Where did u get this info …Unable to find on bse

I got it through an investor friend (That is why I wasn’t sure if it was correct or not). But in the interest of time, I posted it anyway.

I tried dialing in now, but the conference is full. We should get some factual updates once the call gets over.

1 Like

Today is like watching an edge of the seat action movie!

1 Like

Here’s an audio of the call that I recorded (I joined about 10 minutes late): https://instaud.io/2HTi

Major questions answered:

- The sale by DSP was a secondary market sale (DSP itself clarified that the sale was not due to DHFL’s quality as a lender). DHFL itself was recently able to make a private debt sale at 8-9% (Close to a AAA Rated bond). However, they said that they will not be willing to raise further debt at a 11% level, if it came down to it.

- No ALM mismatch. The company has enough liquidity to pay off all their debts.

- (This was in response to my question at 24:25 about RBI hinting at rising interest rates) DHFL has already risen interest rates on their books by 62 bps since April 2018. Changing interest rates are a regular business activity. Also, 99.70% of their Loan Book is on a floating rate basis.

- The government itself is promoting housing for all, attracting massive money to the sector. So tail events are bound to happen (I thought the CEO was quite honest with this question)

- Something about reporting requirements being different, so there could be a mismatch of the debt numbers they were stating in the call and the ones of their previous AR. Didn’t quite listen to this.

- The company has bid for PNB Housing in the ongoing stake sale by PNB.

- The company cannot be held liable for the market reacting this way. They kept referring to this as a one or two day event.

- Someone indirectly asked if the NPA numbers were correct or not and what the management thought about regulatory scrutiny. The management didn’t want to comment about regulatory moves, but said they’re fully compliant and would have no problem facing increased regulatory requirements. Proxy Gross NPAs (Stage 3 loans) are at around 0.93%.

- The company has 35+ years of legacy and with the owners’ good wishes, they will continue to perform well.

Finally, there’s a call for Debt holders going on from 4-5 PM, post which there could possibly be a repeat call for Equity holders at 5-5.15 PM, the details of which may be shared soon (CEO requested the Investor Relations head to schedule another call, because he couldn’t answer all the questions in this one).

I hope I paraphrased all the important points.

17 Likes

Thanks Dinesh

I think its knee jerk reaction to a market rumour

Press release

Personally for me, it’s more a lesson that one should hold at least 15-20% of cash at all times in order to capture black swan events like this. During the mid cap crisis a few months back, I drew a chunk my salary forward and invested most of it, along with whatever savings I had at the time.

Regarding the call, I have to say that the management sounded quite honest. They did not hesitate to answer any question and no answer seemed forced (I especially liked the CMD’s answer about government propaganda creating tail events - if that is not honest, I don’t know what is). I am not sure what risk the markets saw in the company. I could perhaps understand a 10-15% drop on fears on interest rate hike, but a 40% fall is in my opinion, unwarranted (In fact, in intraday, it touched a 60% level and then bounced back). If I had cash handy, I might have even invested all of it today.

8 Likes

Seems like DSP is out of DHFL. DSP Chairman says, its unfortunate that their transaction triggered the crack.

The reason for their sell off doesn’t sound convincing.

3 Likes

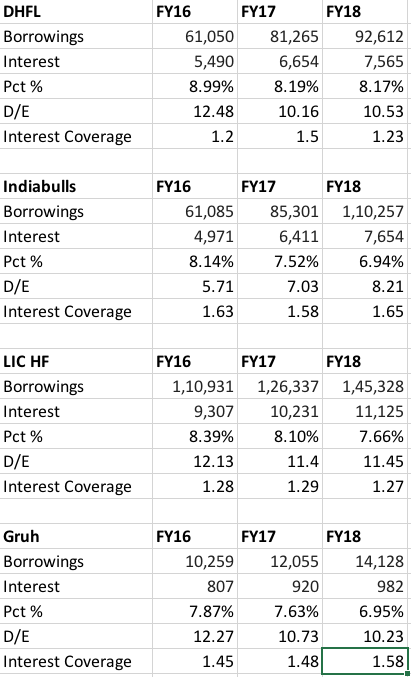

I don’t think this kind of price-action is normal. I think there is definitely some problem, either immediate or impending. I did some basic analysis of housing finance companies - solely from a capital structure standpoint and this is what it looks like.

These are my observations

-

What strikes me immediately is the interest coverage ratio of DHFL vs other players. Between FY17 and FY18, the interest coverage ratio has deteriorated more for DHFL vs others. This I think is because the interest cost for DHFL is higher than others. While all other players had a 50-60 bps reduction in interest outgo between FY17 and FY18 due to the rate cycle, DHFL’s outgo reduced only by 2 bps!

Now in an increasing rate cycle, the interest coverage ratio is bound to deteriorate much further for DHFL vs others. -

A HFC benefits when rate cycle is headed down and sales is increasing and interest coverage is improving. The same thing reverses when rate cycle is up where sales starts decreasing and cost of funds start increasing - The weakest in the ecosystem could get taken out first. I think this is what is spooking the market (or at least one of it) - The chances of reporting a loss in the coming quarters is high for DHFL vs others, because of their deteriorating interest coverage ratio and higher cost of funds.

