@smallcapvaluefind Yes I do feel that froma risk reward point of view, DCB is a top pick. THis is mainly because the risk right now in the banking space for small banks is high, and DCB minimizes this risk the most. Growth will come in the future, I’m not worried about that at all. Survive over thrive for now as far as I see it

The issue with this bank is low cost funding i.e. liability profile. See IDFC first, Bandhan and other new and small banks like.Federal, how they are building their liability frenchise. This bank’s CASA ratio is coming down continuously. That is why NIM is coming down. I dont see good customer care in this bank as I have current account with them. Even I am planning to switch.

But one thing is sure, their books are clean.

1 Like

@Rajesh1975 Not sure if I’m missing something, but isn’t low cost of liabilities a good thing? DCB has a cost of liabilities of about 6.7% in spite of the low casa. IDFC first on the other hand has a cost of liablities of 8.5% in spite of a high casa.

My sense is that the reason for this is the over-aggressive style of IDFC First. Their credit to deposits ratio is 1.3 as compared to 0.84 for DCB (For reference, HDFC Bank is 0.9). This means that IDFC First is giving out loans very aggressively. This strategy can turn out very bad if NPAs rise. DCB on the other hand is conservative and thats why they have a high cash adequacy. in Covid times, safety first is the right principle.

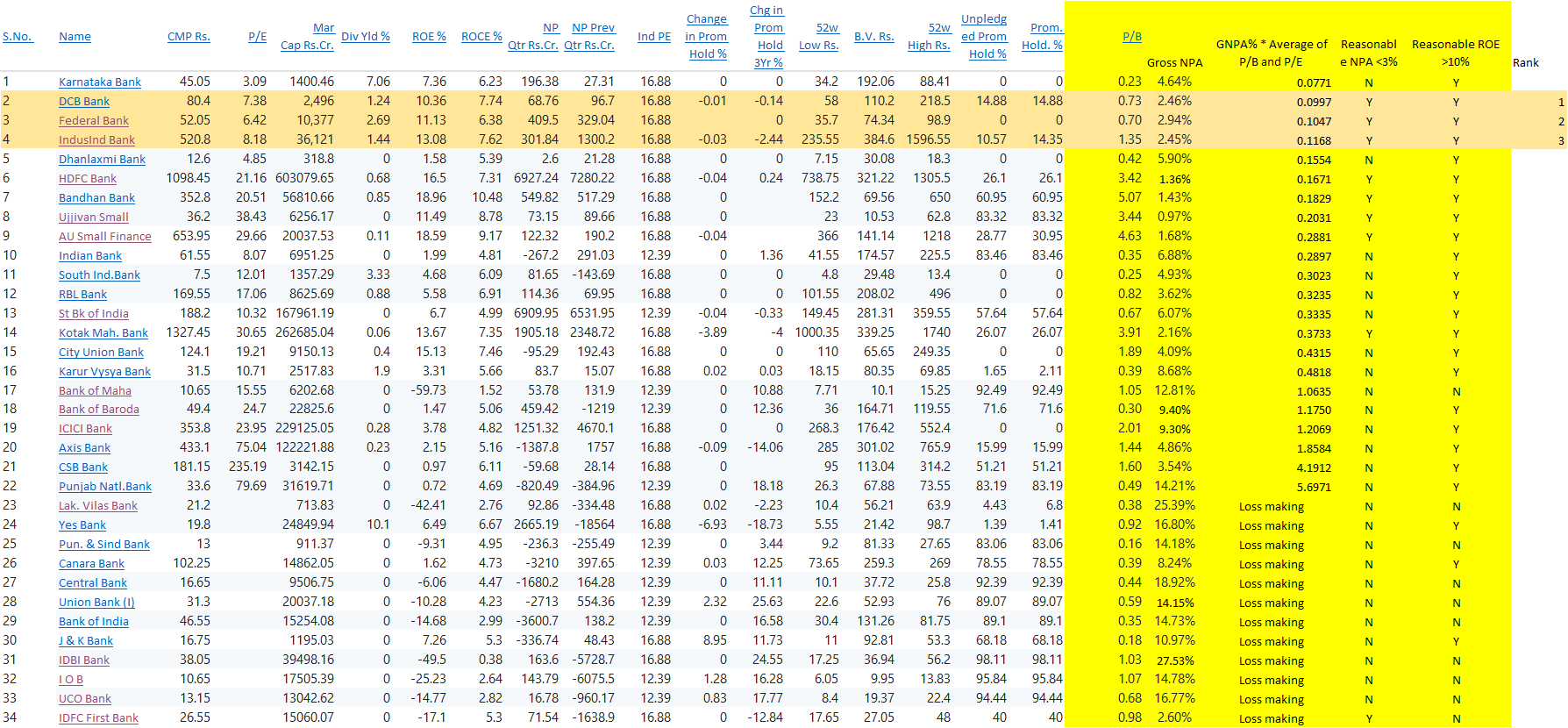

Just refreshed the latest analysis as of 20th July…

DCB is cheapest followed by Federal and IndusIndia bank

Methodology below

1 Like

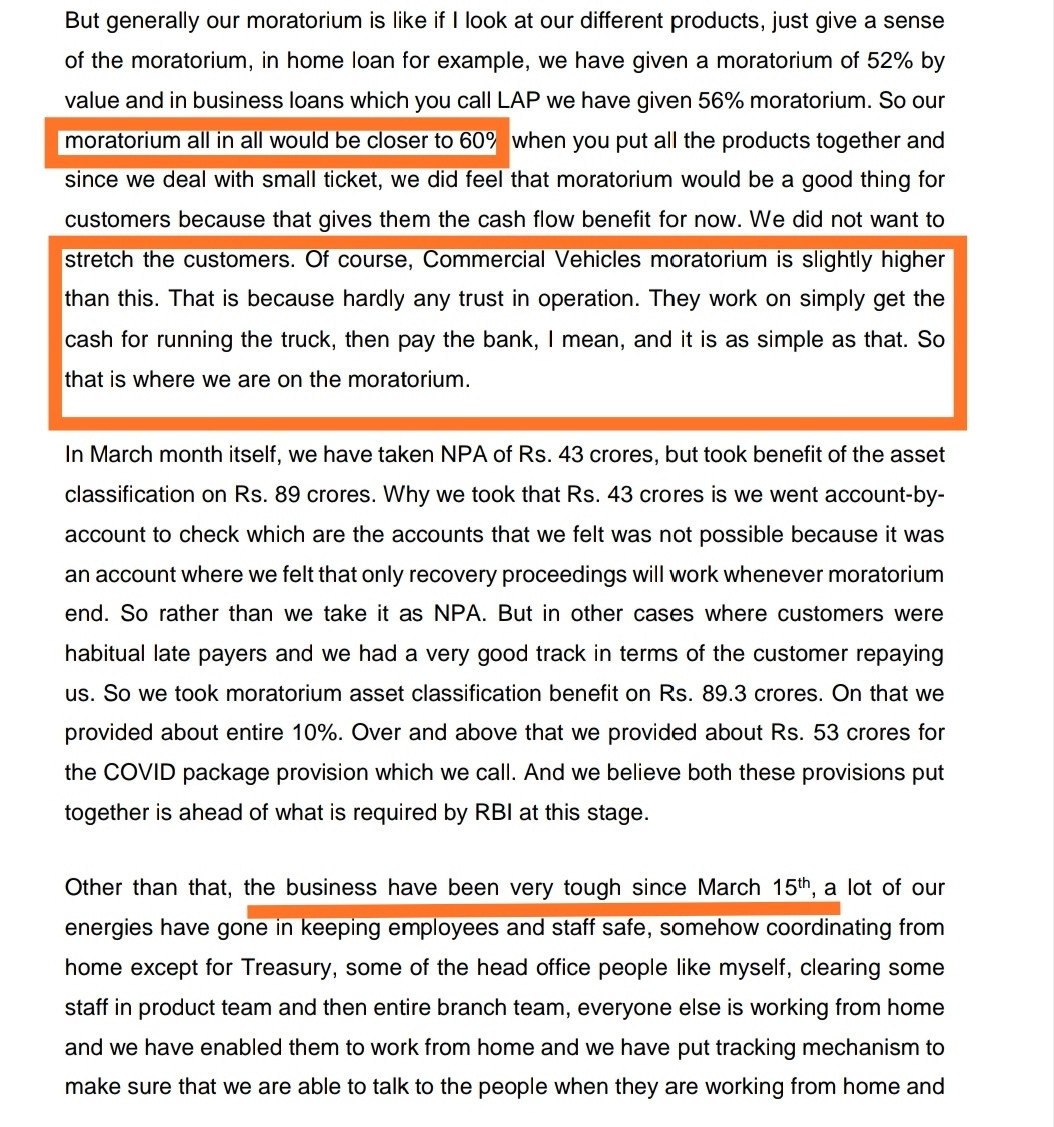

Here’s a snapshot from the investor presentation of Q4FY20 results where they’ve disclosed the moratorium figures

So, it’s 60% of the total book as of March 31st, CV is expectedly higher (no specific number mentioned)

