DHFL seems to have done it again - make the current price look ridiculously low.

This seems to be another common strategy in the current scenario. And this is actually a good strategy these days when management guidance is a good substitute for stock analysis - give direction to the investors and lead them to a target which is high enough but not unreasonable. And it comes after a decent performance in the recent past say 1-2 qtrs for it to sound believable and then let investors read it along with the tailwinds in the sector and or the prevailing bullishness such that the current valuation if high gets justified and if low makes investors feel like buying more. In either case, you end up creating a base for your share price. Last they did this was when they infused 2k cr out of thin air. The price then was around 320 and till that time what seemed like peak price became base price after the news and actually looked ridiculous in light of the news. This interview may well have the same effect cause as far as I remember this is the first time Dhawan has given a direction in such clear terms as a three yr AUM and RoE guidance which if achieved makes the current price look ridiculously low. And this coupled with his comments on perception issues is like challenging the investing community like a daredevil

Rgds

RR

Still invested

Property value of BKC is said to be 500 crores. ( as per media reports)

-

If 10,000 crore is net worth of company (as per Kapil) then this should increase 5 % of net worth.

-

It will take care for 0.5 year of cash without diluting

-

Total average cost of funds should go down as 2500 crore (2000 earlier +500) raised with no cost.

-

It will add to bottom line. It is a two quarter profit.

-

Current PE is around 16. Can they grow more than 20 percent yoy next three years? I don’t know.

PS: I have very early position in dhfl. Thinking about if this is a short term trading opportunity?

Of-course this may not materialize and nothing may change.

Please point out errors in my assumptions.

Puneet

I have no way of knowing how they will reach close to 10k cr in NW by 2018. it could be a combination of PAT gr in excess of 32-35% over 2017 (a gr rate that is double of last 4-yr’s avg); sale of BKC prop for 650cr plus (a value far more than expected and in cash); stake sale in other grp companies like AMC (which isn’t expected as of now), etc. They will certainly need to pull quite a few rabbits out their hat

If it does happen it would mean doubling BV in 2 yrs ie over 2016 (don’t know who else did that last ) …then it is not unlikely for price to be 4-5 times of 2016.

Apart from the usual risks, the biggest risk wud continue to be little change in investor perception (that maybe their loan book contains more risky assets and that they don’t follow prudent accounting policies) and it’s old reputation may keep haunting investors even though they may not find much in reality. It can well perform better than Gruh across this long 5-yr period of 2016 to 2021 on most performance metrics but the investors may never give it a 8-10 p/b…unless we hv far more foreign investors in India with limited Indian memories but continuation of improved performance can certainly get it to a p/b of 3-4 in 2-3 yrs.

Most of the above could well be seen as wishful thinking )

Rgds

RR

Hi I met the management of DHFL during the JPM India conference in a group meeting (CEO - Harshil, CBO - Santosh Nair and one more person) Here are my takeways - the main concern probably for global investos was corp governance which the CEO tried to address during this meeting.

They came across as genuine people. Let me know if you have any questions and if they spoke about it, I’ll answer.

• Can you share your outlook on the competitive intensity? Competition was always there and it’s going to be more intense going forward given the prospects of the sector. Competition helps us stay on our feet – we made key leadership changes – 1) Santosh Nair is our current CBO (ex HDFC – running the mortgage business for 16 years) and 2) Vivek who is our COO ( ex Citi where he was head of the backend team)

• On competition have you been seeing a lot of prepayments / balance transfers? Its like a give and take – somebody takes our customers and we also reach out to other customers and give them good structured options. There are 2 types of prepayments – general and balance transfers. From a balance transfer perspective – the prepayments rate is around 3-3.5% and this is constant across the industry.

• Is there pressure to take on customers that are less credit worthy? There is no such undue pressure – we only fund people who meet our requirement. All companies are allowed to lend as per their credit norms by the government. CEO: There is no data available anywhere on the home loan segment in India that states that this segment is high risk.

• Can you describe the impact of RERA on the segment and your outlook on it? This will take us around 90-180 days more to form some conclusion about this. As of now there is a mixed reaction to it. We operate a lot in Tier2/3 kind of markets which has the smaller builders. We could see larger builders who have registered under RERA work with the smaller ones who don’t want to register but have local expertise. For us, this consolidation will benefit us.

• What are your thoughts on the schemes of affordable housing? There is demand-supply gap which remains where demand is far more. Initiatives like classification of housing under infrastructure status etc will help the sector – so we believe additional supply should start coming in around 24 months but the gap will remain. We are holding conclaves in Tier2/3 markets on weekends where we bring 12 builders under one roof and we also advertise this to customers and there are good booking nos in these conclaves.

