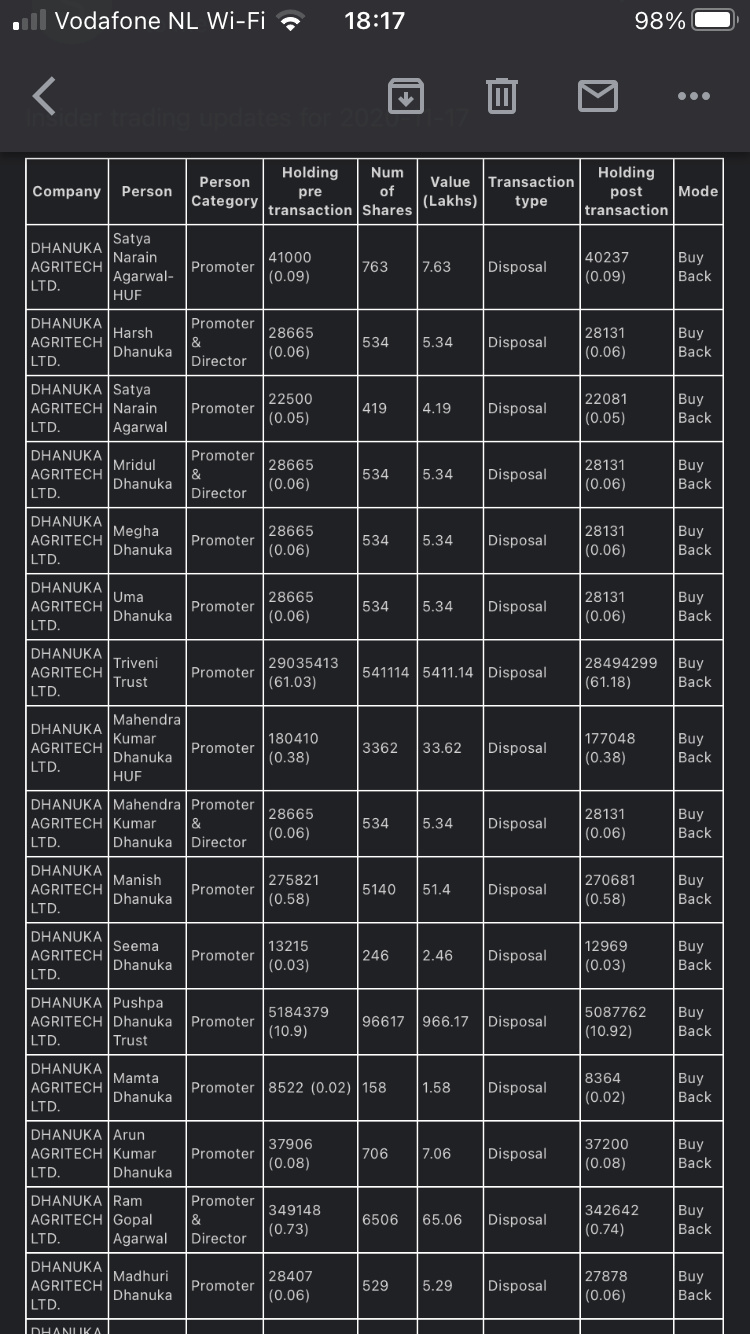

Buyback coming up. It would be interesting to see the buyback price after such a sharp run lately.

1 Like

Dhanuka has come out with a great set of results.This was buoyed by a spillover of 20-25cr. from Q4 to Q1 and some preponement of buying from Q2 to Q1.The concall was also good.Some highlights:

-> Good harvest,great monsoon and ability to leverage a strong balance sheet helped Dhanuka capitalize on high demand.Volume growth was 72%,realisations were down a bit yoy.Expect volume and value growth to converge as the year goes on.

-> As indicated earlier,lack of labour led to very strong sales for the herbicide segment.But this dragged down the GMs,since the product mix was heavily skewed towards herbicides.However,gross margins will improve as the year proceeds.On a yoy basis,GMs will certainly be higher.

