Anyone tracking this counter recently??.. rural theme is going to be on focus for next 18 months… how good is this counter to grab the opportunities??

Interesting article by moneylife

1 Like

Agree with you. Abnormal rise in receivables in FY 18 against flat sales, further aggravates corp. Governance issues. Management also does not seem hopeful about future prospects in the Q2 call as against the optimism displayed in the annual report. This does not seem to be a management with ambition. They give this 3 crore type of salaries totalling to 15 crores to several family members, leading to suspect whether the business is for providing salaries. Brilliant past performance. Poor future prospects. Buying back shares regularly seems to be the only viable option for the company.

On 22nd may 2018 Dhanuka’s statutory auditor, Ms Ambani & Associates resigned. There was no reason stated for resignation.

2 Likes

Dhanuka Agritech had a near save. On Friday their bank was about to release money via SVP when above stay order came. NCALT based biq aquistion by smaller companies is full of landmines.

Any views on the stock? It seems to be showing no resistance at any level on its way down. The downward journey has been steeper eversince the decision to pledge dhanuka agritech’s shares to fund Orchid pharma’s acquisition by Dhanuka labs.

insider trade: Pledge of 3,045,600 equity shares worth Rs 10000.23 lacs by promoter

1 Like

Dhanuka has fell from 900 levels in Jun 2017 to about 300 levels in Dec 2019. And in Dec 2019 it is showing reversal from 300 to 400. Emkay global has increased its target price and their reasoning is “Dhanuka Agritech’s focus on improving product mix by means of new launches should be visible from second half of FY20” I would have assumed all these to act out in early 2019. Does anybody in this group know something that i am missing?

Dhanuka Agritech Ltd. expects its overall sales to grow at the fastest pace in five years in the quarter ended December, led by a rise in herbicide sales and new specialty product launches.

“Last quarter (Dec.-end) was one of the best quarters in last five years,” MK Dhanuka, managing director at the agrochemical maker, said in an interview. “Strong rabi crop due to extended monsoon and spillover of demand from the second quarter due to weaker kharif season to lead to more than 20 percent growth. We expect the momentum to continue into the fourth quarter,” he said.

The company launched three products—Chempa (controls broad leaf and grassy weeds), Apply (controls brown plant hopper) and Largo (controls pests of cotton crops)—in the specialty segment during the kharif season, Dhanuka said. All the three molecules, according to him, have been received well and have started contributing “meaningful” to the company’s top and bottom line.

The company’s focus on improving the product mix by way of new launches and easing input cost pressure is also likely to aid margin. “We expect margins to start improving from third quarter and maintain our full-year guidance of 100-basis-points (1 percent) improvement in margins over the last financial year,” Dhanuka said. The agrochemical maker’s margin had hit a six-year low of 14.5 percent in 2018-19.

1 Like

Rs 12 dividend , seems promoter want to gain max before dividend taxation comes in. Whatelse could be the reason for such a dividend?

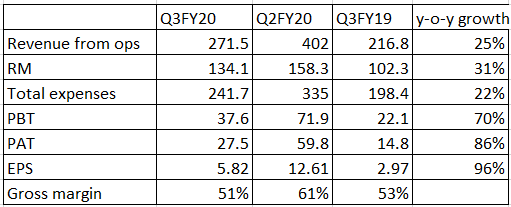

Yes, that seems to be the trend. Even Symphony announced quite a generous dividend few days back. But, excellent results from Dhanuka. PAT almost doubled. Much on the expected lines as the management already declared few weeks back that they have had one of the best Q3 ever.

Dhanuka delivered a good result in Q3. They had guided for >20% growth because of delay in Kharif crop. Had guided 16% EBITDA margin for full year FY20. They had commented that RM has come down but the impact was not seen in Q3 so probably Q4 should see good margin expansion.

From interview on CNBC today

Volume growth 27%, value growth 25%. Sowing increased 10% in Rabi season. Q4 is also expected to be good with similar 20% growth. Because of corona virus in China, some price increase is happening in India. Importing 3 pesticides directly from China, but buying technicals from China and Indian manufacturers. China is cheapest globally and even the players manufacturing in India are dependent on China for intermediates and chemicals so the overall exposure is higher. Since its a lean period in India so dont expect much of impact till March but if coronavirus problems continue beyond that, it can have an impact on Kharif season. Whatever is coming from China has no substitute. Most factories re-opened on 10th Feb so hoping normalization in short time.

The dividend puts 48cr cash in hands of promoters at a time when they are looking to acquire Orchid Pharma. The stock has rallied sharply by 60-70% in a span of 2 months. It was a great techno funda bet with double bottom at 290.

