I also did not get why DSP MF liqudate DHFL bond only… why not the other company’s bond ? There is something fishy…Is it true that RBI proposes new Real Estate credit policy for HFCs as they had an observation that few HFCs are touting LAP as housing loans and DHFL and IBHFL are alleged to be major players in this allegation?

1 Like

They have clearly mentioned in their interviews that it was not just DHFL paper that they were selling but they have reduced exposure to multiple issuers over the last few months.

2 Likes

Who are those? Any idea?

No matter what experts or Promoter says, 45 % fall in a single and not much recovery, doesn’t sounds good. As there is no smoke without fire. There is some bad news apart from DSP selling bonds which we dont know yet. I think it will come out in next couple of days.

Disclaimer- Invested from 3 years.

It looks risky. But based on the information we have at hand, risk reward ratio is favorable. AAA rated, fourth biggest housing finance company with experienced management over liquidity cycles having Excellent NPA figures at 8PE is a bargain. Less than 5 percent exposure would not hurt.

2 Likes

DSP selling small chunks of bond to manage duration/maturity of their bond portfolio is an everyday job and should not cause any alarm. What is concerning is that a AAA rated bond yield rises to 11% in the secondary market so what will happen to lower rated bonds? How deep is the liquidity issues in the market? where are bond yields headed? These questions will be answered in hindsight but risks need to be reduced now. I think RBI needs to intervene and provide liquidity to calm the debt markets.

2 Likes

When the event is big, we as investors start fretting and looking for answers in the minutest details.

Dhfl has had governance issues in the past and hence was valued attractively. Mr. Jhunjhunwala decided to invest based on conviction in the future and is/was sitting on a good profit.

In simple words, DHFL just raised a huge chunk of money recently. How can they default in their payments in the near term? I am not saying their financial health is or will be good, but definitely no issues in near term.

Since Il&fs issue, investors of all strata are nervous about fianance companies, hence a small selloff must’ve sparked heavy selling which spiralled out of control. Dhfl stock price increased in the last year and hence short term covering happened in panic.

Why a stock was allowed to fall 60pct in a day by SEBI is surprising though. Also, if DHFL is buying PNB housing their compliance issues need to be zero. Additionally, Deloitte as auditors gives me peace of mind.

This is my opionion but truth can be different.

Disc: invested.

Wanted to share some rough numbers:

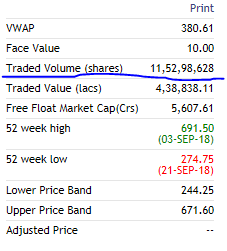

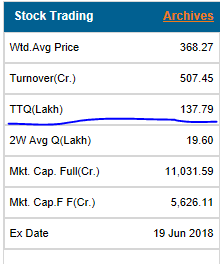

If I look at the number of DHFL shares that were traded in the cash markets yesterday, those were around 11.5crs in NSE & 1.4crs in BSE, total around 13 crs roughly.

Now DHFL has around 31 crs of paid up equity shares. Of this, roughly 40% is held by promoters, 30% by public, and 20% & 10% by FIIs & DIIs respectively. These are approximate numbers.

If 13crs shares were traded out of 31crs, that is roughly 42% shares. If I take out 40% shares held by promoters, roughly 70% of the free float.

If the institutions, DII+FII combined cashed out their entire holding of 30%, even then there would be a 12% shortfall which public had to trade. This seems extremely unrealistic.

It is quite likely that my numbers are wrong, which is why request experts to comment.

Disclosure: investor in DHFL - trying to make sense of what happened yesterday.

NSE numbers:

BSE numbers:

1 Like

Usually the more the management tries to convince shareholders that everything is alright, the more worried they get

This is true in life as well, if you have not done anything wrong, you just say yes or no for instance if some asks were you working late in office, you’d say yes

If you are lying you’d say yes and try to explain why you were late

Traders have a sharp sense of these things so I think in all probability the explanation will do opposite of what is intended

Good management response would be “stock is cheap and we are buying our own stock…as much as we possibly can”

I might be completely off a different tangent here

3 Likes

I’m not going try and advice the management on what they need to do, but using excess cash is not as prudent for a highly leveraged firm as it is for others. The additional cash is part of the business and is required to protect the firm from adverse credit events. In fact, you only need to look at the history of buybacks in India and see how many BFSI firms bought back their stocks in relation to the others. I’m willing to bet that it’s a minuscule amount.

