January 2018

Caustic soda prices increase around 43% y-o-y in January 2018. Prices rule between Rs.47-58 per kg December 2017

Caustic soda prices rise 28-33% in y-o-y December 2017. Prices rule between Rs.42-54 per kg.

Caustic soda production grows 12.6% in December 2017. Output up 5% during April-December 2017. November 2017

Caustic soda prices increase 27-32% y-o-y in November 2017. Prices rule between Rs.39-49 per kg.

Output of caustic soda increases 11.6% in November 2017. Owing to healthy demand from aluminium and soaps & detergents industries October 2017

Caustic soda prices continue to increase at robust pace in October 2017. Prices rise by 29-32%.

Caustic soda output grows 6% in October 2017. Production stands at 234.1 thousand tonnes. September 2017

Caustic soda production grows by 4.7% y-o-y in September 2017. Output stands at 229.1 thousand tonnes. August 2017

Caustic soda prices rise at robust pace in August 2017. Prices increase by 24-32%.

Caustic soda production grows by 2.2% y-o-y in August 2017. Cumulative output increases by 2.1% during April-August 2017. July 2017

Caustic soda prices rise at robust pace in July 2017. Prices to increase by 7-12% in 2017-18.

Caustic soda output falls by 2.9% y-o-y in July 2017. Production increases by 2.1% during April-July 2017. June 2017

Caustic soda prices touch all-time high in June 2017 Prices increase by 28-32% during April-June 2017.

Caustic soda production grows by 1% y-o-y in June 2017. Cumulative output increases by 3.9% in June 2017 quarter. May 2017

Caustic soda prices increase at robust pace in May 2017 Prices to rise by 4-6% in 2017-18

As Samiit Vartak points out, peak valuations and peak earnings are a deadly combination. What the sugar cycle is now seeing is that supply is ramping up fast because of a normal monsoon in 2016 and 2017 - crushing season for the coming year should have good output as well, thereby keeping prices in check. On the caustic front, I cannot fathom pricing of more than 38,000/tonne and that in my opinion is well built into current valuations for DCM. Risk reward not in line for me

Disc - exited a couple of months back as I could not see incremental delta in profitability

While caustic prices may have peaked at INR 36000 - 40000 / T, why do you assume that the situation with the co-products, viz., hydrogen and chlorine will remain the same? Maybe with increased downstream consumption of these products, there will be a higher realization in the coming quarters.

Agree with your view on sugar.

that is because Chlorine has negative pricing which mostly compliments pricing of Caustic - so if Chlorine prices do recover, they might have a rub off effect on the prices of Caustic Soda. And at such earnings, even if you have one thing going for you, there are 10 other things stacked up against you.

I have exited DCM Shriram mainly due to the reversal in sugar cycle. I still have a positive opinion on the company/mgmt/ business. It was a difficult call because of the following:

The +ves

a) Although the sugar cycle has turned both locally and globally DCM Shriram is one of the most efficient players in the industry and is cash +ve. Being efficient and fully integrated of one includes the realisations from power and distillery DCM Shriram’s sugar division will remain profitabable until sugar breaches 27 (similar to Balrampur). Most mills in the country will close down if sugar remains at those levels.

c) Both Caustic soda and Chlorine prices are at yearly highs making ECU realisations all time high. Although commodity a look at last 10 years of Caustic Soda and the current Chinese issues I do not see ECU realisations cooling off in a hurry.

The -ves

a) Sugar is excess both locally/globally and also from a production perspective. Normally once a farmer gets into sugarcane sowing he does it for four years. The acreage under sugarcane has gone up significantly this year.

b) Grasim’s new capacity is coming up in Gujarat and could impact ECU realisations next quarter.

c) The govt control on BT Cotton seed prices dampens any hopes of incremental gains from the BioSeed business and is a -ve on GM seed industry as a whole.

Finally DCM was a great learning experience and I will keep tracking the company and sugar sector closely. What is very interesting is in the entire sugar cycle most southern companies did not make any money and if the same situation continues in sugar they will be in deep trouble and what happens to them will give us some idea about the cycle.

