Dear Mr pankajs,

Reviewed the Annual Report FY16. Net profit of Rs.33.19 crores vis-a-vis 16.39 crores of net cash from operating activities. This works out to around 50% . Is there thumb rule on margin between CFO and net profit ?

Regards

Dear Mr pankajs,

Reviewed the Annual Report FY16. Net profit of Rs.33.19 crores vis-a-vis 16.39 crores of net cash from operating activities. This works out to around 50% . Is there thumb rule on margin between CFO and net profit ?

Regards

Few pointers…

De-growth : People moving to mobile intrenet and not router internet

Margin pressure : Commercial and Govt consumers are price sensitive

But…

Opportunity : Roll out of public WiFi systems

There was a time when I used to buy the latest and greatest router and keep upgrading every couple of years or so and stuck mostly to D-Link. They had a brand which was recognisable in a sea of chinese devices. But now broadband companies like Airtel get their own router installed free of charge to the Customer and these are some cheap OEM chinese brand and so the Customer almost never has the need to go and buy a router for himself. I think this has pretty much killed sales growth for companies like D-Link.

ICICI report on latest results - http://static-news.moneycontrol.com/static-mcnews/2017/05/IDirect_DLink_CoUpdate_May17.pdf

True. So, it seems the only market available for D-Link is public WiFI systems. Not sure when this will roll out.

Heartening to see the encouraging ICICI report on DLink. Thanks!

HDFC research has also issued a report recently with a buy rating on D-Link. I don’t have the report handy but it is available in their pick of the week section which has a very high rate of success.

That’s an encouraging news as I have taken a small position . What are all the main convictions in the report for the buy call. I also heard that D-link would get re rated in view of the TEJAS’s IPO listing.

Thanks for sharing the report. Shall review and revert.

Any views on D-link at current levels from a medium term perspective?

One additional question i have is D-link vis-a-vis Sterlite Technologies. What are your thoughts? Which one will be a better beneficiary of the digital initiatives from GOI?

