coming on a commodity question to you @ragsingh0305…

do u think the pricing of a commodity depends on the rm prices of it, or more on the demand and supply gap?

the C2H4 new production lines , imo, will fail to clear the inventories further, if they start passing on the rm prices of ethylene to the bearish market…

I think it depends on both. The selling price of a commodity products are usually determined by the cost of production of lowest cost producer. Raw material invariably is the largest cost component of a commodity product. Demand supply dynamics do play a critical role too.

Point…

A rebut question, can a.commodity producer pass on the rm prices when the demand is low?

I guess, thats the case when the demand is high rather…

But ultimately, i agree with u, as the pvc industry continue growth at 8pc cagr, ultimately these short term demand nosedive will be insignificant and if the crude dosent soften or stabilize below 70s, this is indeed a problem, unless dhabriya does something about it

Do u have any coverage on chlorine price trends and demand supply scene there and also calcium carbonate??

I am not finding enough data to do an analysis on these rms…

I will try to look for it. However I believe what matters the most in this case is the ability to pass on the cost to the consumer. These feedstocks (RM) are commodities, and are very difficult to form a view on them. If the company does reasonable degree of value add to its products, it can surely pass on the majority of the costs.

As I was checking if there are any other players in the listed space against whom Dhabriya can be compared, came across Fenesta Building system which is part of the DCM Shriram group.

Does any one know any other listed players in the uPVC Window/Door space?

Also is there a way we can track the prices of the RM which should give good insight.

Any inputs would be helpful.

PAT growth annual as 38.5%[fy17 vs fy18] compared to previous growth rate of 14.7% [fy16 vs fy17]

Topline growth 28%[fy17 vs 18] , vs 17.2%[fy16 vs fy17]

ebit margins remain flats at around 7%

consol debt to equity remains as 1.02 from 1.23 yoy…

in that, the long term debt has reduced from 51% to 41% of the total debt

massive jump in the inventory by 40% from 22.23cr to 31.14cr , this was a mere 13.75cr in 2016 march end and 28.4cr h1 end… [a point to worry about]

Receivables rise was a 7.25% and currently stands at 25.12cr from 23.42 cr…[went up to 28cr in h1 end]

receivable is equal to the working capital and 1.48 time the long term debt…

tangible asset stands at 41cr up, 8 percent yoy

asset turn over ratio stand at 1.25 vs 1.14 yoy , up 9.6%

while

operational topline to tangible asset stands at 3.22 vs 2.71 yoy, up 18 percent…

no exceptional items in this annual report…

a 8% jump in the other expense is noted, though minor, should be kept a tab on…

Roce=16.4% vs 14.5% yoy

over all , i like the growth trajectory being delivered at 50% capacity utilization, and keeping dstona which is currently at inception and the new bangalore plant contribution , at bay…

I couldnt yet get in touch with the promoters…

But i did, with Mr.sparsh jain who is the company secretary, who was not authorized to talk numbers about the company…

but 2 take away points that was discussed are…

The coimbatore plant which was built on leased land, has been in the process of transfer to bangalore where the company has bought land…

But the pollution control broad has not issued clearance , yet, and so the transfer has not materialized …

he mentions, there is nothing related to pollution in their plant to have an issue on, this is just the pace of government process thats causing the delay… there is no dispute with the pollution control board of TN which is causing this delay he confirmed

Dstona, has been operational since this year… although he didnt put a number on the estimates, but he did mention, the offtake has been much lower than expectation till date …

Will update further once i get in touch with the promoters…

Notes from my conversation with the management over the phone…

the TNPCB certification has been received and the construction in the Bangalore land has already started, they are in the process of transfer of the coimbatore plant which is built on lease hold land to the bangalore land which is owned by the company…

EXpected to complete transition by this financial year, maximum 7 to 10days of interruption od operations can be expected, whithout any visible effect…

The company uses lead based stabilizers in their upvc profiles, but the gov regulations regarding this dosent relate to the industry segment the company is involved with and has no effect whatsoever…

total capex done is 6cr…

the revenue is booked upder the plastic segment…

the sales are not as per expectation a of now, but with uptick of the realty sector if happens, tey are positive on the prospects…

this financial year, there has not been much of topline contribution worth mentioning…

potential topline that can be generated is 25cr, ebita margin around 20%

currently the capacity utilization of all the plant is 40 to 55% , the maximum capacity that can be utilized out of the installed number is 70%

unit I- malviya ind.area plant- installed capacity is 10, 000 mtpa including dstona

unit II-coimbatore - present capacity -18 lac sq feet per annum [expectes some more increment after the transition of the plant is completed]

unit III-ramchandrapur- 28lac sqft pa

In dynasty the revenue generation possible at maximum capacity utilization is 15-16cr per year, presently booked 3.89cr in fy19, this can double based on the current order book in this financial year…

the prices of pvc and resins that is used has firmed out, but they have a policy to revise their pricing on products 2 times per year, in that they mention they can comfortably pass on the price hike to the customers…

The modular furniture segment uses mdf, ply plastics as per customer needs, but hey mention they have no plans to backward integrate and go into manufacturing of MDF as of now…

CApex planned for fy19 is 3.5 to 4cr, ans is going to be along similar lines in coming few years, No major capex planned in 1-2 years atleast…

Further debt reduction is expected as they are having prepayment of debt in the worklist with the cash flow generation…

No target levels of debt or D/E ratio mentioned…

the accumulation of receivables is in part due to retention money due which is tobe expected in thier business… as all the projects that are undertaken keep 5 to 10percent of the order amount in retention until completion of the project…