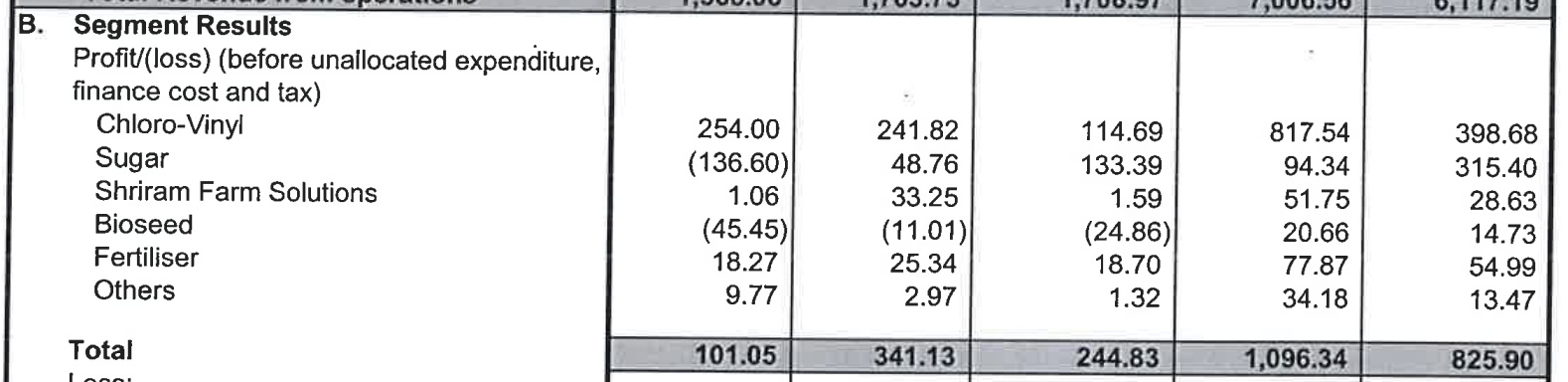

As expected Sugar is in really bad shape. DCM is one of the better players in realizations & efficiency and yet PBIT has gone from 48Cr to -136Cr. QoQ.

Despite such massive hit, I am thinking of holding on to small allocation in DCM Shriram (and ride through the tough times) because of following reasons -

Good Management: The management of DCM Shriram is absolutely fabulous. The level of disclosures, shareholder communication and corporate governance is top class. Due to strong background/history, I feel like they are averse to number dressing or taking short term decisions. Even in commodity businesses, they have superior OPM, ROCE, WC management in both Chlor-Alkali and Sugar businesses vis-a-vis competition. Even at the worst of Chlor-Alkali cycle, ROCE does not go below 13%.

Capex: Chlor-Alkali ECU is expected to soften due to additional capacities that might come in but I dont think the prices will fall in a hurry. As management described, Chlorine realizations have turned positive. Also additional capacities of DCM might support some moderate level of growth in Chlor-Alkali business. Further the PBIT margins in power business are 60%+. I am hoping power business along with distillery might help to rein in losses at the downturn of Sugar cycle.

Two Quality Businesses: Fenesta remains a very good business with a rising brand. The PBIT of 30Cr. for FY18 is encouraging. Although the government pricing action to reduce prices of cotton seeds are negative for GM industry, Bio-seed spends a lot more amount on R&D compared to some other seed companies in this industry. I am hoping that management can scale this business up.

Capital allocation: Capital allocation is probably one area where DCM management has a little bit average record due to decision to expand Sugar capacities. Though across an entire sugar cycle (4-5 years), ROCE is 20%. Apart from this one decision, they have taken capital out of Hariyali business, reducing bulk fertilizer business, not growing cement business. They have poured that capital into Chlor-Alkali business which has very attractive ROCE for last 13 years & Fenesta (a standalone player might not have spent enough to build this business due to upfront capital requirements).

I may be completely wrong in holding onto DCM Shriram but it feels like this is the management that can help to create a lot of shareholder wealth.

