Deep Ind Hits an all time high. Today we will know who are the investors who got in through QIP.

2 Likes

Deep Industries at all time highs again…

This is going superbly…

Thanks @kannu for initiating this

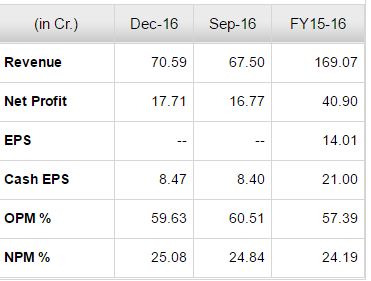

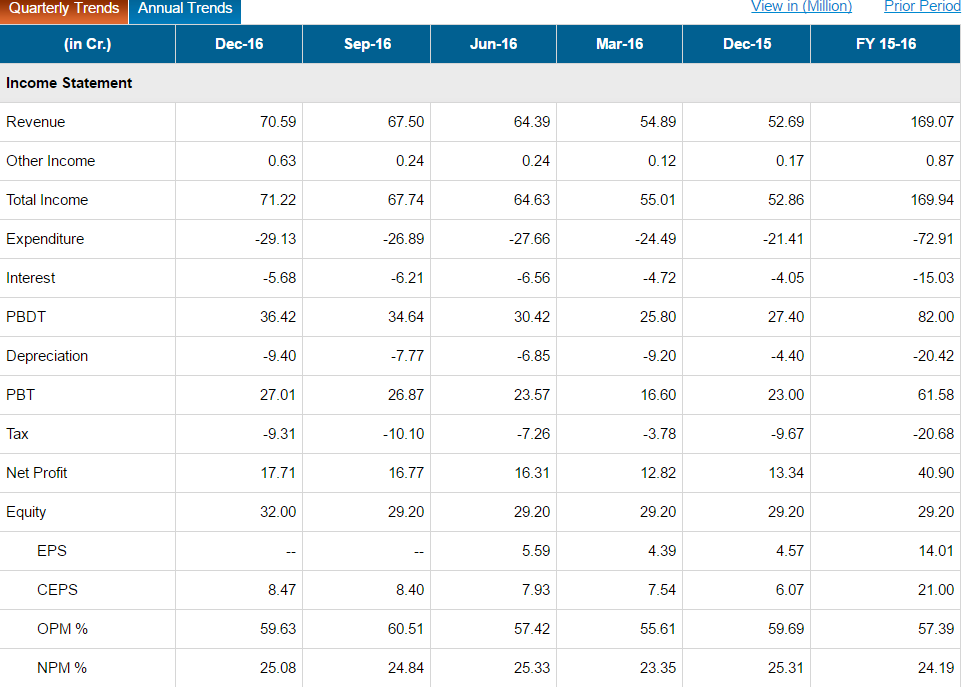

Q3 numbers are in. There seems to be a smudge in the Fax against current qtr EPS but you can X check it with NP figures. Concall is tomorrow @1030 AM

http://www.moneycontrol.com/stocks/reports/deep-industries-standalone-financial-results-limited-review-report-for-december-31-2016-6148321.html

@KS16 Lower EPS - may be due to the QIP in Dec 2016. http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/F796E7FC_7AA3_4245_B9FC_CBA5E873E900_093916.pdf

1 Like

Investor presentation

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/325FC1EC_6331_4A37_A58B_58D8DD87AE30_180205.pdf

1 Like

This is to give a better view of cash EPS, because of the smudge in the scan

This one is from BSE site

1 Like

Good developments in this qtr overall -

Excerpt from presentation…

-

Successfully executed QIP to raise Rs. 63.8crs. Shares issued at Rs. 228/- per equity share. Funding to give flexibility to capitalize on opportunities available in the Oil & Gas Services space.

-

Executed definitive documents for a PE Investment of USD 20mn from Tridevi Capital Partners in to Prabha Energy Private Limited. Deep Industries to hold 51% in Prabha Energy post investment. Funds to be utilized for development and production of Natural Gas from CBM block located in Northern Karanpura coalfields where Prabha Energy holds 25% participating interest.

-

Strengthened Balance Sheet with improved earnings visibility and equity infusion in form of QIP and PE Investment in Subsidiary have led to Upgrade in Credit Rating by CARE. “A” and “A1” for Long term and Short Term Bank Facilities

2 Likes

Thanks @VB1 for capturing the details very well.