-> Concerted action from authorities against spurious products and questionable manufacturing practises continues.Dhanuka and the organised sector will benefit from this.

-> Out of the 27 molecules that were slated for a ban,only 3 are “red triangle” products.Thus,these will be the ones to get the axe first.Company doesn’t see this happening swiftly.Also,locust attacks don’t benefit Dhanuka directly.However,such occurences increase the demand for agrochemicals and thus,DAL might have benefited in an ancillary manner.Hard to put a number on this.

-> On/off lockdown in certain states and regions continues to put very short-term pressure on supply chains.But broadly things have normalized.On the RM side too,there is no pricing hiccup.

-> Sticking to the 20%+ revenue growth and 100 bps margin expansion guidance.Last fy,Rabi season was great and thus base is high.This could put pressure on growth numbers in H2 this year.

-> With buyback,the tax liability is on the company’s side while for dividends it would be on the shareholder’s side.Thus,took the decision for a tender buyback.For fy21,there will still be some dividend though much lower than last fy.

-> Company believes that the unorganized players are having a lot of trouble.They were unable to supply in the numbers they otherwise would have in such a strong environment.Dhanuka benefited immensely from this.

-> Plan to launch 2 new 9(3) molecules in FY21.

-> Given the high dependence on monsoon,the organised players(including Dhanuka) are shifting towards ‘drought resistant’ products.One of the company’s recent launches is for water starved rice fields.

-> Company has very little dependence on China.All partners are either Japanese,European or of American origin.On the RM side too,dependence is not much.

-> DAL wishes to be present at all access points of the farmer.The move to get deeper in a market is taken on the basis of primary sales.For regions/areas where the primary sales are strong the company then pushes for secondary sales.

Overall,management seemed cautiously optimistic about coming quarters.This is all I can recall.

Disc.: Invested.Views are biased.

10 Likes

Is the Buy back record date announced.?

1 Like

Govt Atmanirbhar push on Agrochemical - GST cut , corporate tax cut and many more !

1 Like

Price has been falling every day. Any particular reason?

1 Like

Dhanuka Agritech launches two fungicides for Grapes namely kirari and Nissodium. Kirari is a researched product from Nissan chemical Japan and Nissodium from Nissa chemical - Europe.

There is a very good interview of Dhanuka Agritech Promoter recently he gave to Nirmal Bang. It was a wealth of information as well as how long it takes to get approval from the Babus. He was suggesting about the huge opportunity that exists in Horticulture.

Regards

1 Like

Can you please share the video interview…

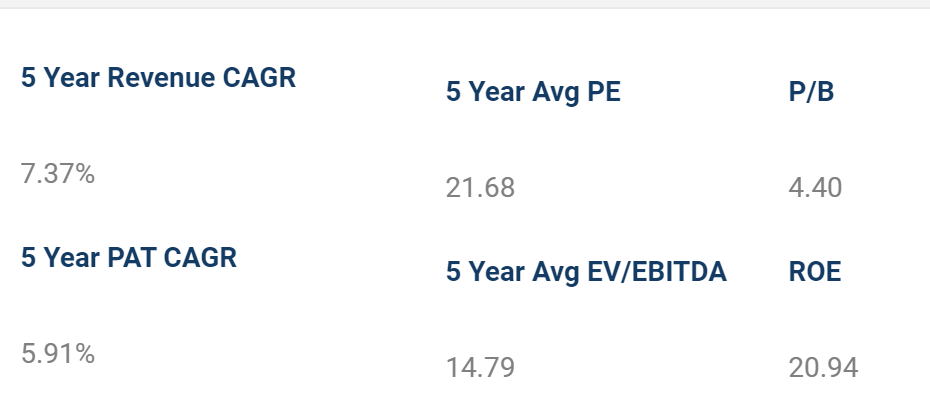

Maybe the stock is now fully capturing the fundamentals. I just checked the valuations. Current valuations are around 5year average of 21PE but profit growth is only around 6% cagr over last 5years. To me it appears that stock given it’s highly consolidated shareholding is trading ahead of it’s fundamentals.