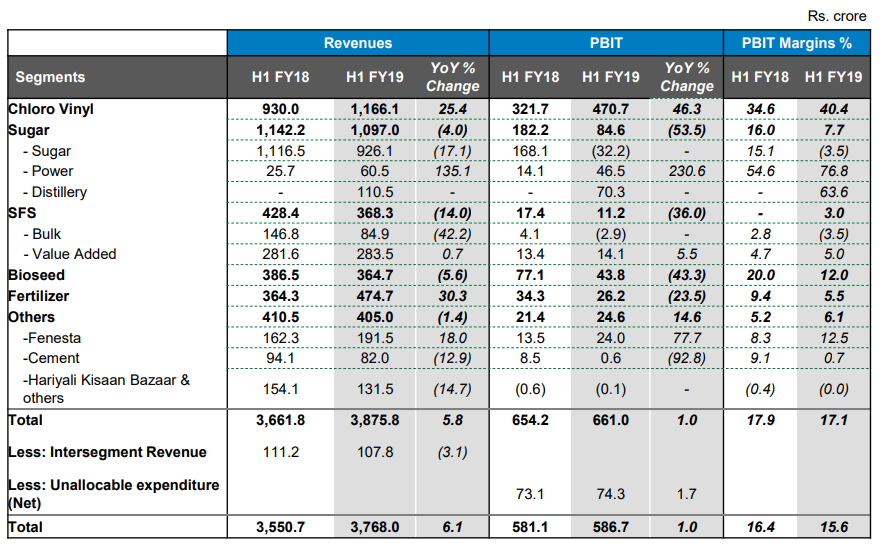

Sugar looks interesting as International sugar prices are at their 8 month high and if one adds Rupee depreciation the price which was 21/22 a quarter back is now 27. Brazil sugar forecast is 21 mn tonnes down from 26.5 min tonnes. The other thing if one looks at DCM Shriram (and other sugar companies) is the impact of distillery revenue. Distillery PBIT is 70 cr in first year of operation, Distillery + Power PBIT is 115 cr up from 14 cr last year. Any revival is sugar prices can become extremely +ve.

Another interesting aspect of DCM Shriram is the Fenesta breakup: Fenesta sales have gone up by 18% but due to op. leverage coming into play Fenesta has delivered a PBIT of 24 cr in the first half.

I hold three sugar companies and all three including DCM Shriram have diversified businesses, but what worries me is the share of sugar business compared to other businesses.

I would prefer they start increasing turnover of other businesses since sugar is unstable and faces lots of govt meddling.

Fortunately, DCM Shriram is able to perform well enough.

I have visited Fenesta showroom again after long time. Few points(most points are specific to the branch)

Overall demand for fenesta windows continues to be robust with growth of around 30%.

Project devision has done well this year grown at 50%(Which I never expected considering real estate slowdown). Big RE players like Brigade,Prestige estates are major customers.

Retail business has grown at around 25%. Doing lot of promotional activities to increase retail sales.

Products are customized as per the requirement of customers/projects.

Upvc door products are withdrawn from the market as it was not doing well. Launched new doors made up of wood pvc(WPVC) for bathroom.

Upvc windows are very reliable in quality having life of 20-25 yrs,less pollutant and easy to maintain.

White finished windows are preferred for projects which takes around 30 days for installation.

Wooden finished windows are used by individual homes which takes 45 days for installation.

Once customer approaches Fenesta, service person will visit the place and takes initial measurements for estimation. Laser based precise measurements are done before confirmation and installation.

For small orders less than 2 lac customer have to pay the amount upfront before placing the order. Orders between 2 to 5 lac,50% of money has to be paid during confirmation and remaining before installation. More than 10 lac orders,customer has to pay 10% upfront and remaining in two installments.

Optically very good nos from DCM Shriram for the quarter and the year.

But if one goes into details, sugar has been the game changer. And chlor alkali keeps steady growth with good margins. The fertiliser and bioseeds business seems to be the dampeners to the overall picture.

Its great to see management consistently keep giving detailed presentation and explaining their various businesses in details.

A large part of capex seems to be done but still remaining capex likely to be finished by end of fy 20.

Valuation wise it quotes at 7-8 PE and for a company showing good numbers, with decent management and capex likely to play out over next few quarters this seems to be a company to atleast keep on the watchlist.

Actually pretty good performance. The caustic soda segment continues to generate very good margins and prices of the product have improved further. Same thing has been there in Andhra Sugar too. I feel these cos deserve better valuations

I think Hitesh Bhai did mention the right word ‘Optically’. Two things and which should be a cause for concern:

a) The company is carrying an inventory of 38.89 lac quintals at a carrying price of 3049 per quintal. This comes to around 1200 crores. A lot of it will be financed by soft loans from the government but one needs to understand with quotas imposed on sugar mills how will this quantity get out of system? International white sugar prices are around Rs 23 per tonne. Sugar being a highly remunerative crop the farmer too has no incentive to switch.

b) The fall in ECU realization should be understood to see if it is some kind of trend, since all the three major players in India Grasim/GACL and DCM are coming up with higher capacities.

Personally, it seemed to me from the results that Sugar now can be profitable at a price around Rs 30/kg, because of co-gen and distillery. It is also that because of the new cane variety, UP sugar mills seem to be doing recovery of 12% or so, compared to only 10% or so, a few years ago.