4 Likes

DhanukaAgritechLimited.pdf (946.5 KB)

A very good overview by Dhanuka Agritech management on the COVID situation. My view is that the company is in a very strong position, both financially and operationally, and will be even stronger on the other side of the COVID situation, some of the reasons being - Debt free balance sheet, this time of the year is usually an off-season for agro-chemicals companies therefore COVID has not impacted the peak season (unlike for some other industries), crude oil which is a key ingredient for raw-materials has crashed, this coupled with stimulus given by China to their local companies and huge pile up of inventory there have resulted in raw material prices to have significantly corrected (which is good for Dhanuka), supply chain not impacted to a large extent - supplies coming in from China and movement from them also happening as a result of agrochemicals been declared as ‘essential products’ even during lockdown. Further, the Govt is supporting farmers with MSP for their products and MNREGA, therefore cashflows for the farmers are being supported to a large extent. While other industries are reeling under reduced demand of their products during COVID, agri and food has not gone down, rather the demand has increased. Forecast is for a favorable monsoon this year which fares well for Kharif season. Payment on account of Orchid acquisition has been done and therefore the pledge on Dhanuka Agritech shares has been now revoked. As a result of the pesticide management bill announced last month there would be increased regulatory means around all the agro chemical producers, which will actually make it difficult for the fly-by-night operators for fake and scurrilous products to play in the market…augurs well for branded players like Dhanuka. Management expects for the industry to grow between 12-15% and Dhanuka to grow faster than that. Ofcourse, there would be challenges in the coming months on the collections due to overall financial crunch in the system, supporting the channel and management of working capital.

8 Likes

Fantastic set of results from Dhanuka. Net up 45%. Short interview and update from the management on the results here - https://twitter.com/CNBCTV18News/status/1270638299346989060

Management already has a good visibility of Q1 and believes strongly that it would be even better than Q4 results.

1 Like

Dhanuka Agri’s Q4 call was very intensive.Some highlights:

-

In Q4,2% of annual topline got deferred to Q1.Thus,Q4 revenue growth could’ve been ~30%

-

FY21 has started well.Launched 2 products in Q1,taking the tally to 7 new products over FY20 & FY21.The total mkt opportunity is 4-500cr.

-

The management will be attending a FICCI conference this week,regarding the draft notification on ban of 27 key products.The total market size is 4000cr. & an immediate ban will put a lot of pressure on the industry.Dhanuka & the rest of the industry will be able to replace these products over next 2-3 years with alternate ones but the prices of these alternatives are high.Thus,it will put undue pressure on the farmer at a critical time like this.Their recommendation seems to be a step-wise phasing out of the 27 products.Company is not against the idea of replacing,but all at one go is a bit too much.

-

Punjab,Haryana & Maharashtra are facing severe labour shortage.This has led to farmers using more herbicides & more mechanization.The net effect will be positive for DAL.However,this is only a short-term opportunity.Over the longer run company expects 10-15% as a reasonable rate of growth.

-

There is concerted action from the regulator,state governments & the industry about the agri industry.All are very serious about curtailing spurious products.This is positive for the industry as well as Dhanuka.

-

Company faced some logistic issues in April but situation improved by April-end.No such issue anymore.Transportation costs have increased but see no material impact on margins.

-

The pledging is on account of group company buying out Orchid Pharma.The shares should’ve been released by now but there is some “technical lacunae”.Expect resolution soon.

-

Company didn’t guide for a concrete number but company expects “very good” growth in FY21.Alongwith 100 bps improvement in EBITDA margins.Gross margins should also rise.

-

Dhanuka saw no delay in payments even in April,May.In fact,debtors continue to be stable and in-line with the rise in revenues.Capex for FY21 to be in the 5-10 cr. range.

The tone of the management was quiet upbeat.This is all I can recall.

Disc,: Invested.Views are biased.

8 Likes

From Edelweiss seminar

Key takeaways

A strong rabi season leading to higher crop production has lifted farmers’ income

levels. With government procurement levels on the higher side too, farmers’ liquidity

position remains sound, which will eventually drive overall agri-input consumption

during the kharif season.

The raw material situation from China has eased off post-April. However, due to

political tensions with China, some of the materials are still stuck at ports. A potential

hike in anti-dumping duty or a ban on chemicals from China would impact the overall

industry. Dhanuka Agritech has a roughly 5% exposure to China regarding

procurement of raw materials.

Based on improved sowing levels along with advance sales of agri-inputs during

Q1FY21, the company expects the kharif season to play out well for the overall

industry. Hence, it expects to achieve 20%-plus growth in FY21.

The government is likely to withdraw the proposed ban on 27 agrochemicals given the

concerns raised by the industry and the farmer community. Dhanuka believes the

government won’t take the drastic step given these molecules contribute around

INR80bn for the industry.

New products are likely to remain crucial in driving growth momentum. Though the

Innovation Turnover Index fell to 13% in FY20, the company believes it would improve

to 15% in FY21 driven by the success of Largo, Chempa and Apply.

Dhanuka’s core strengths are marketing and distribution-reach. Innovators want to

encash the profitability in the shortest possible time. Companies have an 85% margin

or thereabouts even after sharing a 15% margin with Dhanuka.

2 Likes

During April-June 2020 POS sale of fertilizers to farmers was 111.61 lakh MT which is higher by 82% compared to same period of last year.

(just as indicator of agriculture activity ,nothing directly related to Dhanuka agritech)

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1636187

With progression of monsoon across the country ongoing Kharif season looks goods. If the monsoon continues progress well and good water reservoir levels should be good for all agri related companies during present year including Rabi crop season.

Discl: invested

3 Likes