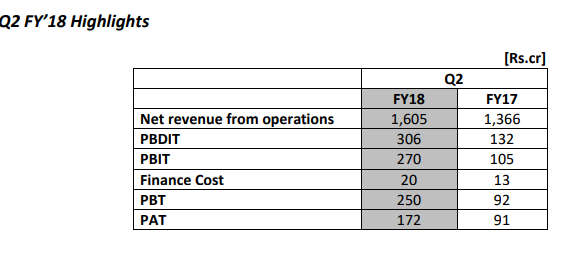

My notes from Q2 FY18 concall. I have left apart numbers and focused on capturing the business aspect of it. Also put their rationale for doing capex now.

Borrowings -

The Gross Debt as at 30th September, 2017 was Rs. 673 crs. and net debt at Rs. -44 crs. vs. Rs. 737 crs. and Rs. 707 crs. respectively, last year. Borrowings are low in Sept./Oct. but move up towards year end as sugar season progresses. Tax Rates will be higher and is likely to remain high with phasing out of exemptions.

Capex underway -

With the objective of strengthening the businesses, primarily on downstream products, Company is implementing projects worth ~Rs. 350 crore in Sugar and Chemicals businesses.

(i) The Distillery will come on-stream by Jan 18 ~190 crores.

(ii) The capex in Caustic Soda at Kota ~Rs. 98 crore and Ammonium Chloride Plant at Bharuch ~43 crore to be commissioned by Jun 2018.

New Capex -

With the objective of increasing capacities along with integration and cost inefficiencies, additional investments worth ~850 crore in Sugar and Chemicals Business along with Power utility has been approved.

(i) Sugar - 500 Crore. Sugar and Co-gen capacity expansion for 360 crore will be commissioned by Oct 18. Distillery capacity expansion for Rs. 140 crore will be commissioned by Oct 2019.

(ii) Chemicals - 98 crore. The capacity increase at Bharuch will be commissioned by April 19 and at Kota by Sep 19.

(iii) Power - 240 crore to setup a new Power plant at Kota in part replacement of existing power plants, completion is expected by Sep 2019.The new plant will be ~22% more efficient than the existing one.

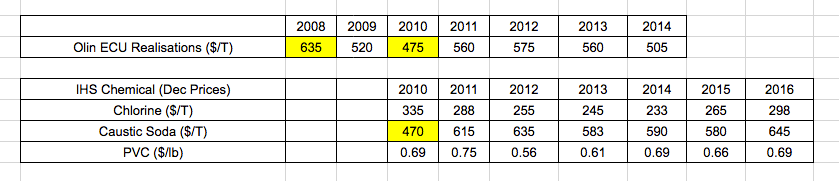

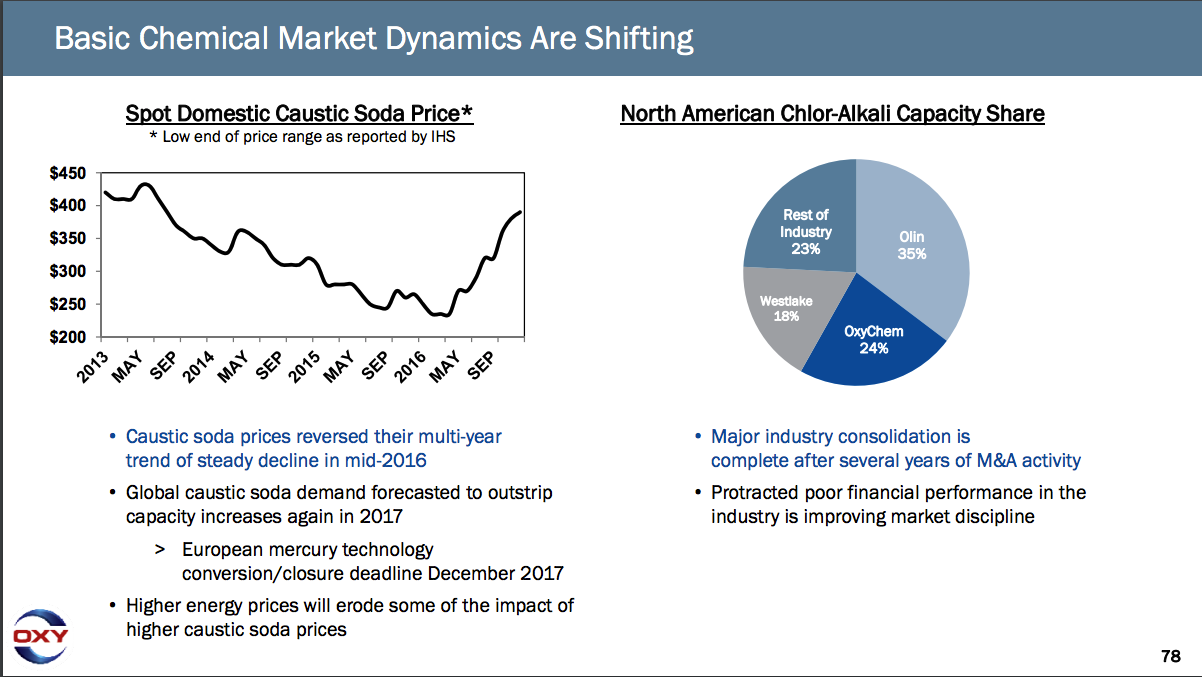

Chloro Vinyl vertical is operating at 90% utilization. Chlorine absorption in market is improving. This would lead to further improvements in capacity utilization over the next few months. The prices of Chlor-Alkali firmed up during the quarter, up 9% over Q1’18 and 28% over last year. They do not enter into long term contracts. It is all spot based pricing.

