Yes, that is correct. These projects will only generate ROCE of more than 12% only if IPA prices prevail over 120-130 per litre on sustainable basis which looks highly unlikely as Deepak Fertilizers do not have control over the prices of IPA. Similar is the case of Ammonia.

Dear Raj,

Thanks for sharing your input here. However, I see that you have invested in this company. Could you please share the positive you see in this company for investing in Deepak Fertilizers? Is it because you are expecting a possible TAN import ban will have a positive effect?

Thanks in advance,

Anto

Hi Anto, my rationale for investing in Deepak Fertilizers was the surge in the IPA prices and the stabilization of the crop nutrition business. Also, you rightly pointed out that the ban in TAN could be have a positive impact on the company coupled with privatization of coal mining in India.

Tomorrow there is a board meeting to decide the rights price and the entitlement ratio. My reckoning is that the rights price would be around 20 percent discount to current market price and entitlement ratio would be 15:100 (this is an assumption, so there could be 5 to 10 percent deviation)

Having said so, there are a few red flags in the company with promoter always focused on Capex due to which there has been misallocation of capital. Also, according to me the board of directors are rubber stamp and not independent in the truest sense.

2 Likes

Rights price at 133 with share entitlement ratio of 15 shares of every 100 shares held.

Hi,

Dates regarding the rights,

Last Date for credit of Rights Entitlements - Friday, September 25, 2020

Issue Opening Date Monday - September 28, 2020

Last date for On Market Renunciation - Wednesday, October 7, 2020

Issue Closing Date - Monday, October 12, 2020

Finalization of Basis of Allotment (on or about) - Wednesday, October 21, 2020

Date of Allotment (on or about) - Wednesday, October 21, 2020

Date of credit (on or about) - Friday, October 23, 2020

Date of listing (on or about) - Monday, October 26, 2020

I have a question about the dates. Are these tradeable like the reliance rights issue? If yes, they will be tradable during the period Sep 25 to Oct 7 only?

I see that the Reliance RE is still available for buy/sell in the market. Is this because Reliance is a very big company?

Thanks in advance,

Anto

Can any body throw light on the current pricing for IPA as the Q1 margins were mainly driven by IPA???

Current IPA prices hover in the range of 85 to 90 rupees per litre. Yes the Q1 margins were largely driven by IPA and the IPA realisation for Q1 was in the range of 120 rupees per litre.

Q2 realisation should be in the range of 100-105.

Also, if the prices fall below 65 rupees per litre, it will turn EBIT negative for IPA segment.

1 Like

Statutory Auditors have resigned citing fees relates issues. The reason attributed seems to be flimsy when the Company is making decent profits.

4 Likes

The same auditor has resigned from one more company IVP Ltd citing similar reason.

3 Likes

Off late, BSR has been resigning from companies citing fee related issues. Asking for fee hike during a pandemic is anyways draconian, or could be a natural way of churn to free up resources for something else. Shouldn’t have material impact of any sort. Nila, Sasken, IVP, Repro are some of the examples btw.

This is my theory. What may have spooked the market on the result day is the resignation of the recently appointed Non executive Director Mrs Renu Challu, resignation of the Auditor and retirement of their CS - all happening at the same time.

Retirement of the CS seems natural - the guy seems 60+ years old as per his professional timeline on LinkedIn. Renu Challu was new and wouldn’t wanna get into trouble since Auditor’s resignation is generally perceived as terminal.

2 Likes

As per Concal, IPA price had fallen to pre COVID levels and from there it has has improved. We should remember that IPA business in pre Covid Quarter was loss making due to cheap imports from China. The main reason for impact in IPA buisness is because of manufacturing of IPA from Acetone route as against from Propylene(Deepak Fertilsers existing process). Can any body in the forum give some analysis on the Cost of Production of IPA from these two different routes i.e Propylene Vs Acetone.