The crash was definitely a surprise for all of us, including the CMD himself. However, it’s moments like these when there are very polar mindsets. The management will get bombarded with acquisitions regardless of whether they provide an explanation or not.

With the information we have in hand, it doesn’t look like anything more than a knee-jerk reaction. We do know that tight interest rate are about to follow, courtesy of the RBI, but speculating that there are skeletons hidden in the closet doesn’t sit well with me. The management did not seem hesitant at all to answer any question in the call and so, there’s room for trust.

We can add value to this discussion only if more factual news emerges.

4 Likes

All companies that lend money are leveraged and have to be leveraged, not just in India

Their efficiency is not measured by debt/equity ratio

I am not telling management what to do, I am only saying what would be ideal thing that would allay investors fears besides no management is capable of always taking investor friendly or company friendly decisions, this you should know except if you are too naive

During 2013 when interest rates went up, the Pe of dewan went down to below 5

The Pe is at 8 now and as interest rate works it’s ways through to weighted cost of capital and inturn to dcf/npv calculations, higher interest rates will bring down valuations of most of the companies not just Dewan

Dewan probably reached there first but Its anybody’s guess if coming out back to higher P/E ratios very soon

Mortal blow to DHFLs ambitions to acquire PNB housing finance. Existing shareholders will be affected if DHFL pays premium and issue equity to acquire PNB housing, since Dhfl is selling at a significant discount. Also it doesn’t make sense to acquire a competitor, unless the intention is to get the help of the top class management of PNB housing to run your own business.

I can understand Godrej, Blackstone or Bandhan bank bidding for PNB housing as they don’t have exposure or build infrastructure in this segment

Why would Dewan want to ?

Shows management is only focused on building a big company so they can take bigger salaries as fast as possible without regard to asset quality or increasing individual shareholder value.

Mortgage business is a commodity business. Instead of buying a company at premium just reduce interest rates to cheapest and people will switch. Oh yeah I forgot, that will show a loss on the p&l whereas buying out will hide that loss in the balance sheet as goodwill or something and come out in the p&l as one off

Maybe they can concentrate first on increasing their efficiency

Profit / ( [opening loan+closing loan]/2) is worst among peer group

1 Like

Yes lot of people are saying companies should not keep on giving clarifications because then doubt increases…

But 50-60% fall is not a small fall and this needs clarifications because then whole sector is being targeted…

Following a series of clarifications… SBI also clarifies about the situation… Now I am just waiting for RBI press release… On Monday they will too … because otherwise it can lead to panic in debt market…

SBI will continue to lend to NBFCs, no liquidity concerns: Chairman on cash crunch rumours

This statement comes after reports emerged that banks are restricting their lending to NBFCs, especially mortgage financiers, and on construction-related priority sector loans

1 Like

N number of people will have N number of perceptions.

The big fall of friday surely warrants management clarification, if they dont do it they might be labelled as not being sensitive enough to minority shareholders interests.

I see it this way - what has happened on Friday that made the buisness lose 45% of its value ?

NOTHING !

we all can arrive at different valuations, but that wouldnt justify 45% correction in 1 day, isnt it ?

if one is to go with the “Market is right” philosophy, market cannot be right on thursday to value a company at 600+ per share and then the same company at 300+ per share just the next day.

its is very human to panic when the market has -ve undertones and a bearish sentiment, i am quite sure the same fall wouldn’t have happened on the same news last year.

3 Likes

Based on all hard facts as of today, DHFL has a very comfortable liquidity level.

