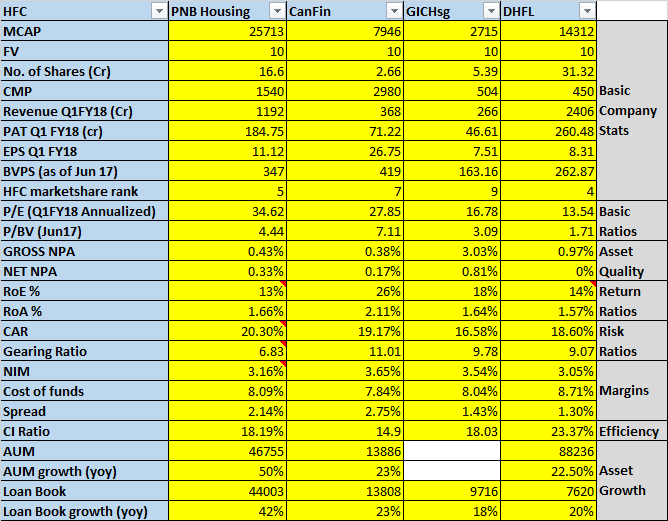

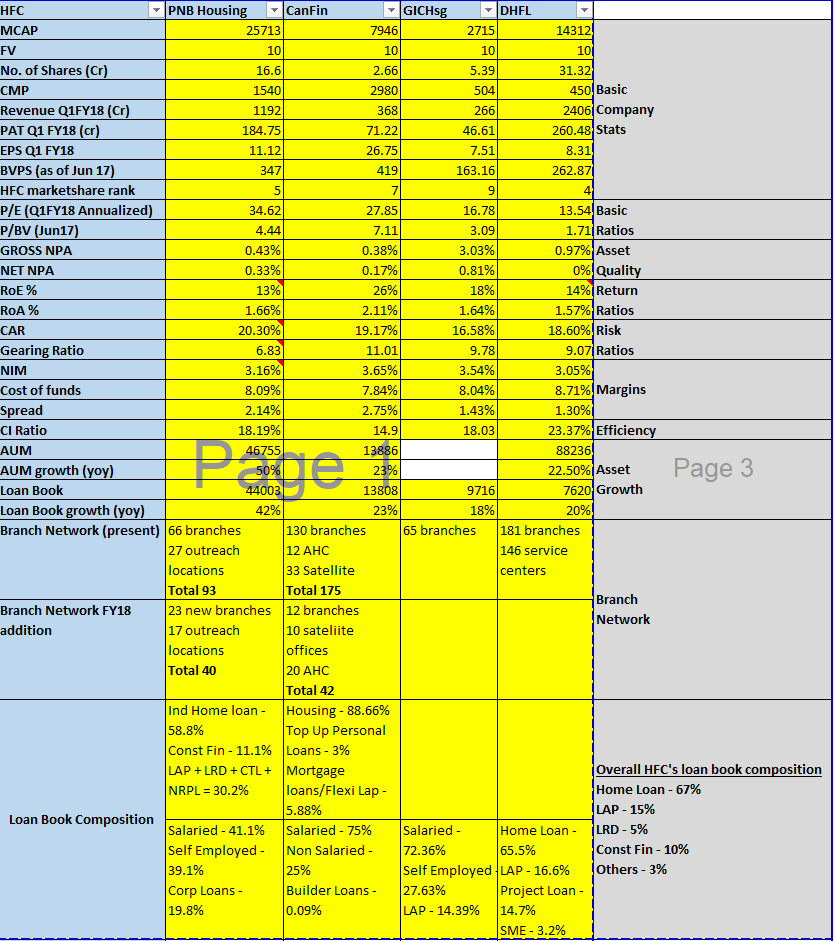

One important criteria you shud add to the above table is loan book mix…v. important from the loan book quality perspective.

One more thing that could be included in this presentation should share of developer loan and lap segment otherwise everything else is perfect

nice work … Thanks …

Good work. One small correction, DHFL spread is 3%.

Added a few more parameters to the HFC-comparison sheet including the all-important loan book composition.

3% for DHFL should be the NIM and not spread i believe.

As per management in Q1FY18 conference call, their yield is 11.4%. It means spread is 2.7%.

This is great. On paper, DHFL should be at much higher valuations than where it stands. So question is why is Mr. Market not giving DHFL it’s due?

There are also unexplained falls of 3-5% for DHFL without any news regarding the company. What are we missing?

Probably some vague connection with HDIL as promoters are related. HDIL has fallen due to NCLT proceedings against it. This is a personal view - pure conjecture

Beyond my understanding why market is valuing dhfl

at such a lower valuation? Mainly operate in tier 2 3 towns where the competition is less. Frequent equity dilution…? Even though profit has grew at cagr 34.4% in last 5 years, eps was only 18.1%. But now they have enough capital and as per management no capital required in next 3 to 4 years

DHFL has already undergone a rerating in the past one year. At 195 levels 15 months back, it used to trade at a discount to book. so its come a long way. Rerating from here on is quite possible and Mr. Market will wait for evidence of consistent results from here on.

This has baffled me from last 4 years when I bought the stock.

My Assumptions for potential concerns:

1 . Relationship with HDIL promoters.

2. Some corporate actions( I remember when they bought primarica from dhfl they did not provide any financial details ) since recently they have started sharing details and conference calls on specific topic and since new CEO joined.

3 I have read one article about DHFL accounting policies from a fund manager. Details were not provided but I assumed something is up. Pic is attached at end of this post.

- Initially there were concerns that promoters have very less shareholding then when promoters issued themselves warrants at higher price to increase shareholding there were concerns about the path taken to increase shareholding.

I have shares since 2013, these are my assumptions. May not be real concerns. I am still invested.point-3 really worries me sometime as I do not understand numbers that well may be fund manager do.

Interesting moves in last 3 weeks for 4 HFC’s i track:

Jun17 P/B moves:

PNB: 4.29-> 4.68

Canfin: 6.89-> 6.85

GIC: 2.91-> 3.29

DHFL: 1.59 -> 1.96

DHFL promoters are exploring options to clean up the structure, which should help value unlocking.

I would expect the promoters to be rational enough to realise that the market is discounting the valuation of the company given the complex structure and perceived lack of corporate governance. High time for them to clean the structure and create shareholder value similar to several other players in the market.

The imminent listing of reliance home finance should give them a hint about the valuations offered by Mr.Market. It’s high time they come out their lethargy.

This is the cheapest HFC available…Markets not having a favourable opinion on the management due to past history but i believe the perception problem can away quickly if the management deliv

ers as the fundamentals are in tact.

Just curious, What happened?