Also can anyone provide analysis of CAPEX expenditure required on IPA from Acetone route Vs IPA route…Deepak Nitrite is having surplus Acetone which can be diverted to IPA. Apart from this the global slowdown in Phenol prices was an indication that excess Acetone will be utilised for IPA becasue of which the IPA prices was depressed during Pre COVID.

In my opinion IPA euphoria is now over as sanitization is not going to press the accelerator for IPA prices.

Disclosure : Invested less then 2% for Tracking position.

Did some fundamental research on Deepak Fertilizers and putting my thoughts here.

My first impressions on the business at a surface level

- This is a fertilizer business - has fertilizer in the name and has a fertilizer business P/E (reinforcing cause/effect cycle)

- Numbers look good (which is why I was looking at it any way) - but they are the largest manufacturer of IPA - So Covid should be driving the numbers and so they must be one-off

With this first impression, I set out to understand the business.

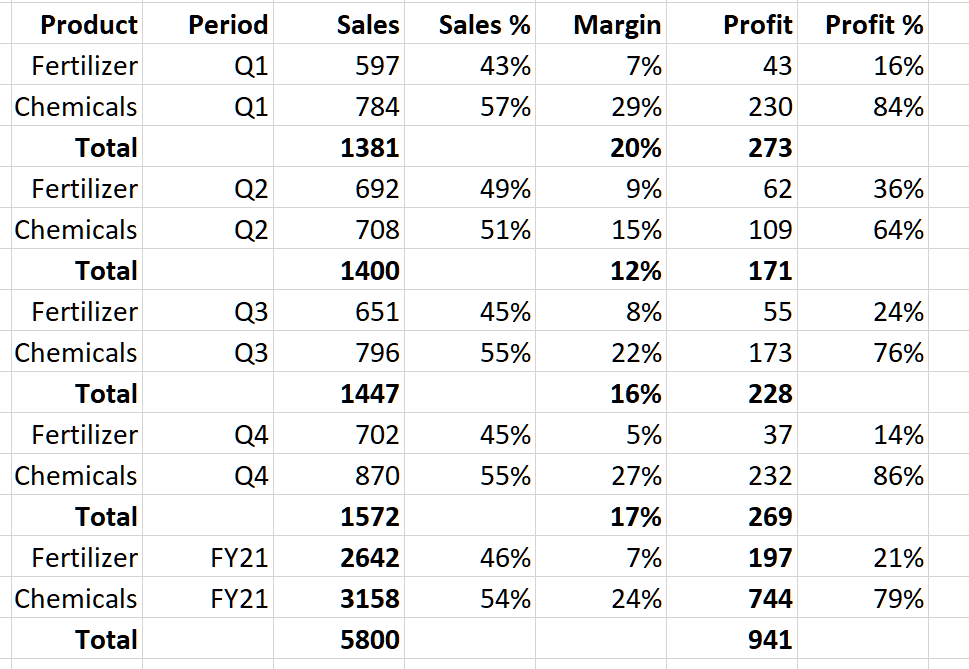

These are the numbers I pulled up from the last 4 Investor Presentations in FY21.

