This could be a few qtrs before a sustainable improvements are seen. At annual basis it is 50+ PE. Expect some correction and thus opportunity.

Waiting to hear new mgmt prospective and strategy- concall or annual report.

Have some tracking position.

This could be a few qtrs before a sustainable improvements are seen. At annual basis it is 50+ PE. Expect some correction and thus opportunity.

Waiting to hear new mgmt prospective and strategy- concall or annual report.

Have some tracking position.

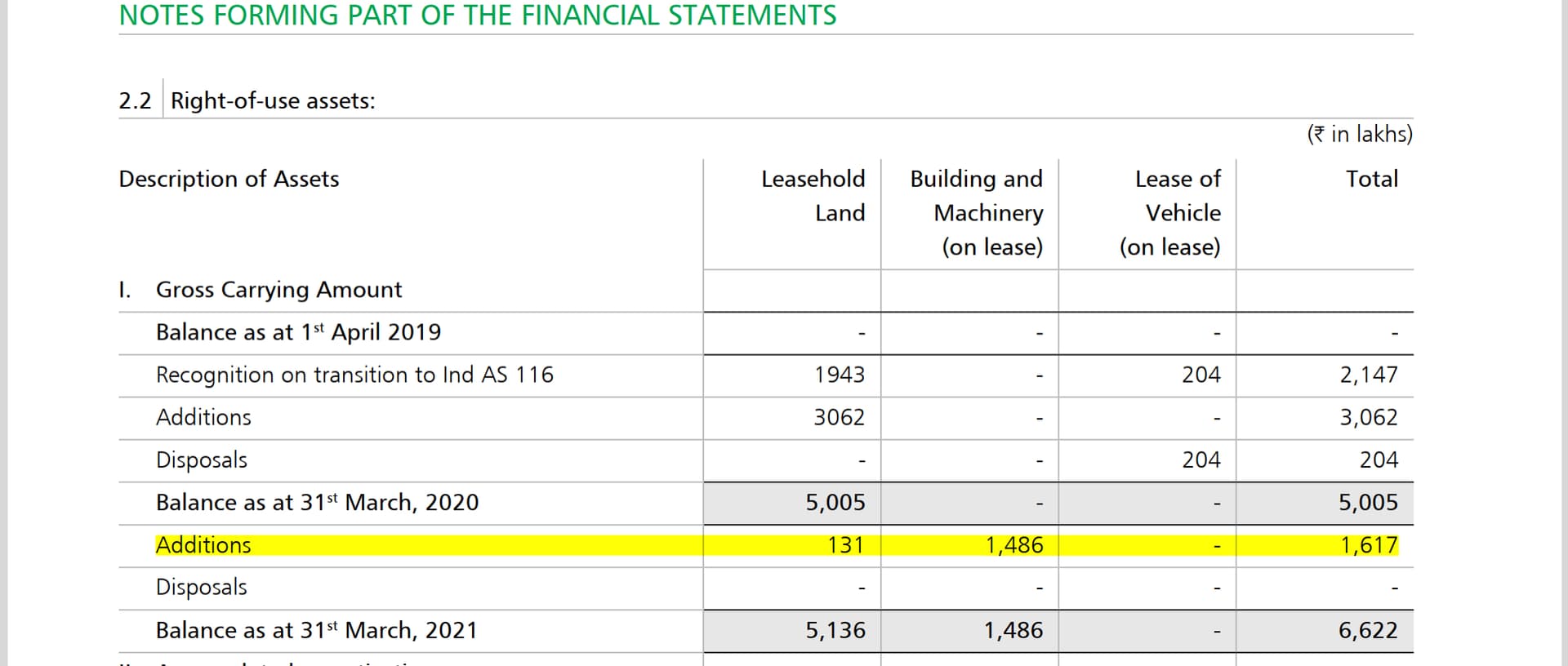

Even though PAT is down for the year from Rs.33 crore to Rs.24 crore, tax outgo in the cash flow statement remains the same at Rs.10.61 crore (against Rs.10.51 crore last year). That too in a year when tax rates have been reduced! How to read this?