Chlorine is attracting negative price at the moment. On an ECU basis, they are stable and are continuously seeing how to improve. Already have 4-5 companies who are pipeline buyers of chlorine from Gujarat factory, so with them we have a flexible long-term contract on chlorine supplies based on the market prices, so trying to hedge their bets from all corners to make sure that they are in a stable position on the ECU realization.

On talks about capex being done at cyclical peaks - “It is very difficult to say and I think our estimate in next few quarters should be satisfactory. The prices should remain firm internationally and nationally, but I think predicting commodity cycle is very, very difficult.”

In March April next year, Aditya Birla Group is also coming up with an expansion, so that is going to have an impact in totality on the industry. Fortunately the chloro akali industry is growing at 5-6% per year, so that is a positive.

PVC and carbide prices are stable, though coke costs are rising. On question about when will PVC capex be done, mgmt said don’t have any plans yet. (I think this is because PVC through carbide route is pollution intensive. Also, the PVC quality through this route is comparatively lower than that of EDC route. )

Sugar -

The Sugar capacity utilization reached ~85% in FY16-17 from ~60% in the FY15-16. This year, crushing has started early and they expect to reach ~100% utilization. Inventory level as at 30.09.2017 was 3.9 lac qtls. (vs. 6.0 lac qtl. last year) valued at Rs. 2,9.70/Kg. Margins would be similar to that of last year as few things like cane pricing has risen but recovery would improve. The 150 KLD molasses based Distillery is progressing as per plan and is expected to be completed by Dec’17. This will further strengthen sugar business.

Rationale for sugar capex - Cane availability in UP is improving due to better acreage and better cane variety resulting in 1.5 times better crop. Read more about UP Sugar industry updates - Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains!

Industry fundamentals have been positive over last few years. In view of this the Board has approved expansion. This involves Sugar Capacity addition of 5000 TCD, Co-gen by 34 MW and Distillery by 100 KLD. These investments will take total Sugar capacity to 38000 TCD, Distillery to 250 KLD and Power to 145 MW and will make them highly integrated. This is to balance our entire portfolio in the sugar business so that they have value addition happening on all three products. As far as costs are concerned, the fixed cost will be absorbed over a larger sugar volume, so the business will become more cost efficient.

They are hopeful of implementation of the Rangarajan formula for cane price fixation; having the same government in the center and the states will make a difference. The focus is to ensure that there are no cane arrears to the farmer at the end of the season and to ensure that all the four components of the industry which is the industry, the farmer, the consumer, and the Government have a stable sugar industry. Sugar recovery in UP has moved almost to Maharashtra level. Governments have been more rational in policies compared to what they were earlier, so therefore, they are expecting reasonably good returns from the sugar industry going forward and that is the reason of going ahead with the expansion.

They did last sugar capex in 2007-08 (primarily on sugar capacity expansion); cane wasn’t available at that time. They had to undertake efforts to expand the cane area, so capacity utilization took time. Unlike last time, this time, they have a ready cane area and the cane intensity is pretty high and rising very fast, so therefore, they do not expect too long a period for capacity utilization. The second change is that they were not integrated last time, whereas now are, so therefore, scale gives benefit on the byproduct as well which is not dependent on sugar cycle; third fundamental change is with respect to the UP recovery which has moved up and is comparable to Maharashtra, so we are more competitive compared to them. Also, it was not only DCM group that invested in sugar in 2007-08, but at least 30 new factories came up in UP and there were also Brownfield expansions in the existing factories. So the capacity expansion in UP per se increased dramatically in that period because of the Government policy. This time, no one is doing capex other than DCM.

Sugar is ~15% ROCE business (except few bad years in downturn).

Bioseeds performance has been improving both domestically and internationally. They expect satisfactory growth going ahead. Losses are getting reduced both in India and internationally. They have very strong research capabilities and many new products are under testing. Will launch as and when they think time is right. Didn’t commit anything!

Farm solutions - The growth in this business is expected to remain muted in the near term. Regarding value-added part of this vertical, they said they are working more intensively to get more products, get some new sources of getting their agri inputs of how to carry those forward to grow this business further. We do feel agriculture that way does require a lot of knowledge and quality inputs at the right time. We are also looking at the Crop Care Chemical business. Seeing what we can do and what we can take up more actively and we are looking at seeds now in their own vertical of wheat and couple of other products. That is also growing well in their market area. So all this combined should give this business stability

Fertilizer - The Subsidy outstanding position continues to be a matter of concern in absence of consistency in release of subsidy payments with the implementation of DBT. DBT mechanism is not working seamlessly. Will take time.

Fenesta - The business is witnessing continuous growth in revenue and earnings led by higher billing. However they are experiencing lower order bookings in ‘project’ vertical, a result of slowdown in real estate industry. Retail segment bookings are growing at a slower pace. The business is making positive PBT over last several quarters.