-

It looks like a bulk of the company’s liquid funds is in Mutual Funds - of the 10k Cr the company says it holds, 8000 Cr is in mutual funds - this amount is as of Mar 2018. I think it is only fair to assume this should be marked down by a 10-15% because of the markets being down from then (Assuming equity funds) and a further redemption of this huge amount is going to come at a further discount to notional value - probably much less than 6000 Cr.

-

When I was invested in this company sometime last year and kept wondering why it was cheap compared to other players, I found that it was because of its relationship with HDIL and this was a corp governance discount. I never quite understood this then being new to the markets but now maybe I do. There were also claims of the company capitalising interest costs - If this were true, then the actual interest coverage ratio is probably much worse than my calculation. I don’t know this for certain though.

-

Then there is the case of actual NPAs on the company’s books. Its always easy to hide these when sales are increasing and interest rates are down. These cockroaches come out only when the economy is deleveraging. This could have a very adverse impact if the NPAs are higher than reported considering the company’s D/E. The company lends to a segment which could possibly have higher NPAs as well (LIG).

So to sum up, there does seem to be a genuine reasons for the slump. All it takes is one big player to try and exit when no one else wants to buy.

Disc: No holdings but held for sometime last year

10 Likes

Not sure where you got these numbers from. If I remember correctly, DHFL had an interest cover of around 1.19-1.23 for the past five years. I don’t remember it ever having a cover of 1.5.

Yes, that was the question I asked. The CMD answered that they have already passed on 62 bps to their customers. I’m not sure how much RBI plans to raise the rates, but they are definitely doing a lot of OMO purchases. Rest assured, whatever impact on the bottom line, would be reduced to the extent of the company’s swiftness in passing on the difference. 99.70% of their Loan Book is on a floating rate basis, making it quite easy to do this.

This would be a fair enough assumption if they had a lot of exposure to equities. But most of their exposure is indeed to debt funds, arbitrage funds and other short term funds (And yes, some exposure to equities). I really doubt such a wide mark-down is warranted.

The company has capitalized interest costs on unfinished PP&E and Leases. This is fair accounting practice (Someone well-versed in accounting, do correct me if I’m wrong). I didn’t find any other interest payments being capitalized. Once again, this wouldn’t affect the interest coverage ratio, since the assets/leases responsible for creating profits have not been recognized yet (At least to the extent the interest is capitalized).

At this point, with the information we have, this is speculation. Once again, a direct question was asked in the concall about NPAs and regulatory pressure, to which the CMD responded in the positive. Unless some proof about cooking the books appears, we should refrain from making allegations.

Disclosure: I hold DHFL in my portfolio. Views may obviously be biased.

3 Likes

For the first point of low interest coverage ratio - I think your calculations include extraordinary gain on sale of insurance which is why profit for FY17 is high and which is why interest coverage range is higher - range is around 1.2-1.25 for all 3 years I think. In fact they got a huge burst of liquidity on sale of Insurance business

For point 4 when the company says liquidity is in mutual funds - I believe it includes liquid funds of mutual funds. I could not find much investment in Equity funds in their latest annual report

For point number 2, why do you say they will report loss?

More or less agree with 2 other points

Discl: Hold some DHFL (<2%)

The formula used to calculate rate of interest is not accurate

You have used interest expense for the year / loan balance at the end of the year

It should be average loan balance by taking the opening balance and closing balance and dividing by 2

First disclosure that I do not hold DHFL or any housing finance company. Along with this number crunching, I think other point to consider is the perception of the market. As an example, Dilip Buildcon (which I hold) fell few months back due to some rumor. Management did multiple analyst meet and clarifications that there is nothing wrong. In fact, No one has been able to find anything significant wrong yet in it but price which fell from 1200+ to 800 has still not recovered. All I am trying to say is that do not ignore this Qualitative part. See Gruh Finance… how it recovered and ended positive. Perception of the management quality probably will play bigger role and numbers might become secondary till confidence is restored which can take time

3 Likes

Usually the more management tries to allay fears the more it ends up adding fuel to fire

While this was a huge drop and probably merited management statement but a good class management would not intervene in the market and probably use this opportunity to buy back shares from the market at half the price it was trading at knowing fully well there is a lot of value in their business

2 Likes

Toshniwal Equity sent out almost identical info minutes after your post here.

Regards,

Suhag

2 Likes

Thank you for posting this. All of the analysis that has ‘suddenly’ sprung up here has been solely because of the price crash, and the assumption that the market is efficient and therefore the price movement is telling us something. Without this drop, this analysis would likely not exist. Paradoxically this is the same assumption value investors (like us) assume does not hold when we buy $1 for 50c.