Bad results!

Despite profits not recommending dividend. What is the signal being given?

Important for mgmt to share strategy

Change in Ad agency

Hi,

Just wanted to ask if you have any idea as to how these big PE players exit these companies? Can you point me to any previous examples that you know of?

Don’t understand why should investors need to know every change in supplier/service provider.

It is material to some of us to see the quality/clientele of agency for a consumer brand…akin to an auditor rapport , agency rapport is equally imp… also tells about changes new mgmt is bringing in directionally

Hi,

PE players generally try to leverage the growth of an existing/promising company with the aim of exiting it within 5 years or so with decent returns.

Some previous examples I can think of currently are La Opala, Vmart, Relaxo had Westbridge backing in them and led to a spurt in their growth.

Advent backing in DFM seems interesting and it has changed the management hoping for aggressive product launches in near future (although, the current pandemic situation might defer the timeline by 2-3 quarters)

Other PR investments by Advent in India are ASK PMS (around 40% ownership), CAMS, Manjushree Technpack Limited, Cromton as listed in their website.

A very disappointing AGM by DFM Foods.

While the quality of questions was surprisingly good (unlike the nonsense we frequently see), the management did not answer a single question with proper specifics. Most of the answers were vague platitudes like “we will continue to strengthen blah blah blah… continue to improve blah blah blah…” without providing any specifics such as the company’s product-wise sales, geographical distribution, dealer network, production capacity, future launches etc. They did not even commit on whether they can publish a proper investor presentation or hold quarterly analyst call in future. Management did not answer how they managed such strong sales in Q1 despite the lockdown – other than saying it proves the strength of our brand.

The Annual Report was disappointing too, with little information beyond what is statutorily required.

In June, the management made the mandatory COVID-related disclosure by providing an update “upto 31st March 2020” ! To say in June that our factories were shut from 22nd March to 31st March is nothing short of an insult to investor since factories had started opening in May. It is also a mockery of SEBI circular which asked listed entities to provide “…timely, adequate and updated information…”.

Agreed the management team is new, but still some of these things are difficult to digest.

(Disc.: Tracking position)

Decent performance, inspite of full lockdowns for school and education institutions and out of home segments not fully recovered, rise in input costs such as edible oil etc.

On a Y-o-Y basis, Q2 Revenue grew by 4.0% & PBT grew by 9.5%

On Q-o-Q basis Revenue grew by 22.9% & PBT by 31.1%

Agree with the ask that a proper investor update and presentation would help uplift image and transparency, as well as project new management professional ways - its a miss.

This time we have better Investor Presentation. Good thing is that they have negative working capital.

Anyone can please share DFM foods concall transcript ?

Notes from Annual report - focus on mgmt and industry outlook

While numbers are yet to reflect high growth trajectory, believe foundation blocks are in place, mgmt quality is top notch and resiliene was visible in FY21. All in all interesting times ahead.

Invested

Annual Report

The Company is a leading player in the snack foods market in India, and our brand Crax is a household name in the country. The Company manufactures products across the range in salty snacks including extruded, namkeens and has recently launch potato chips. There are two state-of-the-art processing facilities at Ghaziabad, and Greater Noida region both near the Company’s Corporate office in Noida that manufacture the salty snacks. The Company also operates through third party contract manufacturer at Kashipur (Uttarakhand). With product differentiation, aggressive marketing, and a focus on high quality, the company is growing at a steady pace over the last 10 years

The Company keeps innovating on new products and flavours. This year, the Company launched a new product ‘Crax Bowls’ and two new flavours. The Company also has a wide network of distributors that provides it reach across the country. The Company has also been aggressively building the Crax brand through investments in TV and digital advertisements. The Company is the market leader in extruded snacks segment in the country. The mix of best-in-class production facilities, aggressive marketing and deep distribution network gives the Company a competitive edge over the competitors in the segment. The Company is well positioned to make most of the growth in the industry and switch to organised players.

