The HAM business is capital-intensive and by experience company knows it that’s the reason they are moving slowly away from these. Company is good at written procedures and quality manuals and has stringent quality procedures which is very encouraging.

If you are taking loan @10% and able to invest in some activity where the return is more than the cost of interest e.g 12 or may be 15% than you are adding capacity at no cost it is PURE DHANDO ……The company’s Borrowing committee is headed by Dilip Suryawanshi who was proprietor the firm before it become publically traded company and I hope he knows the power of leverage . Company has strong execution Skills , That the reason L&T finance had backed giving unconditional and irrevocable counter guarantee (CG) to the Yes Bank .( The company received an early completion bonus of INR877.9 million in FY18 (FY17: INR514 million) and is entitled to a further INR290 million bonus in FY19, which is a testimony to its strong execution skills.)

However the data in screener it shows so you have valid reason but my humble suggestion is that one must to go through the AR and one may be surprised to experience that one’s learning curve may be grow to the max

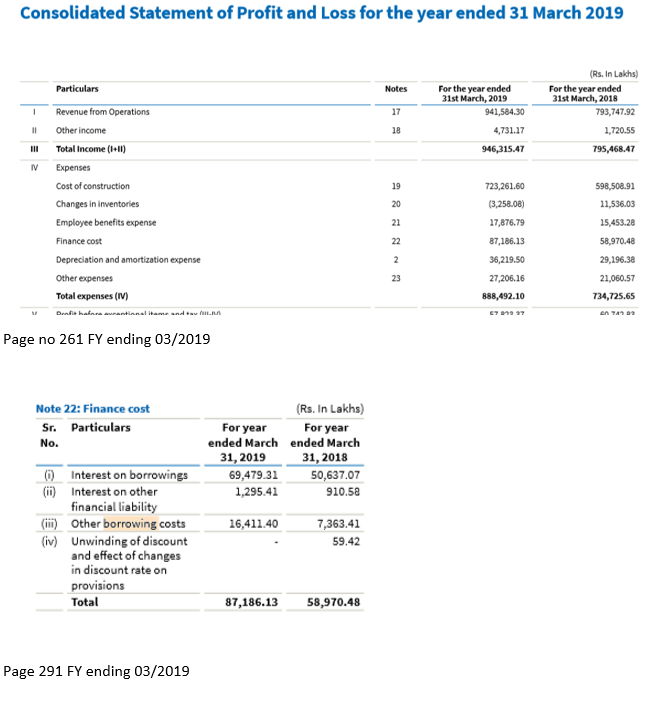

Now to take on borrowing costs. As per the AR it says that ," Borrowing costs are interest and other costs (including exchange differences relating to foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs) incurred in connection with the borrowing of funds. Borrowing costs directly attributable to acquisition or construction of an asset which necessarily take a substantial period of time to get ready for their intended use are capitalised as part of the cost of that asset. Other borrowing costs are recognised as an expense in the period in which they are incurred."

This is excellent news after the recent gloomy outlook in infrastructure due to the recent letter of PMO to NHAI.

Out of the investment of 290 crores which Dilip buildcon has already made they are getting 409 crores which translates to around 37.5% returns.

Also this signals the foreign investors are showing interest in the Indian Infrastructure space and hope there is no govt interference in these kind of deals.

Sorry for my limited knowledge. But can anyone explain how selling of HAM project will help DBL in long run? I was hearing Rohan Suryavanshi interview and he mentioned that DBL will sell rest of 7 HAM projects in next 3-4 months.

DBL business model is t to monetize the assets as soon as its completed and they don’t want to maintain the roads and get revenue from them in the long run.Their strength is quick execution and their strategy is to get good returns on the money they have invested in these projects.It will help them to improve balance sheet,working capital to enable them bid for the upcoming projects.

Their preference is only EPC projects but since most projects given by the government are in HAM model,they execute HAM projects for their EPC part.

Now their challenge is to get the buyers for their completed projects and so far they are able to get them.Shrem group bought some of their projects earlier and now Singapore based Cube highways have bought four of them.

This is to inform you that,the best quartly result came out.

1,Net sales has increased from 2564.39 cr to 2746.19 yoy.

2, Most notable one is Profit after tax has doubled from 87.69 cr to 181.91 cr.

3,FII also has increased holdings

4,No management pledge

5,Get lot of project’s for approval

I think get ready for another spectacular ride in Dilip buildcon…Share your views guys…

I think their best quarter is yet to come. Typically Q4 is better than Q3 and Q3 is better than Q1 and Q2 due to monsoon in Q2. Also trend is thta Govt allocates many infra projects to these companies in March before financial year ends. DBL order book has already been around 31000 cr and it might grow more within Q4. So I think next 2-3 years belongs to infra sector and companies like DBL are going to benefit.