Management has a positive view on the moratorium on the home loan portfolio which constitutes to 38% of the book and 79% are self-employed

Fun fact - The word “Moratorium” was mentioned 78 times in the earnings concall

3 Likes

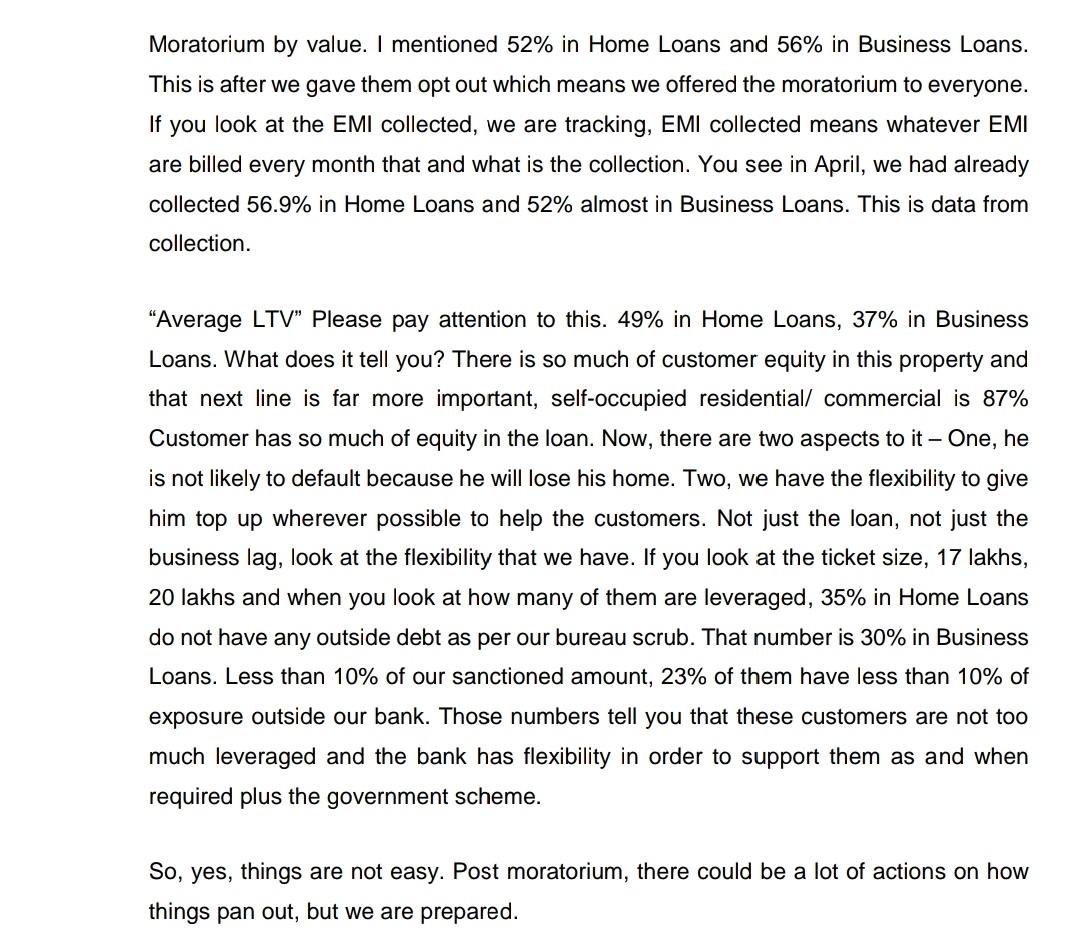

Moratorium has been reduced from Rs 1,908.1 crore as on March 31, 2020, to Rs 710 crore on May 31, 2020,” the bank said in an exchange disclosure on 17th June.

Latest moratorium figures may be disclosed in upcoming Q1 results press release.

1 Like

I want to know, I have not been tracking this stock. Considering they becoming a small bank, Is it worth investing in this company considering the risk it has. Wouldn’t it be better to have HDFC bank, even if DCF banks perform well by how much margin they can give returns considering the risk we would take?

1 Like

Results declared by dcb

1 Like

Management comments/concall takeaways:

Collection Efficiency: Collection efficiencies for Business loan/LAP and CV loans as of Sep

were 87.5%/91.3% and 77.1% respectively compared to pre covid level of 97.5%/ 98.5%

and 92.1% respectively . 93% of MFI borrowers have paid at least one EMIs.