Looking at these, few things stand out

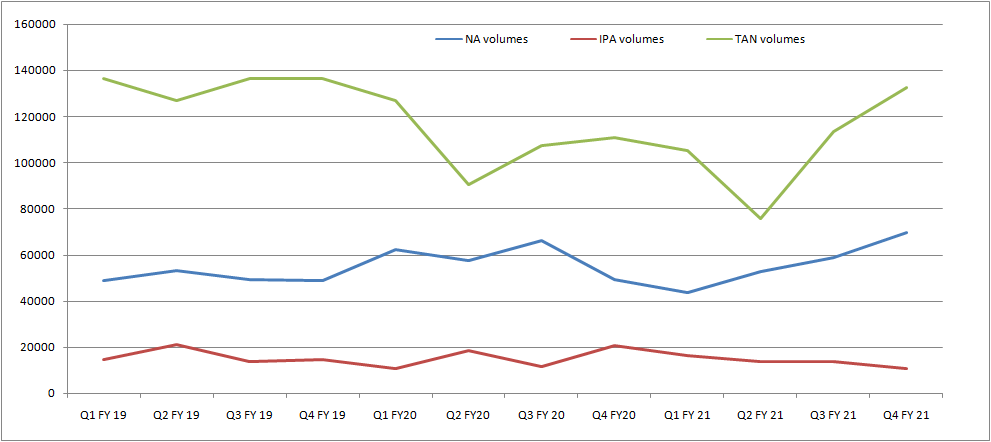

- Though Fertilizer business contributes a lot to the topline, its contribution to the bottomline is much lesser. Chemical business contributes 80% of the profits.

- Chemicals margins are at a respectable 24% for FY21. This appears to be continuously improving on account of increase in TAN contribution when compared to FY19 and FY20 - There is almost 30% increase in volume of TAN and consequently the margin profile has continuously improved

But what about IPA? Is it contributing disproportionately to the profits in FY21?

IPA sales as per my calculations by looking at the 4 investor presentations works out to about 550 Cr. That’s about 9% contribution to the topline (18% to Chemicals). They are likely to have made about 150 Cr profit from IPA sales. So the more than doubling of operating profit from 450 Cr to 950 Cr - 500 Cr odd increase, had a contribution of about 150 Cr from IPA which may reduce by about 50 Cr when Covid demand reduces. But the rest of the increase of about 350 odd Cr could be the sustainable increase due to operating leverage in the TAN (Technical Ammonium Nitrate) and CNA (Nitric Acid) business. Again, lot of guesstimating - so please verify on your own.

The improvement in product mix by reducing of low-margin trading products is also visible in the working capital management.

There is also a big improvement in OCF which has helped in reducing debt from 3000 Cr to about 2300 Cr. The net D/E of the business improves as a consequence from 1.2x to 0.65x

While researching I discovered that they have major market share in these. #1 in India in all and 2nd largest manufacturer of Nitric Acid in SE Asia