One more risk I wish to highlight is the contract risk. I read somewhere the contractual clauses for dehydration business is very harsh.They have to pay a fine of 1Cr/day if the equipment breakdown is for more than 15 days in a year. Also they have to pay heavy LD(Liquidated Damages) if they do not perform as per the expectation.

But overall I am quite positive. For next 3 years they should do very well unless there are any major contractual issues.

Regards,

Raj

Disc: Invested. No trading in last 90 days.

1 Like

hi @raj1968

If i am not wrong, you were investing mainly in consumer facing businesses. Over the past few years, you seemed to have changed the strategy and moved on to b2b type of companies. How do you build conviction in these type of companies.?. Also, how do you first spot them?. Is it by running some screeners?. Would be of great help if you could share your experience. thanks

Hi @gautham1,

You are right, I was into consumer facing businesses mostly. However, they ran very fast and became overvalued(in my views) to a great extent. Also looking back at the rally in Industrial and Cyclical companies forced me to rethink. Gradually I exited from richly valued consumer companies.

I do not use screener much. In fact I do not know to use it to spot opportunities using screener. I get ideas from various sources like TV, magazine articles, blogs and try to see a visible growth and confirmed order book for next 2-3 years besides sector growth. My feel is that they will provide better returns for next couple of years.

I have changed the horses as I felt it was necessary. Hope this helps.

Please look at video below. I respect this gentleman very much.

Regards,

Raj

4 Likes

thanks a lot @raj1968 for sharing your views. appreciate it. you are right about the valuation. thats why i consider 2014 a bad year because one had to sell even though the companies were doing fine.

I am not sure of tv, magazine etc. I think most of the time there will be vested interest.

Anyways good to know that new theme has worked for you. Thanks for that video. I too admire him.

The management of deep ind is now meeting analysts in the US including fidelity. A very positive sign of things to come

DEEP INDS in FOCUS

In a boost to firms like Deep Inds, Reliance

Industries and ONGC, the oil ministry has moved a proposal to

the Cabinet for allowing pricing freedom for natural gas

produced from coal seams.

The ministry has proposed to the Cabinet that coal-bed

methane (CBM) gas producers be given pricing freedom and

allowed to price the fuel at market rates, sources privy to

the development said.

This will help operators quickly put in production the

CBM blocks they hold and reverse the trend of investors

relinquishing coal-seam blocks due to viability issues of

current pricing.

The sources said the CBM gas pricing policy proposed to

the Cabinet is in line with the recently unveiled regime

governing small and marginal oil and natural gas blocks.

The government had recently auctioned small and marginal

discovered oil and gas fields by promising investors complete

pricing, marketing and production freedom under a revenue

sharing contract agreement.

Pricing freedom would help quickly ramp up CBM gas

production to targeted 5.77 mmscmd within a year, they said.

The cabinet has given its approval. Excellent times ahead for Deep Industries

2 Likes

If anyone have subscription then this could be good read…

Do post your analysis after reading.

1 Like

Regarding Deep being an asset intensive business has been discussed on the thread. This is into leasing business and asset turns will be low. If they get more orders, they will have to buy more equipment to service those simultaneously.

I read the article and didn’t find anything new. This thread has more material than probably what the author knows(obviously he has not put his money and hence the details are not required for him).

Deep Industries is a capital intensive business( a well known fact). For every new order they need to go for a capex. Now some important points to ponder.

- Their EBIDTA margin is 55-58%. They recover the cost of equipment is 3 years while the equipment life is 15-20 years. When the renewal of the contract comes they can bid much lower(as the equipment cost is already recovered) and for competition it becomes tough to win.

- Management says that they will grow 30% even without a new order in FY18.

- Their CBM block will start generating revenue from FY19. This project is fully funded now with $20M QIP with Tridevi Capital.

This all ensures good growth for next 2 years without any capex needs.

If a new order comes then only they have to worry about capex but it also starts giving them additional revenue.

Disc: Invested since lower levels and bullish in the prospects. My views are biased and hence please do your own due diligence.

8 Likes

Deep Industries will have their post result earning call at 4PM on 2nd May. The earning call invite is attached. Anybody interested may join in.

Deep Industries Ltd_Q4FY17_ Earnings Call Invite.pdf (104.4 KB)

Regards,

Raj

Great work @VB1 …simply fantastic. Thanks for sharing a 360 degree view.

Regards,

Raj