Business Developments

There is a huge headroom to grow through further strengthening our current product portfolio in existing geographies, expansion into new geographies, building larger pack portfolio (Rs 10/- and above) and innovation into premium segments

While DFM would continue to drive growth in the traditional trade and route to market, it is also looking at aggressively increasing its footprint in alternate channels such as e-Commerce and modern trade. Several new initiatives have been piloted to strengthen our capability in channels of the future. DFM will continue to collaborate with key players in e-Commerce and Modern Trade to drive strategic priorities.

Further our initiatives for FY 2021-22 would be to decentralise third party (3P) facilities enabling optimising logistic cost with the source of supply being closer to the market.

Annual Report contd…

Despite the challenging environment witnessed last year we were able to increase our market share by 187 basis points in the extruded category thereby further strengthening our leadership position. Further, through a selective approach of efficiently leveraging each channel of sales we were also able to take our distribution reach to a 2 year high.

With the aim of taking the sales function to the next level of growth and efficiency, we also began the rollout of sales force automation in the North as well as East regions. Sales automation holds the potential to reduce the cost of sales by freeing up time spent on administration and reporting and to unlock additional revenue by automating outreach to customers in the sales funnel. The value unlock that the sales automation can create will bear results across the entire range of sales and industry dynamics.

We intend to double down on our direct retail presence in India in both, urban and rural, markets and build a strong foundation for the years ahead thereby having a direct impact on growing our revenues substantially. While we continue to focus on enhancing our sales system, and on active retailing, a great focus is being given on greatly enhancing our omni channel presence. With omni channel shopping becoming more and more pervasive, embracing these trends effectively, promptly, and comfortably can enhance our competitive positions. Further, we plan to constantly upgrade our distribution and supply chain network and re-frame our go-to market strategies to ensure ready availability of our products.