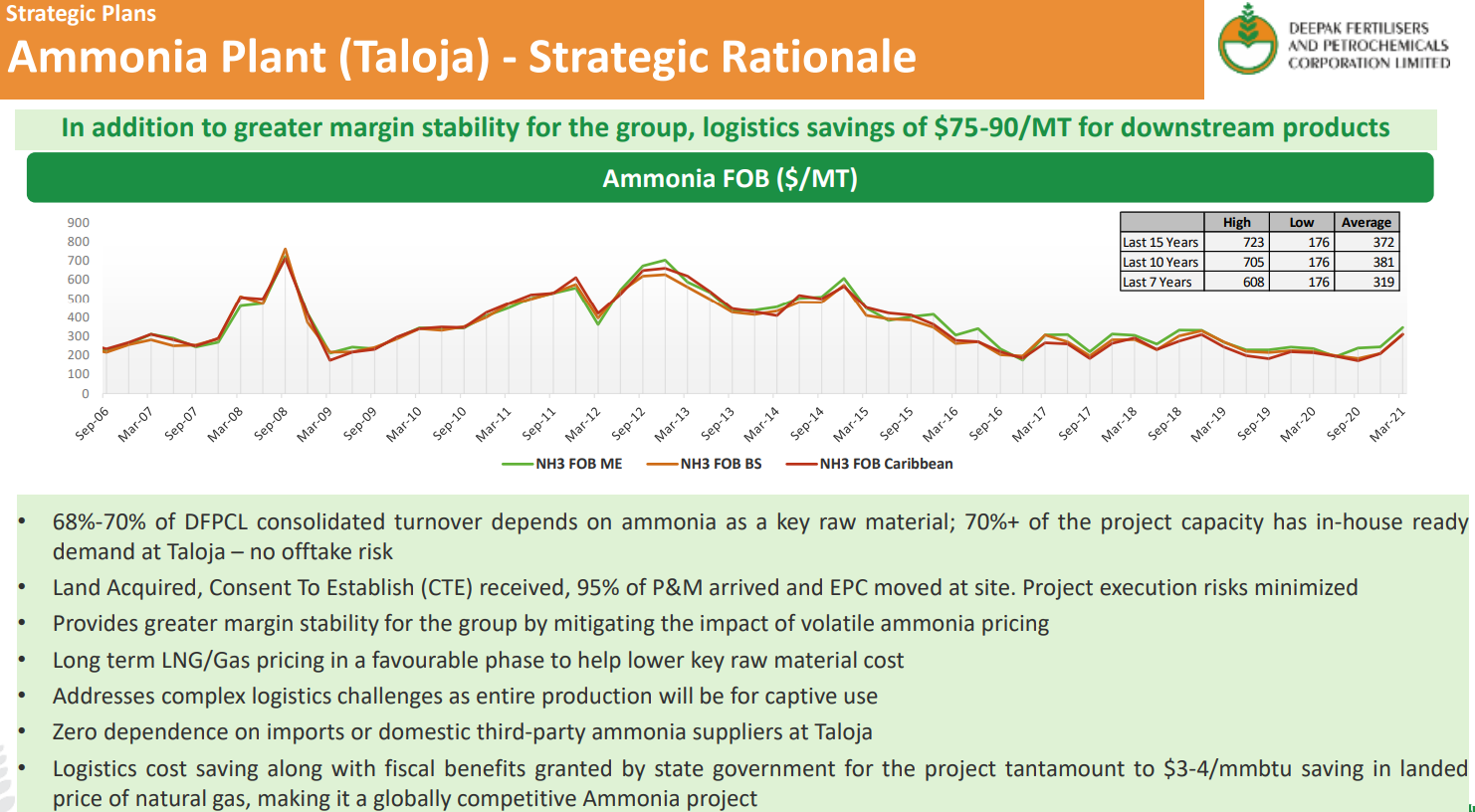

There is another interesting thing happening with the business as well. They have embarked on a mammoth Capex, maybe even more ambitious than what Deepak Nitrite did with Phenol.

Ammonia is a key starting raw material for end products that are used in a lot of sectors from mining, paints, fertilizers, dyes, construction etc. This is China-level capex. We haven’t been this ambitious in terms of building capacities so it is nice to see it happening, especially for essential raw materials.

Investment Thesis

-

Scope for re-rating from the current 7 P/E and 1x sales (Chemical business alone has a sales of 3200 Cr and market cap is 3000 Cr) to something better - Deepak Nitrite for example is currently trading at 5x Sales. Not even including the fertilizer business here.

-

Operating leverage could play out going by the current capacity utilization

-

When Ammonia plant capex comes online, the transformation of the business could be very similar to what Deepak Nitrite did with Phenol

Phenol Imports (FY21 only ppto Feb '21) - Notice the big drop in imports in FY20 and FY21 - Completely substituted by Deepak Nitrite

Ammonia Imports (FY21 only ppto Feb '21)

This is even bigger in terms of opportunity size than Phenol. Also the per kg realization of Ammonia conveys another important thing - At Rs.25/kg - this is cheap by weight which means it will be harder to compete for imports (Same logic as applies in cement at Rs.5/kg or Phenol at Rs.70/kg). Bulk of the cost would be logistics cost in these low realization products.

For domestic businesses as well, there is a lot of working capital stuck in transport which too could be reduced.

On the topic of comparison with Deepak Nitrite, the margins of DN improved from 10% → 12% → 16% → 24% → 29% and with it the stock has returned about 10x.

Deepak Fertilizer is now at 10% → 16%. So next 3 years will tell us how it actually plays out. At current starting valuations, we are probably not overpaying and the trajectory is an optionality at these valuations.

