One need to go through the following reports to have better understanding of the company debt

http://www.careratings.com/upload/CompanyFiles/PR/Dilip%20Buildcon%20Limited-05-03-2019.pdf

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Dilip_Buildcon_Limited_April_10_2019_RR.html

https://www.indiaratings.co.in/PressRelease?pressReleaseID=36761&title=india-ratings-revises-dilip-buildcon’s-outlook-to-negative%3B-affirms-‘ind-a%2B’-

The HAM business is capital-intensive and by experience company knows it that’s the reason they are moving slowly away from these. Company is good at written procedures and quality manuals and has stringent quality procedures which is very encouraging.

If you are taking loan @10% and able to invest in some activity where the return is more than the cost of interest e.g 12 or may be 15% than you are adding capacity at no cost it is PURE DHANDO ……The company’s Borrowing committee is headed by Dilip Suryawanshi who was proprietor the firm before it become publically traded company and I hope he knows the power of leverage . Company has strong execution Skills , That the reason L&T finance had backed giving unconditional and irrevocable counter guarantee (CG) to the Yes Bank .( The company received an early completion bonus of INR877.9 million in FY18 (FY17: INR514 million) and is entitled to a further INR290 million bonus in FY19, which is a testimony to its strong execution skills.)

However the data in screener it shows so you have valid reason but my humble suggestion is that one must to go through the AR and one may be surprised to experience that one’s learning curve may be grow to the max

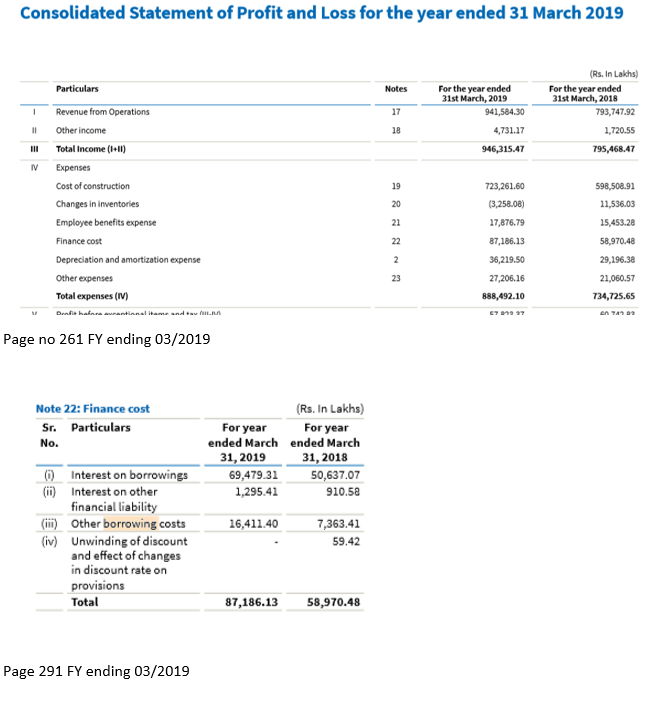

Now to take on borrowing costs. As per the AR it says that ," Borrowing costs are interest and other costs (including exchange differences relating to foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs) incurred in connection with the borrowing of funds. Borrowing costs directly attributable to acquisition or construction of an asset which necessarily take a substantial period of time to get ready for their intended use are capitalised as part of the cost of that asset. Other borrowing costs are recognised as an expense in the period in which they are incurred."