelweiss no longer remains in the top 10 shareholders.

Anant - my comment on your point that you raised above regarding MTM adjustments in the bond values:

As we know, if there was any MTM loss taken because of decrease in value of corporate bond, it would have passed through P&L decreasing bottom-line (gain in bond value also passing through P&L increasing bottom-line).

I looked at last 5 years financial statements of ECL Fin and Edelweiss Consolidated to check if/how MTM in current assets impacted the numbers. Below is what I found:

I would take Consolidated numbers with big pinch of salt as we know there are tons of moving pieces in the consolidated numbers. If MTM loss come under “Other Expenses - Diminution in value of investments”, then ECL Finance has not taken any big MTM hit. In fact, for FY18 there has been reversal of 12.8cr for ECL Fin.

I would request someone else to reconfirm my findings. Also, please correct me if MTM losses don’t come under “Other Expenses - Diminution in value of investments”.

Without going into the technicalities of valuing a bond - I noticed most of these bonds had coupon greater than 12% and some were as high as 20% with duration of 2-4 years left for maturity. I don’t know what their current Yield to Maturity is. To keep things simple - if 10 year GSec yield is 8% (it would be much lower for smaller durations) - and if most bonds coupon is north of 12%, Gsec yield moving from 8% to 9% would not impact as much to price of shorter duration bonds with very high coupon rate. It would impact more to longer duration bonds with their YTM/coupon closer to 8-9%. A bond downgrade or late/default coupon payment would be a bigger drag on price than 100-200 basis points yield movement for such short duration high yield bonds.

Re: Long term viability of ECL Finance corporate debt and ALM and liquidity issues: If above findings confirm that major MTM losses were not taken in the past, then it shows that BMU team is capable of managing liquidity and ALM.

Please note that I am not giving Edelweiss BMU team a 5 star award for best treasury management based on above findings. Just wanted to share my findings with you and other participants.

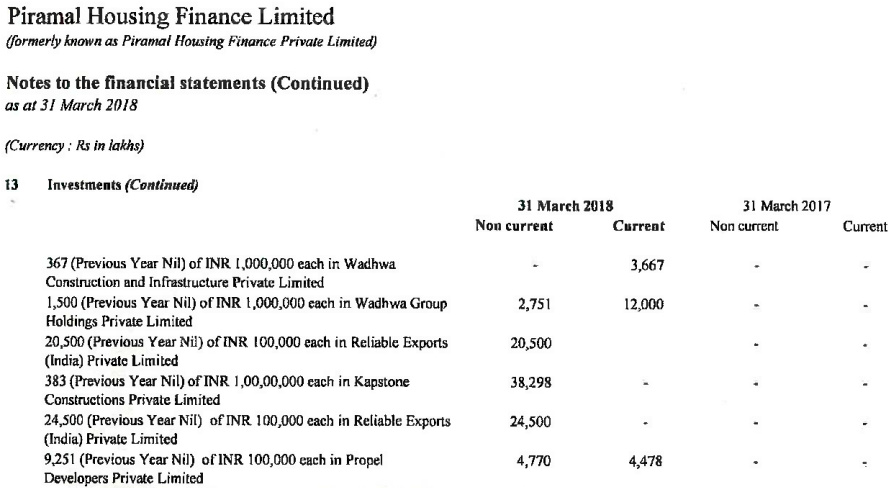

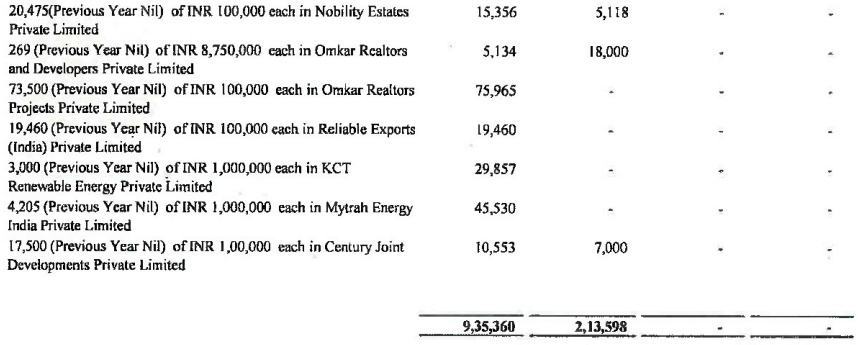

On a separate note - I found that PEL (housing finance subsidiary) has about 2136cr (current) and 9354cr (non-current) investments in unquoted debentures to many private small players which makes up approx 25% of their assets. Below is a screenshot. These definitely don’t seem like super liquid investments. IMHO - it’s part of business to invest in such instruments and having a top-notch management to maintain ALM and liquidity is the differentiation between quality and ordinary lending business. For me management is super critical in lending business.

Disc: I hold PEL and intend to hold both PEL and Edelweiss forever unless there is structural change in lending business or any corporate governance issues are uncovered. Hence my views may be biased.

I agree with you on this that for shorter duration bond the impact is not significant since there is no compounding of interest and also I agree with you on that higher the coupon lower the impact. Very simplistically the loss for Rs 100 bond for a 10% coupon and 1 year in maturity and with annual payment is 100 * (1.1/1.11) = 99.09 and the same bond with 20% coupon 100*(1.2/1.21) = 99.17 when yields go up by 1%. But as maturity goes up the losses increase, so the same bond with 2 year maturity would now be at 100*(1.1/1.11)^2 and so on. Rough loss are in multiples of .9Years to maturity.for 10% coupon and .8Years of maturity for 20% coupon. So on a 7000 cr portfolio held for ‘Stock in Trade’ and an average maturity profile of 2 years the MTM losses would be roughly 140 cr (I am not considering the rating downgrades) for a 1% yield going up.

Piramal Housing: A cursory look at Piramal Housing makes me think that they have done it the right way and feels good to look at it after looking at ECL. The key difference being that there is no ‘Stock in Trade’ portfolio. The current and non-current Corporate bond investments are in all likely on account of their maturity in the coming year or years after that respectively. Most (or all) of their portfolio looks HTM. Also the Current investments:Non-current investments ratio is 4:1. The only thing which I did not understand is that all the investment origination is new (probably moving from one subsidiary to another).

funding through structured bonds is one way of corporate lending book. Its part of structured financing including promoter funding. These structures are being done by large corporate funding books like Piramal, ECL, ABFL, Kotak (through various entities), avendus, Indostar. These are part of collateral based lending. After this quarters INDas adoption, NBFCs will have to be transparent in disclosing their credit losses, its now akin to Insurance reserving, it will be based on expected credit loss and life time loss has to be taken in to consideration along with data of portfolio performance of past few years. These deals prima facie looks risky, however it totally depends on structuring and underwriting of these structures. Many Wealth management entities does this for their wealth clients. We need to trust management for these structuring and underwriting.

For Edelweiss there the headwind is interest rates however it doesnt seem to be a long risk. However there are many tailwinds. The SEBI cap will give level playing field for smaller Asset Management companies, also large part of their Asset management is AIF ( not MF). AIF is still at nascent stage in India.

Wealth management has just started off the tipping point.

Insurance also will eventually have level playing field considering regulations. NBFC and ARC is doing well and eventually am hearing they have banking aspiration.