Per correspondence with co over email after Q2 nos, they have attributed margin expansion to some additional factor other than local sourcing which is key as well. These were - Price increase in some products , higher share of higher margin products in mix. Though they were non committal on sustainability but have done one noth better in Q3. My sense is that market is in disbelief and would.like to wait n watch, though it clearly appears as structural up move in margin profile.

Key part that stood out in their comments was parent support as making india strategic element in APAC( currently india serves SAARC as well)

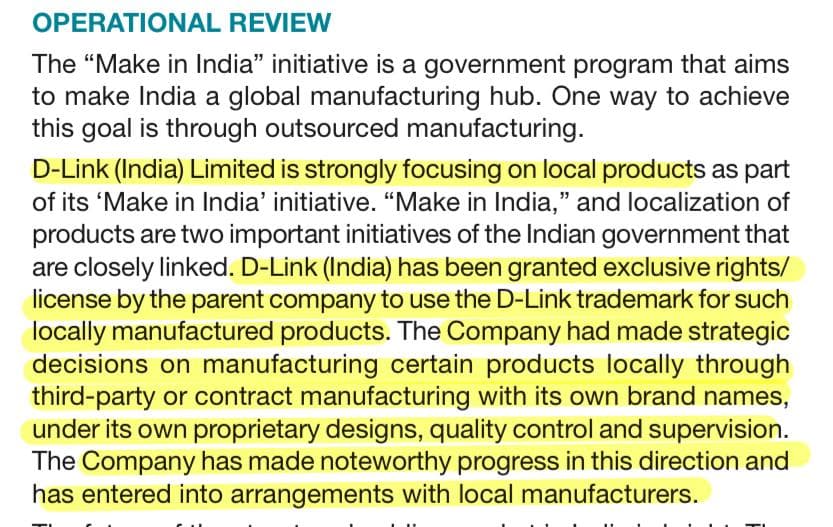

Parant has given full freedom on sourcing while commitment of R&D support is given as well. One can check RPT and royalty works out fair with these kind of support.

While Dlink directly hasnt applied PLI, their local subcontractors have it and thus both parties stand to gain which is also a structural underlying boost to margins.

Dlink india stands to gain with Taiwan china escalations as well and may serve as global supplier at some point - they didnt agree nor denied it.

All in all asset light debt free MNC play with more totally undemanding valuations.

QoQ while bottomline is improving substantially, topline hasn’t moved much - this stays key to watch out for. Suspect some seasonality here.

There is a dip in profit qoq, EPS has come down from 7.7 to 5.7, inspite of 10% increase in topline. Reason to be ascertained.

You, topline has gone up from 918 cr to 1180 cr, i.e. 30% increase! You EPS has doubled from 11.7 to 24.3. Company has declared Rs 10 dividend.

A company in technology domain, with MNC pedigree, increasing localisation, given a freehand by mother company, increasing export potential, enjoying customer’s trust. Has the potential to scale new high.

I wish there was a press release every quarter on performance and outlook.

Disclosures are very poor. However company has delivered good PAT growth and is super cheap with high RoE 26% and RoCE 35% and MNC parentage.

I don’t know if people have noticed the Rs10/share dividend announced which is a 42% dividend payout ratio. After the 9% surprising fall stock trades at 10.6x FY23 P/E with 4% dividend yield.

My sense on DLINK is that they benefitted disproportionately due to the Covid-related closures in China. Dlink makes routers, switches etc which are rather low-margin commodity sort of products.

The margin shrinkage this quarter indicates I could be right. Need to observe for a few more quarters to be sure.

Disclosure: No investment, only academic interest.

margin expansion being sustainable was’t confirmed by mgmt during my correspondence with company in previous qtr (indicated depends on product mix), however price action aligns to @basumallick views.

Cat 6 structured cable category seems to be doing well for them and could be a factor in product mix that played out over last few qtrs as institutional order - feelers from AR and some of railway tenders quoting Dlink as ref product.

Due to lack of mgmt communication (both pro active and lack of clarity in queries response) its difficult to assess company aspirations even though sector offers potential.

Have exited post Q4 results, stays on radar for agm communication etc.

Based on some further research, I understand that margins in Q4 were impacted by higher raw material (copper) prices, which have come down in April and May…

Came across an article which states Dlink has launched an indigenous series of surveillance solutions. These products are designed and manufactured in India

Nothing performance in Q2, as the management says nothing, don’t know what to make of it. Meanwhile Foxconn, the other Taiwanese company in electronics manufacturing continues to make waves.