CARE has removed the ratings from ‘Credit Watch with Developing Implications’, re-affirmed of ratings and assign the outlook as ‘Stable’ of the bank facilities of DFM Foods Limited (DFMFL) following the closure of sale of stake of Promoter, PE Investor Westbridge Crossover fund LLC and other investors to AI Global Investments (Cyprus) PCC Limited (AIGIPL). AIGIPL has acquired 73.94% of the paid-up share capital.

http://www.careratings.com/upload/CompanyFiles/PR/DFM%20Foods%20Limited-02-25-2020.pdf

1 Like

Looking for a bear case here.

Advent has bought substantial stake (about 75%) in the last quarter. This is now higher than the earlier 67% reported in the deal. This has happened at around 250/sh. Overhang on the stock, in terms of pledge is gone. Advent should bring in a capable management (They seem to have roped in a ex-Coke guy). I just looked at their track record (Crompton is a good local example).

Looks like they do this often and so should have reasonable experience in growing businesses.

https://www.adventinternational.com/investments/?region=&country=§or=17&keywords=&col_order=

DFM hasn’t done too badly as a business if you look at a 10 year track record. Topline has grown about 7x and bottomline about 10x (Roughly 4x in both if you use FY11) which isn’t bad. I see Crax available even in the kirana near me.

Current valuations aren’t too demanding (especially if you anchor around Advent’s 75% stake buyout price). Its currently at a 30% discount to that price.

Is there a lot to lose from here?

Disc: Been buying around 170 levels over last two weeks

9 Likes

Not invested. My only thought on Crax is that in this extruded snacks / namkeen space, all the major heavy weights are manned by people who built bottom up businesses in these areas - I’m not sure if a professional FMCG team can crack it the same way - no real substantiation for this, just a doubt - I think the risk here is failure of / slow integration of teams and leadership churn. Also no fresh capital came into the business though access to debt should improve, which may prompt heavier balance sheet utilization.

Plant closed from 28th March as crax doesn’t fall under essential item & sales would drop significantly. Quite possible people may differ non esssntial purchase due to job cuts and lower income …Volatility in raw material prices… Hardly any dividend yield (not even 1 percent) & when there are many good options available at good dividend yield…

As per screener, Pledged percentage is 85%. Is this an issue ??

The Pledge was released before the old promoter sold the stake to the new promoter. Bse disclosures have the information.

2 Likes

The pledge was by previous promotes.Currently the promoter is Advent Capital which is a Private Equity company with a good track record.

Thanks. This implies that screener data is not upto date - which is a serious issue since many of us depend solely and blindly on screener.in data.

Some errors are inevitable. If something of interest found, as an investor we need to get the numbers confirmed in ARs and BSE/NSE

This actually is a serious issue ! Please note Screener.in is an excellent tool, but it should be used only as a starting point of your analyses. Use it to create a shortlist and then you have to do further research by other means before investing.

1 Like

There is no issue with screener. Once u check insider trades in bse u get to know that pledge was released before selling (which is an obvious requirement before selling stock)

The shares holding pattern is updated once a qtr. Once that is updated one would get updated value in screener.

2 Likes

Gaurav,

Thanks for your insights. I already have holdings in DFM foods and was thinking of increasing. I am quite lured by the fact that a good company is now handling and has 75% stake in the company (talking abt Advent). I completely agree that the factories are closed as this doesnt come under essential items but isnt this all discounted? It is trading at 170-180rs which is at a 50% discount from it’s recent prices of 300. If everything was hunky dory it would fall or may be trade like other companies (D-mart,Nestle, HUL etc).

P.S.: Not comparing this with Nestle, HUL etc. Just trying to make a point

1 Like

Since the plants are closed…do we have idea on the approximate inventory they already have (before the shutdown). Also when are they planning to announce 4th Quarter results ? There has been no note from the management on the impact of COVID

even i have DFM on my watch list… but i feel its best to wait for a quarter of results… loss of production due to lock-down would definitely impact earnings and when things do open up also its not like they would be able to produce at full capacity and make products available everywhere… so i expect prices to correct a bit more… giving a very lucrative opportunity below 150s… where it should easily give 5x in 5 years…

1 Like

I spent sometime to understand the end demand, my understanding it that the product is focused around school going kids and targeting their pocket money.