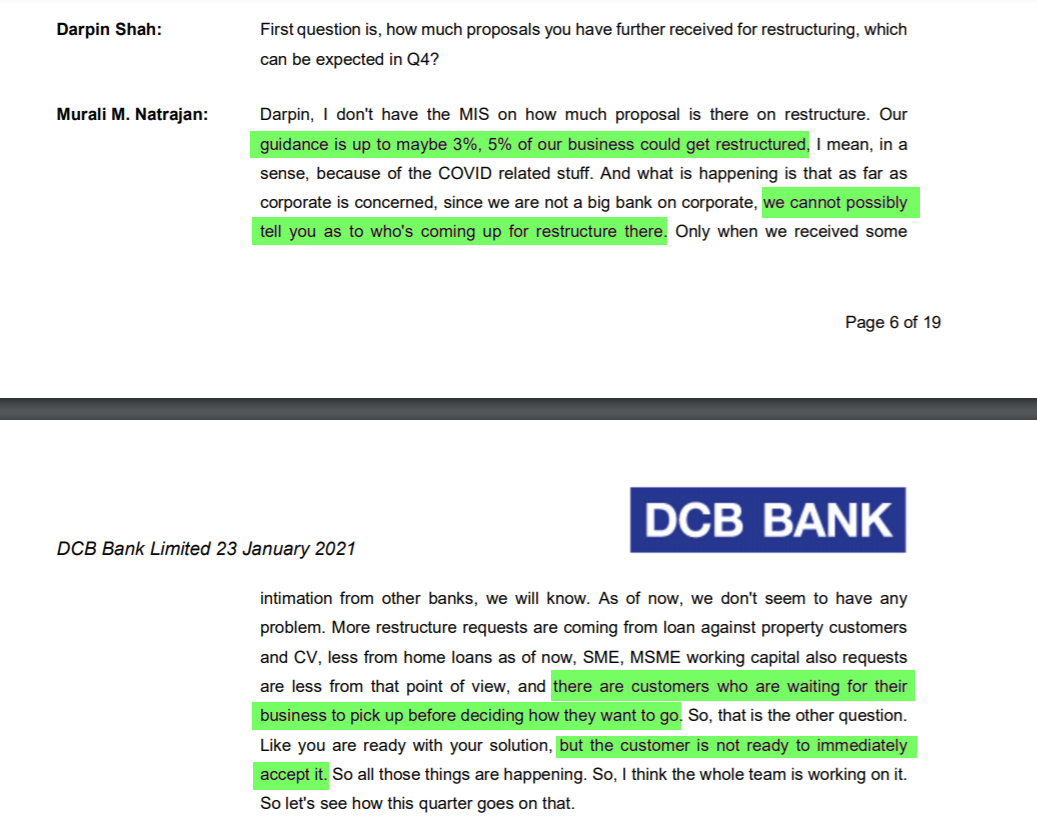

Restructuring: Bank expect restructuring to the tune of 3%-5%. Slippage to remain

elevated for next 3-4 quarters.

Credit growth Outlook: Bank intends to focus on LAP, Home Loans, Gold Loans, KCC,

Tractor Loans and short-term Corporate Loans. Based on current outlook, the Advances

for the full year may remain flat to FY 2020 or may de-grow slightly.

Disbursement: During the quarter Bank disbursed Rs 18.1bn. (Corporate Banking Rs 4.6

bn, AIB Rs 4.1bn, Gold Loan Rs 4.0 bn, Mortgage Rs 2.7bn., SME/MSME Rs 1.5bn)

ECLGS: Under ECLGS Bank has sanctioned Rs 20 bn. Customers have so far drawn down

Rs 3.0bn and the balance is expected to be disbursed by December 31, 2020.

4 Likes

Anyone still tracking?

DCB is now trading at below book value again. I didn’t find any red flags in the results or the concall which would warrant this kind of a beating down, much worse than other comparable banks.

4 Likes

Marcellus has exited DCB Bank completely and entered AAVAS Financiers

2 Likes

Where did this info come up

Look at the portfolio update section

“Exit DCB Bank: We have completely exited from our DCB Bank position in our portfolio. The reasons for the exit are: (i) While DCB has historically been conservative in its underwriting, the impact of Covid-19 on DCB Bank has been higher than many other lenders due to DCB’s focus on the SME/MSME segments; and (ii) the recovery for DCB will be more uncertain and will take longer than for the larger banks. This is because DCB’s relatively smaller size and focus on the self-employed segment which limits the levers available to improve RoAs to pre-Covid levels and accelerate growth. The higher stress on DCB’s balance sheet is evident from the high restructuring loan book along with collection efficiency trends reported in the Q3FY21 results. We therefore believe that unlike some of the other lenders which have frontloaded provisions, the impact of Covid on DCB’s profitability will not be limited to FY21 only but continue to impact credit costs in FY22 as well.”