• DHFL is plagued by a lot a corporate governance issues. Can you elaborate on that? CEO: Since I have started meeting investors, there are basically four issues which people exist are: 1) DHFL-HDIL connection. – DHFL and HDIL have family relations and Kapil (Chairman - DHFL) and Sunny (CEO - HDIL) are first cousins. In 2009-2010 they split the businesses where HDIL went to Sunny and Kapil got DHFL. All cross holdings were then sorted out and now there are none, 2) Another issue was that there was there was HDIL Tower (real estate office building) which was split between HDIL and DHFL – 4 floors each. DHFL took then a decision to shift main management to a BKC building since there were concerns that both managements were operating from the same building. Then we bought a new building to remove stakeholders – we bought in 2012-13 a new place for 750crs in Kalina and this was all disclosed. Then people had concerns about this purchase as well. Now DHFL has taken a call is to exit that purchased property and get the money back. This now is shown in the BS as work in progress of 500cr. We paid 750 for some height allowance payments but since we didn’t get the permissions we got 250cr back. And now since people know that we want to dispose it off – we are getting lower price offers so we have held on to it 3) There is no exposure of DHFL in the business of HDIL – and not in its sister companies, But DHFL does provide home loan for HDIL customers as its pure business where the counter party is the customer and not HDIL. 4) Last issue was, that given DHFL’s size why wasn’t one of the Big4 an auditor? – The auditor then was TR Chaddha. So we moved away midway and got – Chaturvedi and Shah – as the statutory auditor and Deloitte as the management auditor.

Disc- Not invested and not looking to at these levels

Thank you Rahul.

Here is one of the glimpse of what happened in 2010 when I wasn’t tracking the company.

Summary : DHFL and HDIL promoters together executed non disposal undertaking of some cross holding of dhfl/HDIL shares to get ECB loan from icici canada. 50mn.

They failed to disclose it to exchanges.

Case went to Sebi. They were acquitted as no confirmed ground were found as there is technical difference between what should be disclosed “pledge” shares or Non disposable undertaking which is a type of encumbrance .

It at-least establishes HDIL and DHfl were not working in arms length. Ofcourse foreign investors or long term investors may want to stay away from company.

We haven’t seen such thing in last few years. But we should agree amount of disclosures have become better only in last 2 years or so since new ceo has come. I remember there was no information regarding when they bought a dlf insurance company in 2013. What was the price paid? How etc. I had to mail a crisil analyst to get the information.

My learning is we have to keep watching everything with microscope.

On the contrary if management is taking right steps now and If market is wrong now then in due time it should reward the management, company and investors.

Here are details of case:

Puneet

Strong Q2 Numbers from DHFL

YoY

Revenues up 21%

Profit up 26%

Disbursement up 51%

Loan Sanctioned up 68%

Interim dividend declared Rs. 3/Share.

Sanctions and disbursements growth of more than 50% for a large company like Dewan shows we are looking towards exciting couple of years. Signs of tailwinds for housing finance companies are starting to show.

Despite the significant reduction in cost of funds and C/I ratio, its taken a steady shift away from pure home loans to riskier products to be able to maintain the same NIMs (Q2 vs Q1).

Dialed in to JM Financial concal yesterday which also does real estate funding and I quote them verbatim "The real estate sector is undergoing SEVERE stress across geographies where we operate."

JM does most of its business in Mumbai, Pune and Bangalore.

Also, JM is seeing yields drop in riskier products along with reduced asset covers (2x to 1.5x) required by competition oflate.

If I have to link up the commentary between the two, I would surmise that DHFL is clearly chasing growth in riskier products and at the cost of margins which surely are headed south of 3%.

DHFL is targeting tier-2 and tier-3 cities, and not just builder-driven properties. Home construction loans are getting larger. They are also doing excellent marketing for PMAY, which I think the big players in metro and big cities are missing. So it seems like a mix of interesting strategy, government subsidy and lower cost of borrowing, all working in their favor.

Still, the bullish commentary and goals for 2020 seemed like unrealistic. The latest quarterly results give some confidence, but sustaining it will be a challenge.

Disc: invested since 2011 and over 15% of portfolio now.

@hemtan100 Thanks for the details. Can you tell me where can i get loan bifurcation for sectors and comparison of that on a QoQ basis for DHFL?

Regards,

Suhag

DHFL Earning Presentation Q2 2018.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/eacca2f8-8d08-4e0d-b8c4-ab28645df829.pdf

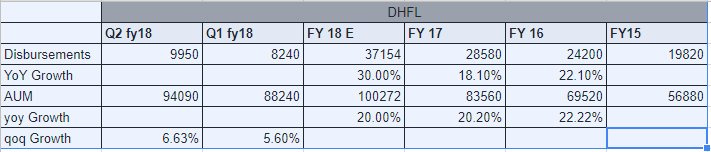

DHFL - higher than average growth in disbursements needed (+30%) to sustain the same AUM growth as past 2 years (+20%)

#Q2 #headwinds

Has somebody done Financial modelling for DHFL? Would be of great help if you could assist me with the file and calculations.

Thanks!

Housing Finance - Ambit view

http://reports.ambitcapital.com/reports/Ambit_BFSI_HFCsHoldersbeware_23Jun2017.pdf