In current scenario when schools are closed and might not open even till June - I would expect significant impact in Apr-Jun qtr numbers.

Having said that shouldn’t materially impact terminal value.

1 Like

Resumption Of Partial Operations

1 Like

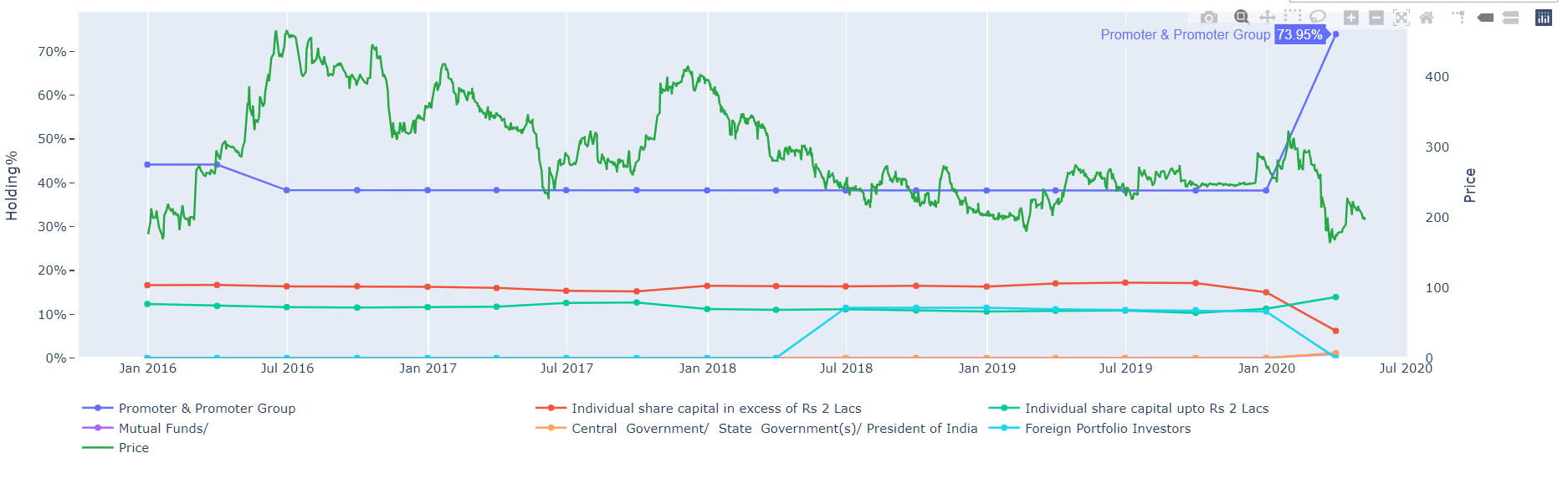

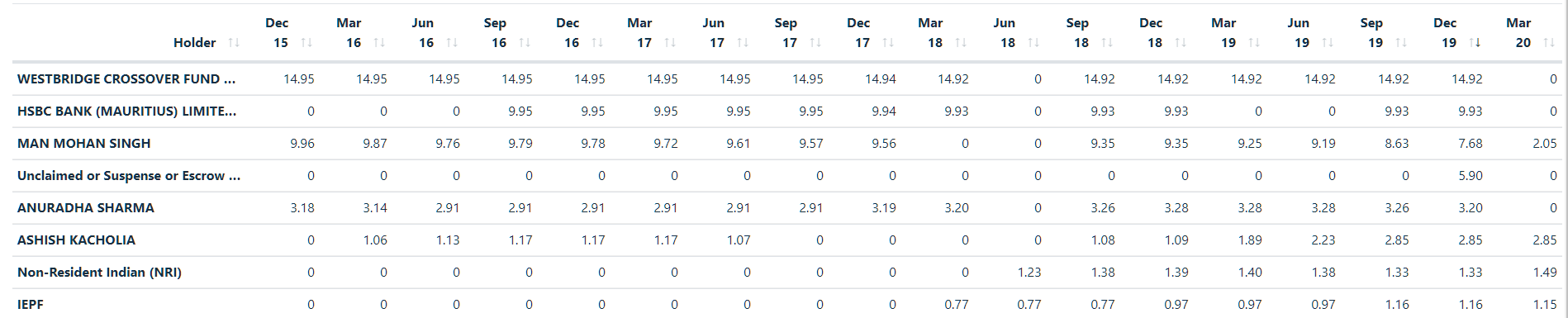

Latest shareholding change after Advent entry shows their holding at ~74% and hence the large jump in promoter holding from ~38% to ~74%. Promoter pledge consequently is zero now.