Sharing the link. He has information at his fingertips.

2 Likes

Market is always forward looking …not backward looking. You may come across many stocks which have been giving negative returns in the past , but now the market is Re-rating those stocks and giving a high P/E due to change in fundamentals of the company or the Sector in which the Company operates and the market expects a good performance in future.

(1) Here the company under discussion operates in Agri sector which is receiving Agri-Push from the Govt like never before… This year all the Actions /reforms are directed to improve Rural Economy, Agriculture, Agri-inputs by way of priority lending, Subsidy, Direct benefit scheme to farmers …etc.

(2) This has resulted in superb performance in Q1 2021 with 250% increase in Net profit and 70% increase in Revenue. During lockdown, the Agri- inputs were treated as essential and so the plant operated full capacity to meet the market demands. The management has given guidance higher double digit growth in 2021.

(3) The ROCE at 26% is the highest in the industry

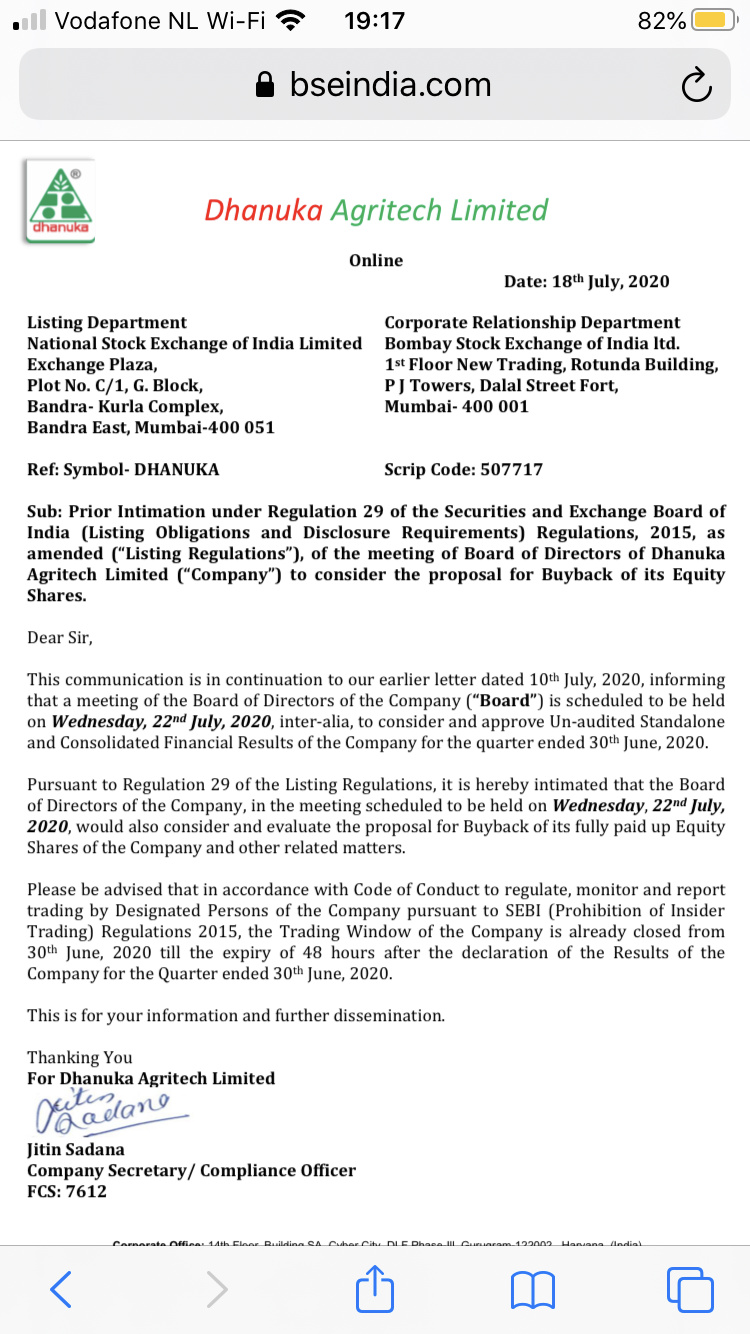

(4) The company has declared a share Buy Back @Rs1000 to reward the share holders apart from regular Dividend. In fact it has been a regular Dividend paying company. Two years back also, it

had rewarded the share holders with a Buy Back.