- Last couple of quarters, the management is talking about chemical value chains moving from China. So this could be a China+1 play and import substitution play

Risks:

- Large capex doesn’t always pay off and doesn’t always pay off soon. Plant coming online could be delayed. Total capex for Ammonia plant is over 4000 Cr!

- While OCF is improving dramatically, the business has to continue taking more debt to finish this ambitious capex. While this would have been frowned upon and seen as highly risky, in current low interest rate environment, if the business can generate good returns over the risk-free rate, it could in fact work out as a positive (World is flush with cash with less avenues for profitable investment)

- About 77% of promoter shareholding is pledged

References

Investor presentations Q1, Q2, Q3, Q4

Disc: I have positions from 220-290. Am a novice and could have made several errors. Please do your own due diligence.

Update: Looks like the pledge is not really a pledge to borrow. It is a non-disposable undertaking (NDU) provided by the promoter to IFC for CCDs issued to a subsidiary. Company clarification here.

64 Likes

1 Like

deepak fertlizer some notes from q4 concall:

they have deferred the TAN expansion and are focussing on the ammonia project to get it operational by sep’2023.

1500cr has been spent in f21 (already part of the financials) and 13-1400cr each is to be spent in f22 and f23.

debt has reduced from 2665cr to 1800cr in f21 which includes fccb/ccd of ifc (about 400-450cr) which will get converted to equity in next 6-7 years. why this is important is because the additional 2800cr ammonia investment will require debt, which they had indicated will be additional 800cr (but this figure could change, because it looks low). annual repayment of existing debt is 250cr. but it looks like overall debt levels would be comfortably manageable including the leverage ratios. ofcourse, provided product pricing environment remains healthy.

new ammonia capacity is 5L tpa and about 150-200 usd per ton is expected savings at ebidta level, ie 500-600cr (ideally).

the concall indicated that q4 and f21 growth was contributed by volume increase also and not just increase in realisations. plus they have capacities available to increase volumes this year. and because they did large expansions in 2017 and 2019, further debottlenecking possibilities are there with less capex.

eg. fertilizer capacity of 6L is 70-75% utilised and can be increased closer to 90-95%. they are also planning debottlenecking to increase capacity to 8L. their processing plant already has this capacity. they need to increase their raw material handling part. this div has also been steadily improving margins and hence showing stupendous growth.

TAN is at 88% and 105% is possible. they are also studying possibility for debottlenecking.

acid complex is at 74% and they have done 85-90% earlier. but nitric acid is almost at 100% already. they can increase realisation of nitric acid by changing the concentration and charge higher. there is shortage of nitric acid in india.

IPA is at 79% and closer to 100% utilisation is possible. here q4 gpm was lower and they feel this is sustainable. full year margins were higher due to exceptional q1. at gross level ipa contributes 15% to total profit

non core assets are land at pune and investment in australian sub - 700cr could be the value of both. plan to sell this within the next 2 years.

13 Likes

@phreakv6 thanks for the detailed thread. Do you have any insight on the below information ? Also do they have some interest in real estate as well ?

2 Likes

Thanks for the detailed post !