Westbridge, HSBC and Anuradha Sharma’s holdings are also zero now.

Hopefully overhang from the past isn’t much and the company can set a new course for itself under the new management.

Disc: Invested

2 Likes

Guys wanted to know from you all if the company will be more valuable 5-10 years down the line and the business is good. Why did the promotors sold out their stake? I can understand westbridge selling,but why did promotors sell out if they know the business is good and would be more valuable 5-10 years down the line? As it is they were associated with it for 30+ years

I don’t think the old promoters were able to grow the business to its full potential, probably because their interests were not fully in it. They were leveraged through equity pledge probably to promote their other interests and perhaps had little option but to sell their stake at the reasonable valuation offered by Advent. Generally when management changes like this happens in a stagnating business, most of the policies that did not work out are thrown out - it is easy for a new management to do it than for the old one which had a commitment bias towards it.

Professional managements have generally run businesses better but it is hard for promoter-owned and operated entities to give up operational control, although it is vital after reaching a certain stage of growth. I think the sort of person Advent has chosen, Lagan Shastri, IIM-B Alumnus with 22 years exp in Coca-Cola India (last role: Exec Director of Market Operations) could do that job. At this point though it is all a possibility/hope thing. The management has to prove itself and show its strategy and then prove it with execution.

PE firms like Advent come with a focus on growth and can leverage experiences from operating around the world in similar businesses to achieve that. Let’s see how it goes over the next 2 years in terms of decisions taken by the management and that should give us an idea.

18 Likes

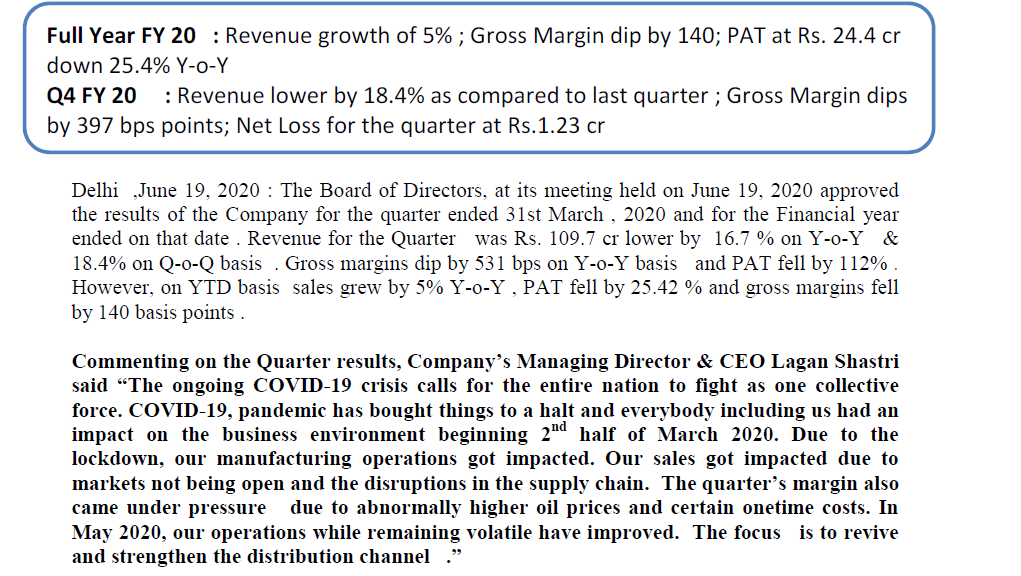

Poor results for the quarter.

Looks like house cleaning (refer CEO’s comment about certain one time costs)has started by the new promoters.

Disclosure - No investment. On watchlist.

2 Likes