There is no issue or plan or write off of any of the receivables however…

due to the capital intensive nature of the business and the wide range of products they produce, with in order inflow, they have to maintain a high inventory, majority of which is unfinished goods/raw materials in most times of the year…

hence the trend in the inventory is likely to continue in the rising or volatile …

NO numbers were mentioned in terms of the topline guidance n the margin amount…

But the performance of the past 1 to 2 years is likely to be maintained…

Currently, according to them, the real estate business is not in the best shape , which is affecting their growth specially after demonitization, rera and gst…

with revival in the sector, they are optimistic of better growth and improvement in margins…

The target of 200cr that has been doing round in some forums as a topline target issued by the promoters, is completely off, and the company has no such internal targets set as of now…

On dividend policy, the board is in discussion presently, may consider from the next financial year…

There is no franchising in their business model, only distribution and direct business witht he customers…

Hi @Capsule91 thanks for the details, helps to build the conviction, the only concern I see in this is the unorganized players in this space, for ex- I have been observing the uPVC windows, doors where ever I go these days - offices, hospitals etc.

Each of them have different product name which implies there is a huge unorganized market out there

Do you know what is the market share of Dhabriya and is there any threat for the company from the other players.(unlisted), by any chance did you ask them any questions on this topic

Yes i did ask questions on this line…

They didnt have number to share but they did mention their client base are big realty developers who generally seek quality and garauntee of teh products, to the tune that they generally block 5 to 10percent of the order in retention until the project is completed…

So in the segment where they play, they are very much directly linked to big ticket realty development where the unorganized players have lesser entry…

But i feel this is a given fact, so nothing new input regarding this…

I am waiting for the annual report , will approach them again with further questions, meanwhile, i am finding the stock to be technically weak and am avoiding buying into the dips as yet, maintaing part of the initial tracking investment…

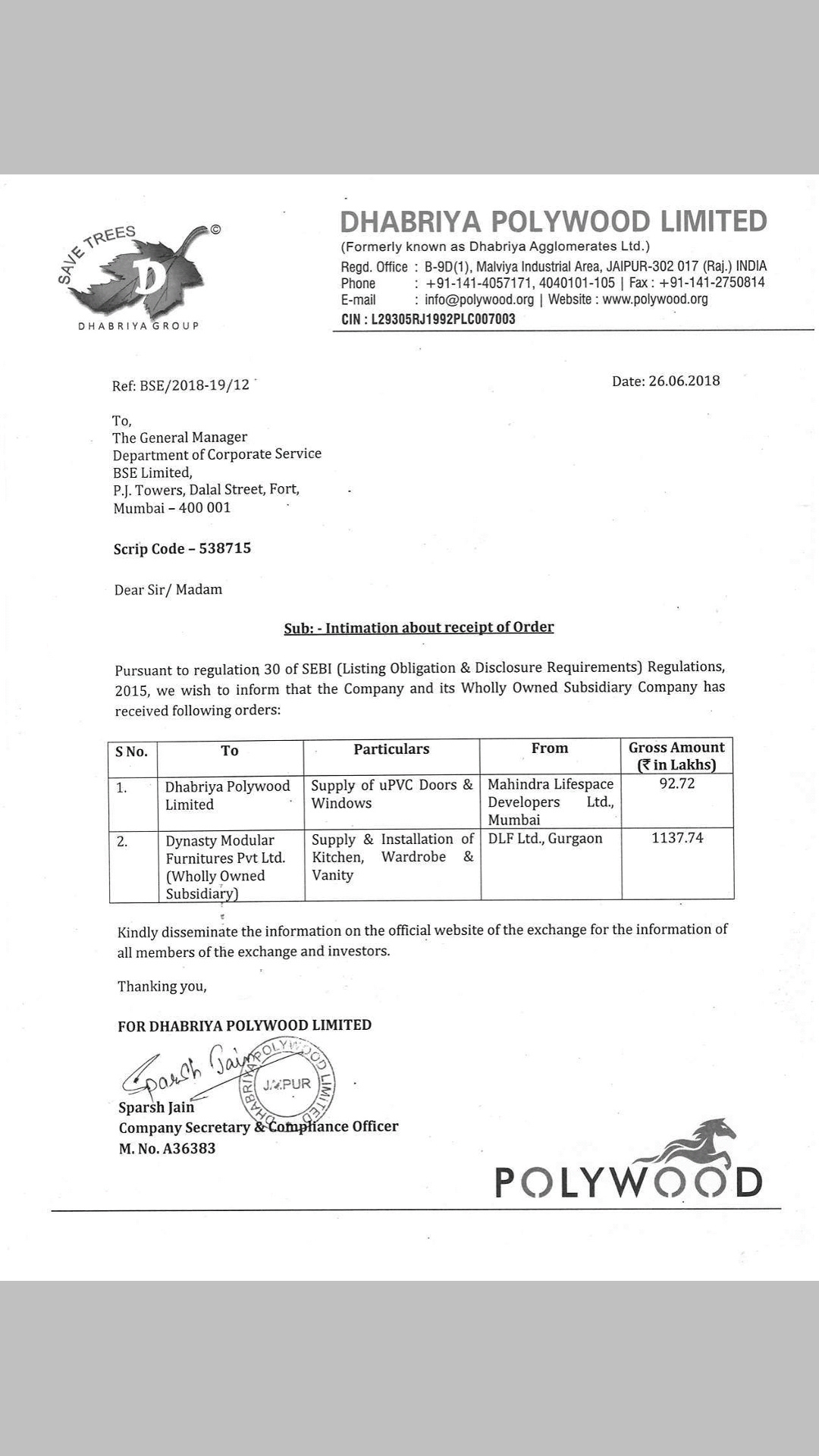

This looks positive and these disclosures brings in more conviction towards the business.

This also highlights the point you made earlier that they deal directly with builders for orders.