Annual Report Contd…

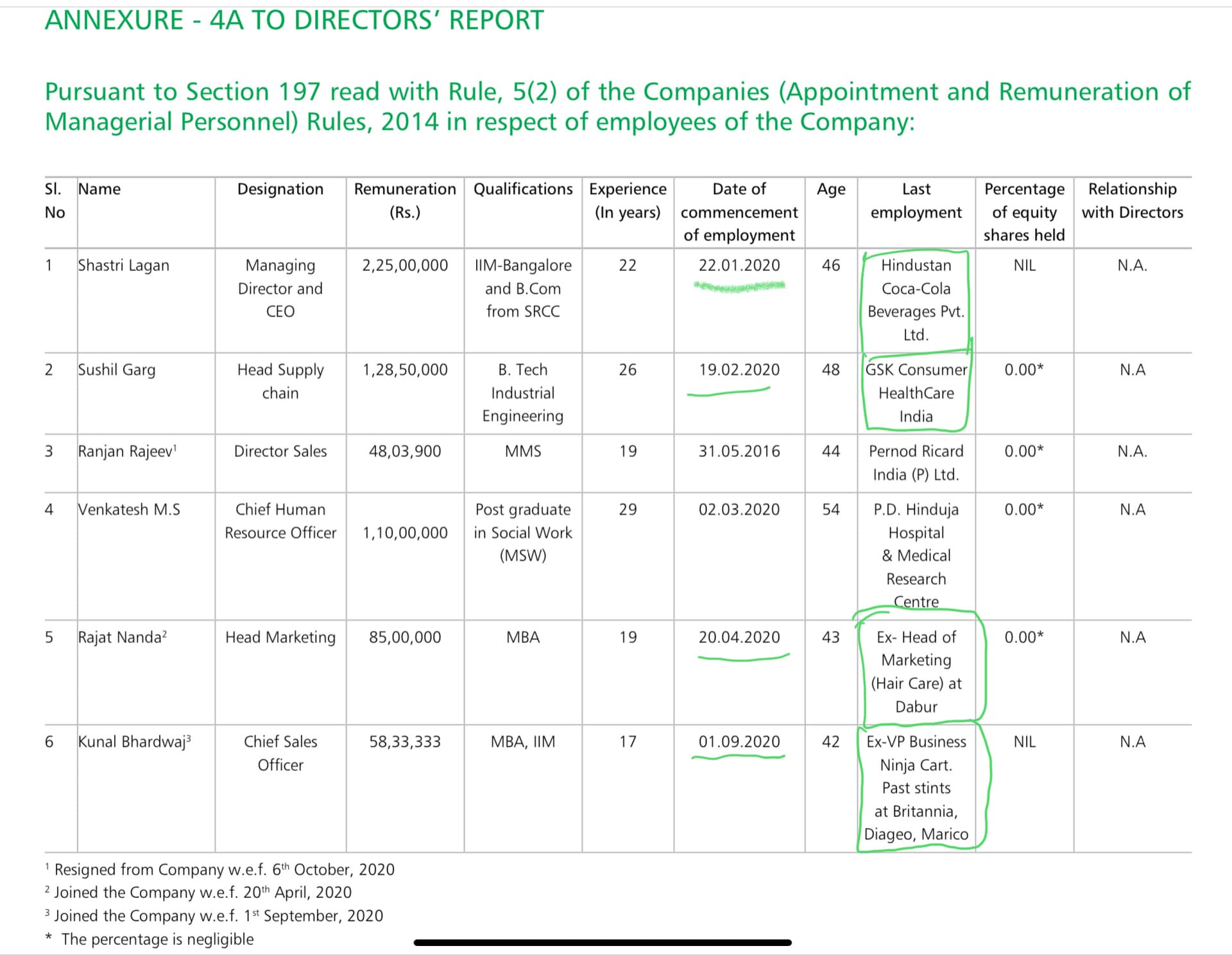

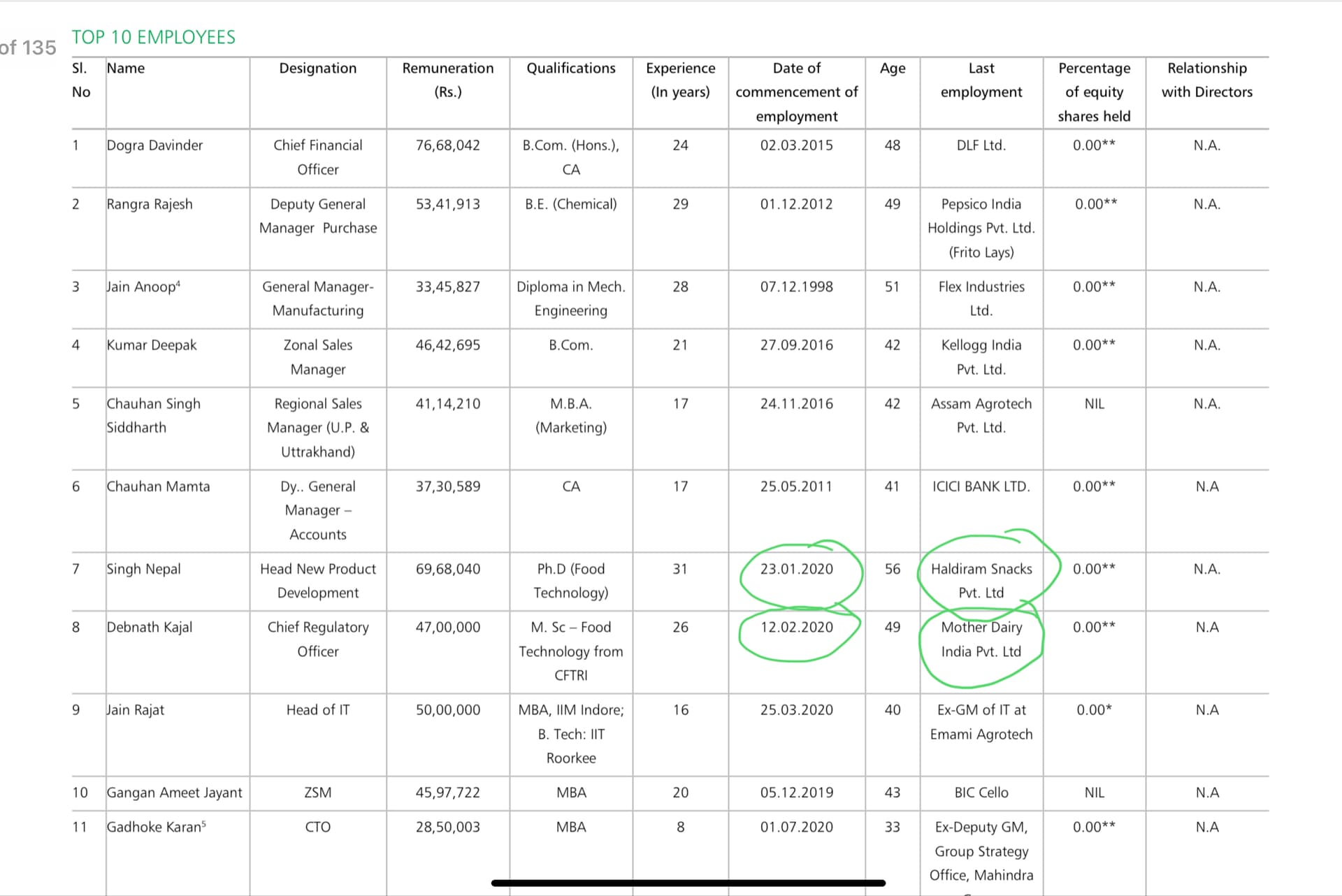

Management Change and Important Employee addition

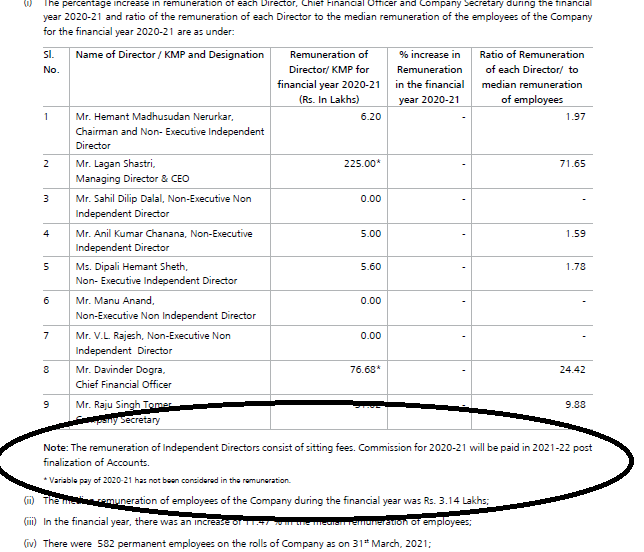

I found the following in DFM Foods Annual Report:

With respect to the above, I note the following:

What does “post finalization of accounts” mean here since finalization has already happened. This is from the Annual Report itself.

Secondly, even if actual payments for both the above items happen in FY2021-22, is it not necessary to account for them in FY2020-21 on accrual basis?

Can someone clarify if I am missing something.

(Disc: No positions)

To me , it appears that this table (remuneration of directors) was prepared before the finalisation of FY accounts. It may have been accounted for already and therefore it is already EBITDA relevant for FY20-21. However, it may not be reflected in the cash-flow statements. And therefore this disclaimer was necessary.

The Company’s Policy relating to appointment of Directors, payment of Managerial remuneration, Directors’ qualifications, positive attributes, independence of

Directors and other related matters as provided under Section 178(3) of the Companies Act, 2013 is furnished in Annexure – 1 and forms part of this Report. The Policy is also available in the Investor Relations, on the website of the Company and can be accessed at the weblink: ( http://www. Healthy Snack Foods Manufacturer for Kids | DFM Foods and%20Remuneration%20Policy%20DFM.pdf)

As per this policy clause… 4-8

Quote

The remuneration to the Non-executive Directors (including Independent Directors) may be paid within the monetary limit approved by shareholders, subject to the limit not exceeding 1% of the profits of the Company computed as per the applicable provisions of the Companies Act, 2013.

Unquote

I think after induction of new management, remuneration increased more than 1 % of limit. Net Profit also down on Covid impact.

that why this is deferred for next FY.