(5) It has never diluted its share holding by selling stake or pledging shares. It still holds 75% stake indicates promoter confidence in the company it owns.

(6) The stock has fallen recently from Rs 900 perhaps due to Indo- China border tension in line with all other Agri stocks since there may be some import content for raw material…However , the situation remains same for all Agro chemical stocks / pharma API stocks where most of our companies depend upon Chinese imports for raw mateterial…

Discl: Invested. Forms a small portion of my portfolio though. May be biased and I may be wrong in my assessment. Please do your own assessment before investment.

.

3 Likes

India Agri Exports during Q1 2021 rises by by 23 per cent to ₹25,553 crore as against the export earning of ₹20,735 crore in the corresponding period in the last financial year.

How Modi Government Has Speeded Up Its Efforts To Increase Agricultural Exports, Double Farmers’ Income

1 Like

Hi fully agree with your thesis on being forward looking. Also agree to the company looking good on most parameters.

However will be a bit cautious extrapolating the Q1 performance. This year the monsoon arrived early and so lot of Q2 sales shifted to Q1.

2 Likes

as you may be aware, historically the maximum revenue happens in Q2 for all the agri chem companies including Dhanuka, Coromandel International and this Q2 should also be no different is my view. Then anyway the sales moderates, but this time TN sowing acreages have shown good growth and will do really well and they will put one more crop in the months of Oct and we have to see how the overall South performs in the coming months.

2 Likes

Attended the AGM today. I missed some part of the initial management address. The CDSL website is quiet complicated so no wonder most shareholders couldn’t join in. Some highlights:

-> Good monsoons throughout the year will continue to aid volumes and sales.

-> R&D facility spread over 6 acre at Palwal to be used for developing formulations of existing products.

-> Sales and development team of 500 people. Company has started creating a database of existing and new clients based on the crops they sow and the acreage. So far,database of 3 million farmers. This is used to intimate farmers about product launches and which product to buy when.

-> The dependence on monsoon will continue. Company expects this to reduce with water conservation practices gaining ground. Drip irrigation programs and “Nal se Jal” will aid this. But it will be long gestation.

-> Company is open for contract mfg. opportunities. Dhanuka expects Rabi season to be excellent this year as well. However,too early to say how exactly it will pan out.

-> Launched two new products,Kirari and Nissodium,via 4 virtual conferences. Both are very sophisticated products and resolve the powdery mildew issue in grapes. Initial response is very strong and company will sell out entire trial stock very soon. The total market size is 5-600cr.

If someone here attended too then please feel free to add more.

8 Likes

Dhanuka Agritech Buyback offer @1000 per Share , Record date fixed 28 Sept, 2020.

3 Likes

Dhanuka reported pretty decent set of numbers in Q2. The concall concluded some time back. Key highlights:

-> First month of Q2 was dry and then crop damage in major states affected revenue growth. However,company believes it has gained some market share on an overall basis.

-> Plan to launch 2 more molecules this financial year. And 6 in the next. Margins vary from molecule to molecule.

-> Working capital has improved but blurred due to high inventories. Post a strong Q1,company built up inventory but things didn’t go as planned. Expect to liquidate it in the coming 2 quarters,small spillover into next fy. Cash position of company remains healthy.

-> H2 has high base because Rabi season last fy was very strong for DAL. Company expects a Q2 type of growth rate in H2.

-> No issues on supply of RM since April. Prices are stable. (someone even asked about a war with China!)

-> Company is awaiting a project report to move further on their contract mfg. plans.

-> There is ample scope for growth for companies like DAL. Going into Fy22,company expects early double-digit growth assuming monsoons are normal.

This is all I could recall.

Disc. : Invested. Views are biased.

5 Likes