I’m not sure what to make about this news. Assuming all is good, I am very worried about the fragility of Indian equity markets if a sell-off by a ‘small’ mutual fund can trigger such loss of wealth. The level of homogeneity in the finance sector this implies is terrifying, since there were/are no buyers to match this selling volume. Further, could DSP not have anticipated this and saved themselves the losses by doing off-market transactions? What would happen if a blue chip company was next? How far would the contagion spread?

9 Likes

I agree with Sushil’s opinion. In an event like this everything adds up. There have been perceptions about management quality for so long. It will be hard to point at very obvious root cause because none of the above warrants 40 percent downfall. Either we don’t know something or today’s event is discounting of all the perceptions related to management integrity around a rumour.

Imagine if this was hdfc bank. No one would have believed the rumour. Because it is dhfl investors/trader say “ I can’t rule this out” . What is my safest option?

“Run !!!”.

Where do you spread rumour? Where you know it will be believed by fellow investors. It won’t be believed in Piramal or hdfc.

Investors sell, not only because news/rumour warrants selling, but also sell because you feel others will sell based on this news/ rumour , hence price will be lower for foreseeable future.

I feel it also has connection with yes bank ceo not being extended and stock cracking 30 percent. It tells investors if you can’t trust promotors then it will take one day to wipe out all gains. Also I was wondering why no one was speculating that rbi can say the same for Kapil.

Now we have seen couple of these cases. Below stocks may not be exactly same but similar in nature due to one day heartbreak.

-

Vakrangee ( 90% wealth lost since January, price is still not back. Next two quarter profits( March and June) were also significantly lower) so it still makes sense.

-

Pc jeweller (584 in January and 71 today, profits for March and June quarter were inline and not down much) share is not back up still.

3 Dilip Buildcon ( explained by Sushil in last post)

4: KPIT (this is 3 years old)

- KRBL(. 533 in May and 361 now, profits were in line for next quarter not significantly down) share is not back up still.

We should do deep dive in above stocks to understand specific nature.

In KPIT, I received a message that promotors are planning to sell the company and this is another Satyam in making. I was wondering where did I get this message from as I have no messaging service, not subscribed to any groups.

Within next 3 months stock came back to original price. In KPIT there was no previous management integrity question or issue.

When there is a panic, everyone wants to run in same direction downwards at any price at same time. But in upward journey trust building takes time, one step at a time , one person at a time.

I assumed bringing Deloitte as joint audit partner would have removed investors concerns on numbers. Apparently not.

Looking forward: if DHFL reports reasonable strong earnings next two quarters.

If you still ask the question “ can I trust the numbers?” Anything else doesn’t matter.

Trust building will again take some time.

Few thoughts:

- TTM yearly profit is 1347 crore. Today’ s market cap is 11000 cr. How much you value the uncertainty?. It is 1.2 times book. Will the profit number start reducing by 40% by next quarter ?

2.Does today’s issue cause housing loan demand slowdown for dhfl?

3.As per management promise they have enough liquidity to carry till at-least till March 2019. Do you trust them? Your call based on your market experience.

4.For money supply perspective, will it be constraint?- Is money supply at a higher interest also a constraint? or money supply at lower interest rate a constraint?

5.This is an interest pass through business. All banks, nbfc’s pass the interest rise to consumers. Even if there will be a margin pressure for short term that will be shown in number and you give less valuation for that .

-

The risk of unknown will be there for near future. In times of volatility investors will always say “ why should I take the risk? ”.

-

Rakesh Jhunjhunwala has a good stake. It would be interesting to see his take. If he wants to he can build confidence for dhfl promotors. Will he? Don’t know.

8 What happens when dhfl will post reasonable numbers and we don’t have any concrete evidence of wrong doing and default. At what point we say, it was nothing just only a rumour . 6 months from now? 1 year from now? It will help us take a decision then if the stock is still undervalued.

I am still making my mind but thank you for sharing concall details and other facts which helps us analyse.

This is a great learning opportunity.

Puneet.

10 Likes

The only difference between the stocks you mentions and Dewan is that Dewan went to -60pc and recovered 20pc right away to end up with -40pc

I think most of the stocks you mentioned never recovered some of the lost ground

Disc: No holding here.

I don’t think this fall is ordinary by any means and keep in mind that it did not make decent recovery despite management call. Are we saying that such large sellers fool enough to panic like that?

I have heard strong rumours that RBI will focus its lens on abuse of LAP loans and related NPAs and that’s why HFCs were particularly punished. We need to keep in mind that HFCs had corrected already so it can’t be valuation. There are also rumours of collusion between RE developers and HFCs to keep ever greening of loans. These might not materialize but the way Yes Bank has been treated anything could happen. Keep in mind that IL&FS loans were AA rated few months back and became DD suddenly so regulator is in overdrive to take out all weak spots in the financial system. Market perception of DHFL has never been great so punishment was coming. One thing is certain that this is not technical sell off and rest will be known later.

2 Likes

This contains most of the things that’s been attributed to the crack today. But this article puts in neatly with a bow:

3 Likes