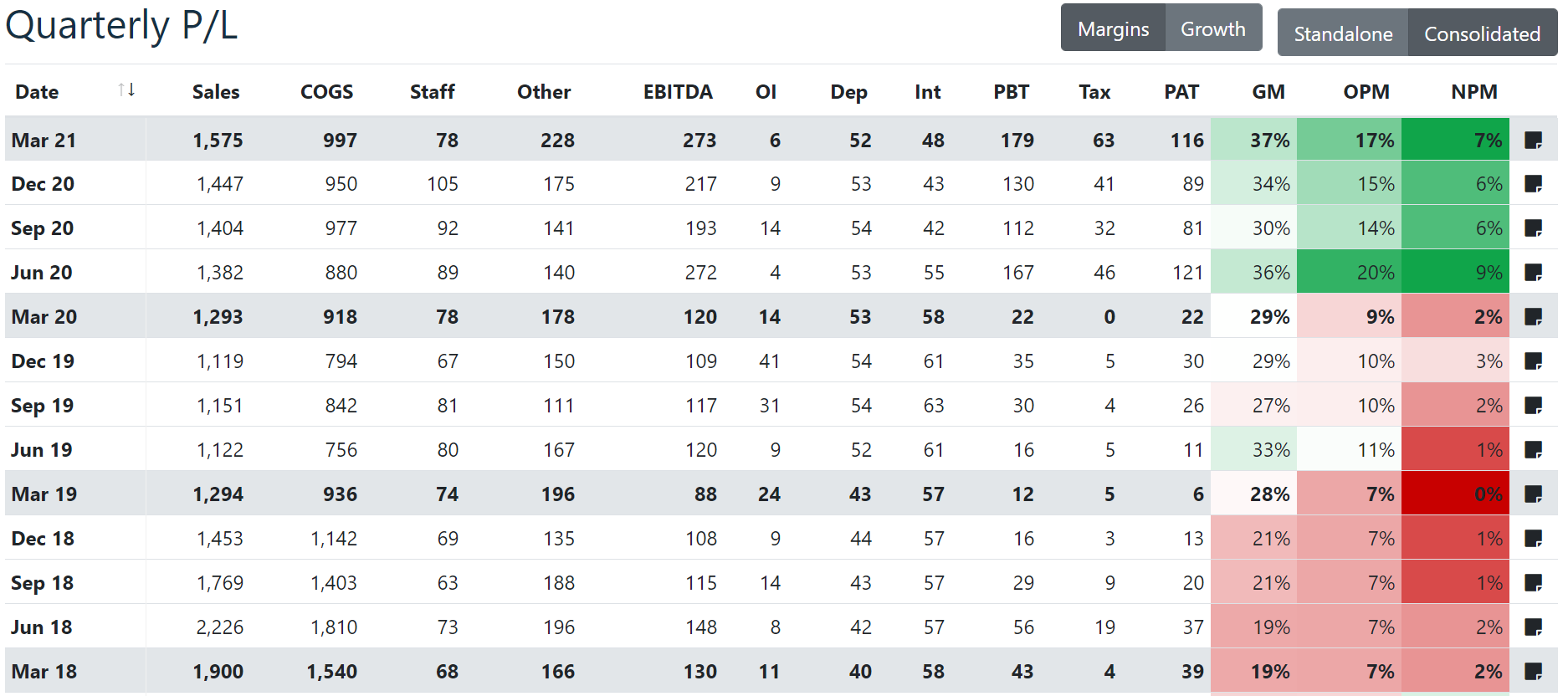

EBIT margins trend over the last 3 years.

Clearly fertilizers segment contributing positively and huge expansion in margins of Chemicals segments

Fertilizer segment positive margins can be attributed to the strategy of company to move from commodity to specialty, value added products (Smartek)

Now what led to the EBIT margin expansion in chemicals segments. Is it volume led growth or better price realization.

But if we look at the volume of chemicals… i don’t see too much variation in volumes. So most probably this could be due to better price realization.

Now the question is can it sustain the kind of realization and margins. If it is the case, then its good candidate for rerating imo.

Disc: have done only preliminary analysis and have only tracking position.

5 Likes

@Rafi_Syed

They own a 10 acres property(4 lakh sq ft retail space) called Creaticity in Pune but it contributes just 0.5 percent to the company and is insignificant. Regards hiving off…

The company is basically trying to move away from their low margin trading business. Most of these are in the industrial chemicals segment. They currently trade Ammonia, Acetone, Toluene, Methanol, Phenol, MX, Acetic Acid, MIBK, SK… They currently produce Methanol, Liquid Carbon dioxide, Nitric Acid and IPA. With their ammonia capex they’ll automatically take care of future ammonia needs and nitric acid too(oxidation of ammonia).