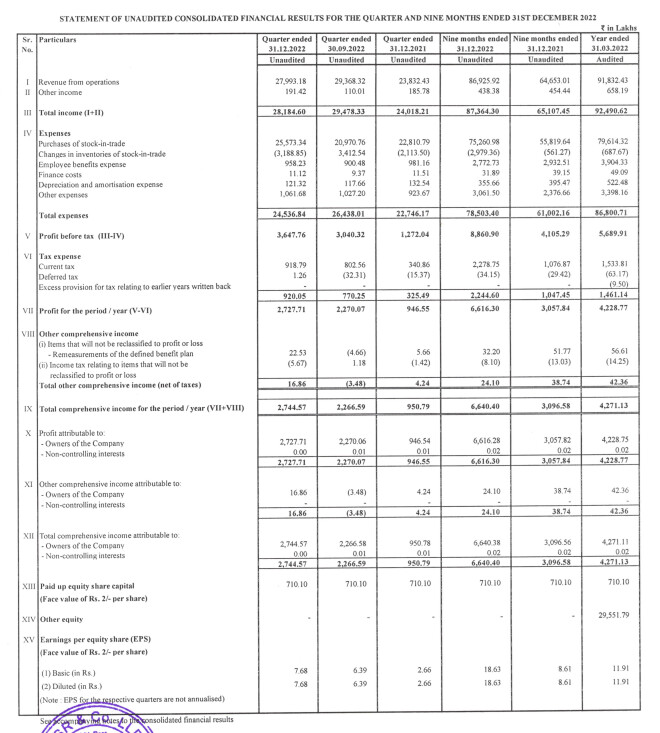

Q2FY23 Net Profit Of 23 cr

VS

Q1FY23 Net Profit Of 16 cr

VS

Q2FY22 Net Profit Of 13 cr

QOQ Net Profit Growth Of 44%

YOY Net Profit Growth Of 77%

Share Holding Pattern

#DLINK cmp 205 Mr ASHISH KACHOLIA

Enters 1st time Directly with

3.34 % Equity

Previously never held

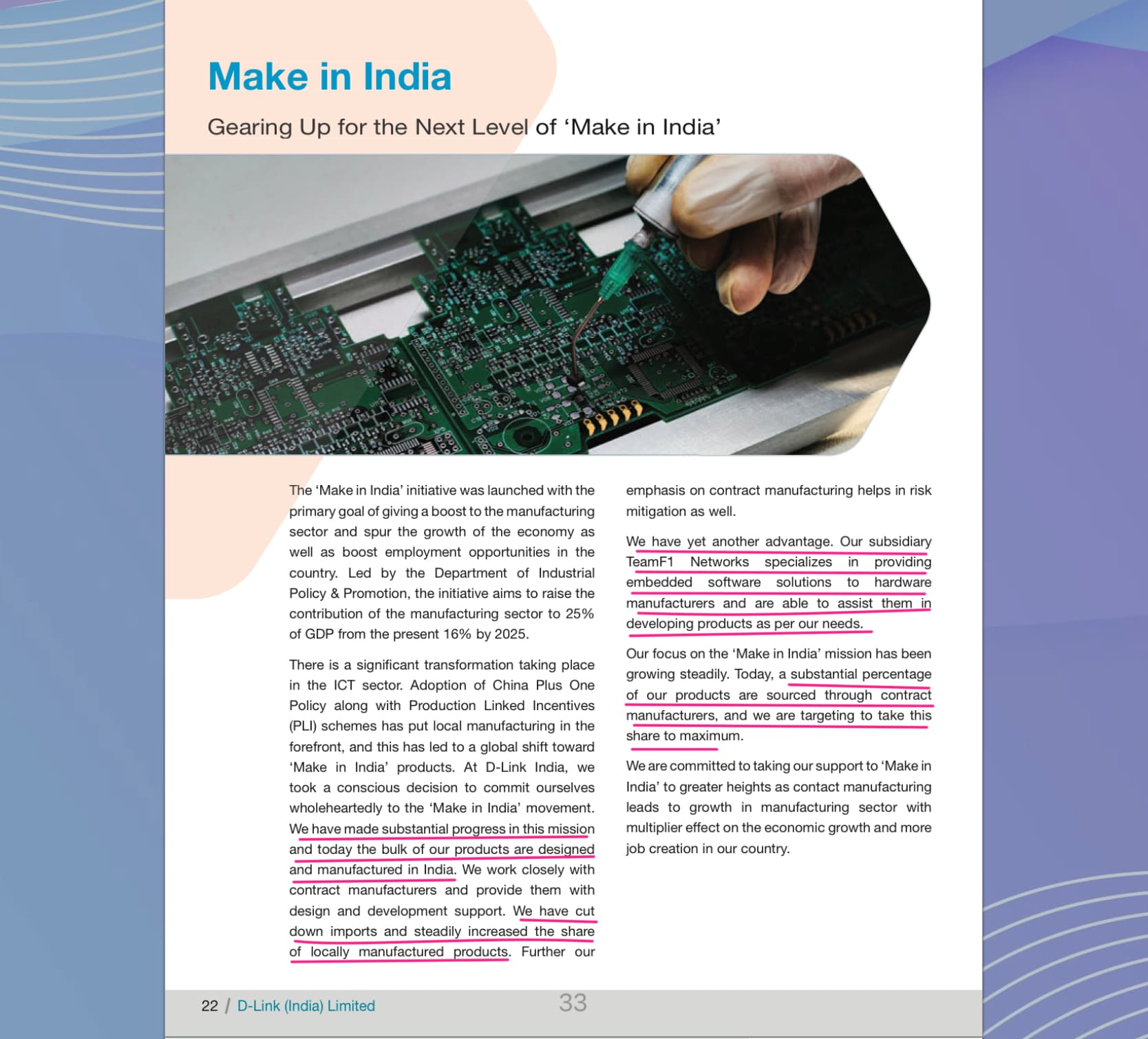

I could not find any concalls or management interviews. I guess so far they have been just importing the end product and selling in India. But recently they are contract manufacturing and selling. thereby they are able to increase their profit margin. But just want to confirm how much is it true and what is the future of this. Are they going to substitute all their imports with local manufacturing then its a big positive for the company. Is this one of phenomena or the trend is in bold.

Look super interesting. In 1HFY23 company has grown PAT to Rs38crs +90% YoY. If they can maintain the same in 2HFY23 they should do PAT of Rs76crs. So at Rs956crs company is trading at a P/E of 12.6x for company with 15% plus RoE and net cash balance sheet business paying decent dividends and growing.

The shift of manufacturing to India is a very big deal. India produced produced products are cheaper than China or Taiwan now. So I wonder if D Link can be used to supply to other countries also in the future using the contract manufacturing in India.

You are already seeing the rise of EMS (electronic manufacturing service) in India with the likes of Syrma SGS who is talking of 40% industry growth. D-Link is of course not an EMS firm but might be sourcing from EMS firms

Disclosure: Invested

Superb results by D-Link. Rs18.63 EPS in 9MFY23. Should do atleast Rs26 EPS in FY23E. Stock trading at 8.0x P/E FY23

Any reason for dlink margin improvements? Are they manufactoring in india?

They are not manufacturing in India, but now they are getting manufactured in India ( since last almost a year )vs only imports. The margins improvements might be because of this amongst other reasons.

D-Link appears to be an exciting opportunity with Q3 numbers, that were indeed top notch, with continued margin expansion at the operating level, now at an impressive 13%. It was about 10% in Q2, which itself was a big improvement from its long term average of about 7%. I gather from reliable sources that this is largely due to more local purchases from their Indian vendors & lessor imports from Taiwan as also mentioned by @Gandhi_Jayesh in the above post.

I also gather that the Co. has improved its efficiencies by opening ware houses at multiple locations across the country. Earlier it was centralized at one place. It has also been developing multiple vendors across the country for its supplies. This has resulted in improved profitability with lower transportation costs, far lessor turn around time & quicker deliveries. This further helps in inventory mgt. at the distributor level.

I understand that improvement in operating margins on higher sales are sustainable, n perhaps the new normal. We will have to wait n see if this is indeed the case because if it is, then the stock is ripe for re-rating from its current low multiple. D-Link is a debt free Co. with a high RoCE in the proximity of about 37% for the current year 22-23.

The current market cap is only about 855 crs.