2 Likes

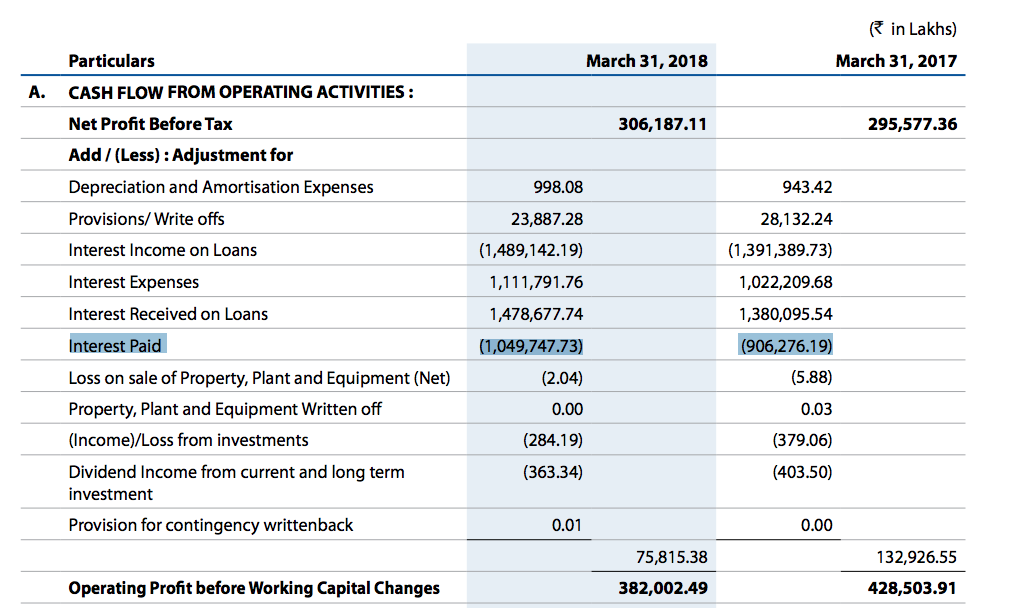

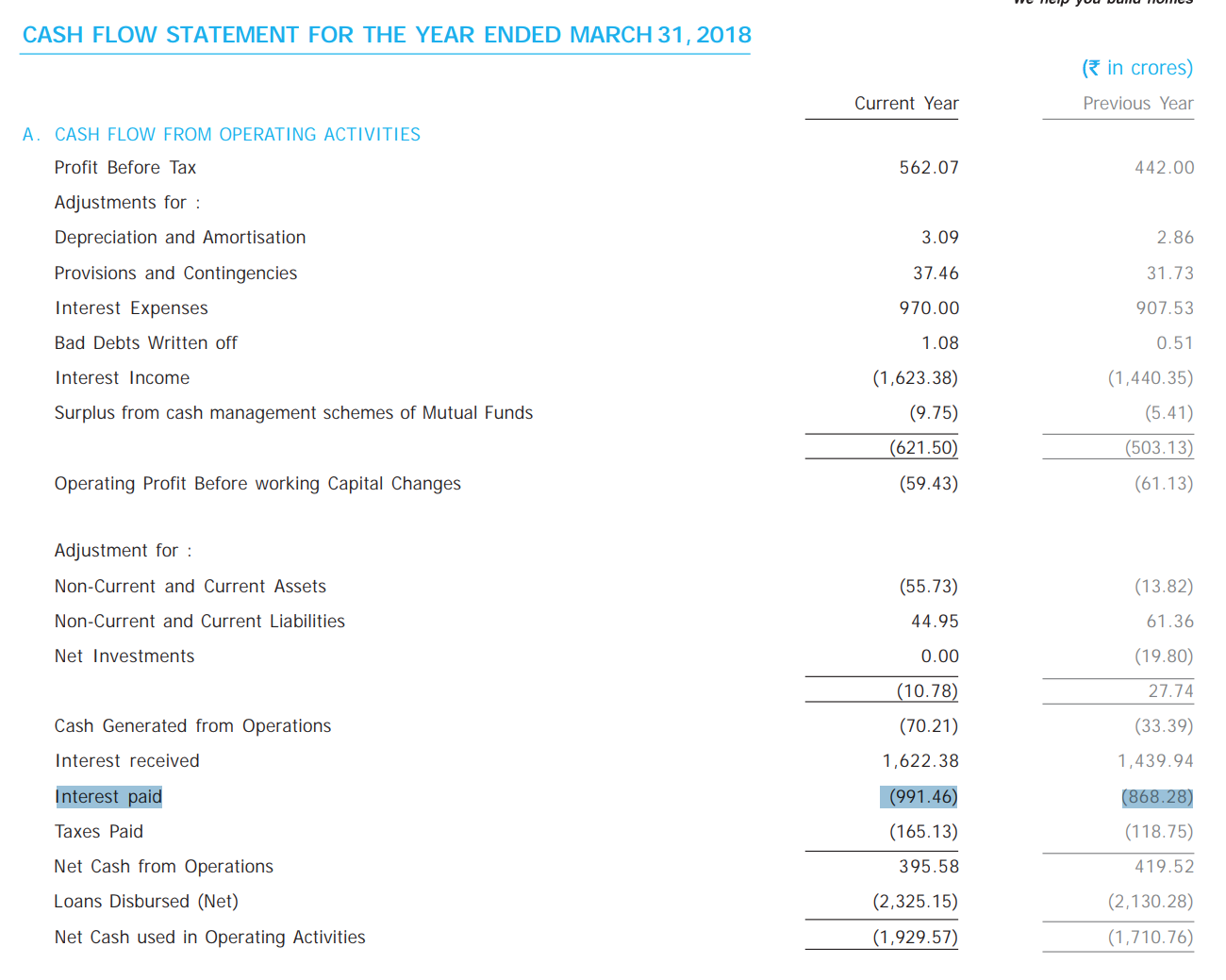

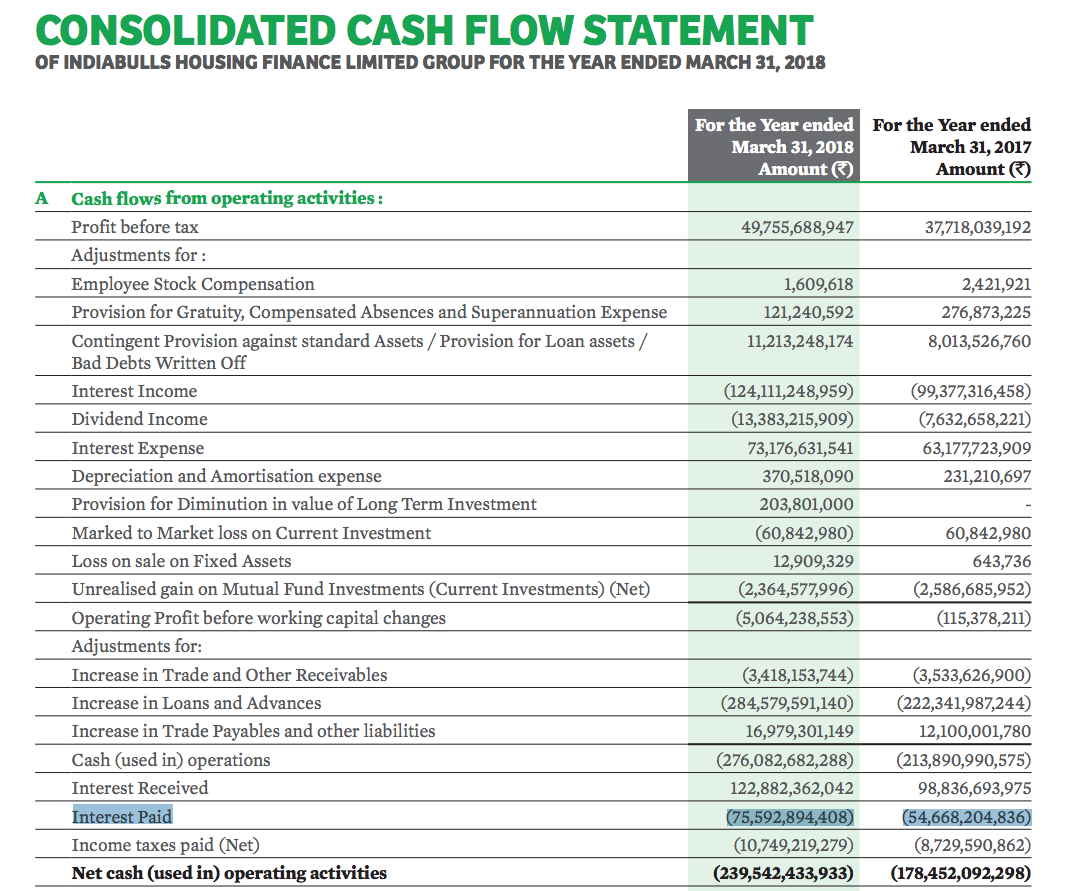

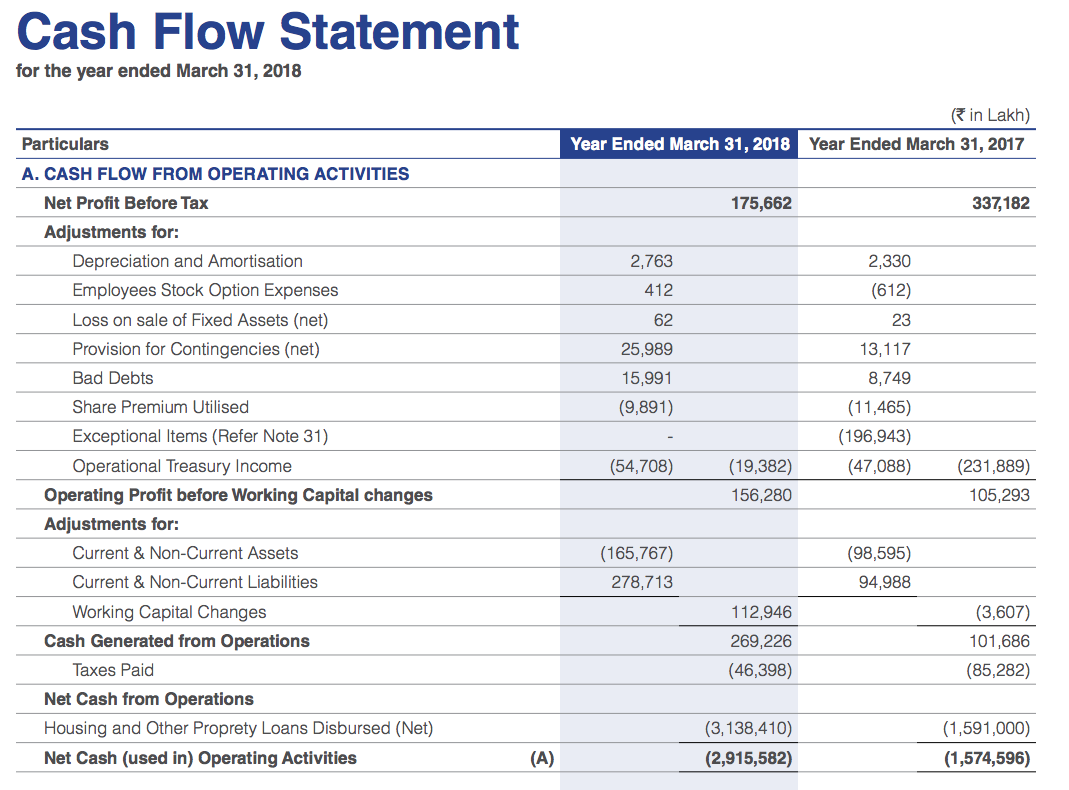

Here’s another curious thing, noticed in conversation with @anni23

CFO shows Interest Paid and Interest Received clearly for Indiabulls, LIC and Gruh

LIC HF

Gruh

Indiabulls

But for DHFL and PNB Housing, this is how it looks. There is no line-item showing the Interest Paid and nothing to show the Interest Income received.

DHFL

PNB HF

Interestingly, PNB Housing’s cost of funds are a little all over the place (based on the PnL). Maybe this is something normal but interesting nevertheless, that a few companies in the sector do things in a certain way that provides more transparency while two of them don’t. The Interest Paid line item in the cashflow for Indiabulls, Gruh and LIC closely match the number in PnL while there is no way of verifying the same for the other two.

2 Likes