It looks like they are slowly letting go of their traded chemicals business and sticking to IPA, Ammonia, Nitric Acid, Fertilizers(moved to 100 percent differentiated in q4) and TAN(I’m happy they’ve deferred capex here until ammonia capex can aid the margins) which would improve their overall margins. Note that the investor presentations confirm that these are the segments they are looking at.

A few years ago they created a separate entity to house TAN and Fertilizers together(since both need ammonia). What I suspect will happen(speculation from now on in…) is theyll consolidate their business even further and the low margin bulk Chemical trading business and the real estate business will be seperated altogether at some point and we ll have a focused higher margin structured business here Note: Mr Shailesh said the name deepak Fertilizer is a misnomer in the latest concall and I don’t see how they’ll manage 2800 crores for ammonia capex with just 800 crores debt so maybe they are throwing hints at us regards what to expect regards structure and outside investors(end of speculation).

Personally, I am a huge fan of deepak Nitrite and have been tracking deepak fertilizers since last year waiting for that aha moment and the paths followed by deepak mehta and shailesh Mehta are very similar and slowly making sense regards capital allocation and vision(though deepak fertilisers had more of a bumpy ride this past decade).

I agree with @phreakv6 and can see a virtuous cycle of margin improvement alongside the already high revenues which can increase further on full capacity utilisation and debottlenecking (though revenues may drop a bit with the low margin traded chemicals slowing down) which will lead to improvement of cash flows and hopefully interest payments leaving the balance sheet to be replaced by internal accruals for future growth in a few years which will aid Pat even further… but the risks are obvious when dealing with high debt, heavy capex and a sort of decade long turnaround company which is still 2 to 3 years away from reaching the position it wants to be in.

Edit(additional notes):

Currently for FY21 the manufactured chemicals(IPA, TAN, Fertilizers, NA) make up about 76 percent of revenue(4421 crores) with the trading chemicals making up 24 percent(1387 crores). The investor presentations clearly have moved into the direction of only highlighting these and ignoring trading… So when valuating the Company I wouldn’t take the whole sales. its mcap is still cheaper than sales even with this and the margins would be a Lot, Lot higher when removing the low margin trading chemicals so I wouldn’t be surprised if their margins go through the roof as consolidation continues.

Also, they only managed to move to full differentiated fertilizers 100 percent in q4 which led to big volume increase already so expect further improvement there in the near future. Also ammonia prices went up by 11.8 percent in q4 and hence why the margins and ebitda for fertilisers were low so expect improvement there too. Once the complete their ammonia capex this danger will be neutralised(bensulf takes up a small percent of fertiliser revenues so even if phosphor prices rise in the future the impact will be low on this segment once ammonia capex for npk is complete). So the triggers for margin improvement are:

- Consolidation from low margin trading chemicals to their higher margin manufactured chemicals.

- Move to differentiated fertilisers which has already begun for 1 quarter

- Ammonia capex which will improve margins and stability for Almost the entire fertiliser segment and for TAN and NA.

- Debt reduction which will decrease interest costs and improve PAT margins and could happen in a few years(Fy25 at the earliest probably considering planned ammonia and later TAN capex)

- If Their Post ammonia and TAN capex plan concentrates on high margin chemicals capex instead of fertilizers.

Disc: Not invested yet. But could be soon. Not a sebi advisor. Please flag if not adding any value.

19 Likes

Hi,

Just a question… Aren’t all of these commodity products? is there some moat in setting up the facilities/mfg ammonia, IPA or any other product? Do they have pricing power or any differentiation/criticality which will help them compete with Chinese?

Regards,

Nikhil

2 Likes

In commodity chemical mainly in import substitution type, companies try to set up plant as big as possible so that no other local competitor can think of entering and look for the pie,as it is not viable for others as already company which setted up the capacity very big. This itself will acts as a MOAT for this kind of import substitution story . Exactly same thing happened with deepak nitrite story.

8 Likes