Nothing that the market doesn’t know.

5 Likes

Hi @Vineetjain111; @smallcapvaluefind, @Vinay_T_M & others who’re tracking - how much of that (Marcellus view) do you concur with. Think there are multiple good things with the bank like a granular loan book, conservative approach to lending, sticky term deposits, and quoting at such low valuations. As for the MSME loan book, believe most of that should be secured and I see even the small businesses are finding their feet now. Views around whether you’re holding still or have exited too lately. Thanks so much in advance.

1 Like

Marcellus has very high standards - and decent returns that make those high standards look a bit haughty in comparison ;). Their strategy is to go after the most loved and most consistent stocks which are overvalued and enjoy the ride. High price to book but decent earnings yield is what end up with and still make those decent returns due to the quality factor.

I would not just get discouraged by that. Marcellus stocks have been big laggards in my portfolio in the recent upcycle. It is after all a risk on environment after a long many years, while Marcellus is geared for a more long term balanced environment

Disc: entered at 100 recently. Also accumulating CUB gradually.

4 Likes

I believe that Marcellus’ reasoning is spot on! DCB was already struggling for growth in FY20 due to the slowing economy. Murali Natarajanji took a conservative approach by focusing more on asset quality than growth. This explains the lower return ratios from thereon.

However, COVID really has had a big impact on the bank’s asset quality due to rising stress levels from their key customer base (small businesses/self-employed). Since most of their book is backed by physical assets, there are high chances the losses will be limited but a 5% restructuring smells danger

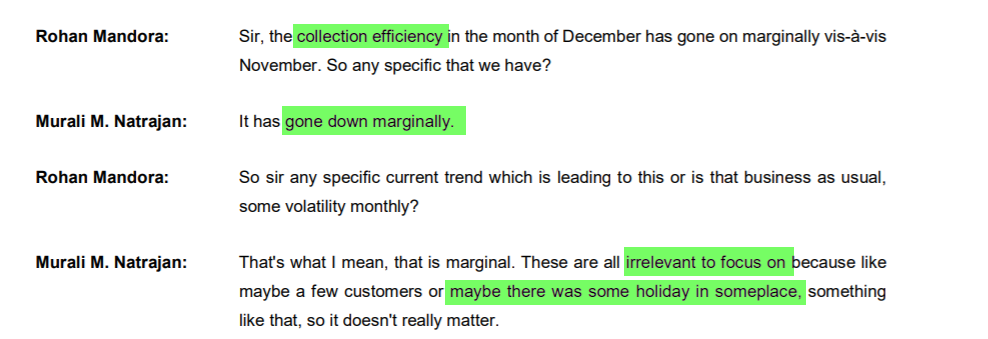

The bank is also struggling on the collection efficiency front as their collection in home loan and mortgages has slipped below 94%. When asked about a decline in the collection MOM, this is what the management has to say

The deposit growth is also down 3% YOY (down 5% from March 20 levels) which isn’t a positive sign either. The credit-deposit has taken a hit because of decreasing liability base, it now stands at 87% (vs the average of 82-84% previously).

My theory - Due to increasing NPAs, DCB would struggle to achieve a 14-15% ROE which is an expectation from the investor community. To further explain this, let’s do a Dupont analysis. ROE = ROA*financial leverage. Since DCB’s ROA is consistently struggling below 1%, an increase in NPAs would mean an even lower ROA for the next 1-2 years. DCBs leverage is already high, consistently over 10 and they would have to make 1.5% ROA to reach the desired 15% ROE. This means that they would have to take more risk (increase in financial leverage). This is what Marcellus is saying in point 2. Nobody knows when/how they can reach a ROA of 1.5%.

At 4% NPA, DCBs book value will come down by ~30%. Just think about it, a book value of 1000 was making 1% ROA. Now that the book value is 700, to make the same profits the ROA has to go up 1.4% whereas we expect it to be lower due to the increase in losses. Controlling the asset quality and growing would become a big problem for DBC in the coming years. To survive the NPAs, they would also need to raise more capital (obviously at these low PB ratio).

Disc - exited DCB

- If you want to understand the relationship between leverage and ROE better, here’s a case study of Hdfc bank and Kotak Bank: Kotak’s standalone ROE is consistently around 12-13% whereas HDFC Bank has 17-18% ROE. Is HDFC Bank clearly better than Kotak?

Nope. Hdfc bank is taking a much higher risk compared to generate the returns. Hdfc bank’s financial leverage is 9x whereas it’s only 7x for Kotak. So, HDFC Bank is taking higher risk to generate additional returns for the shareholders. ROA of HDFC Bank is 1.9% while it’s 2.1% for Kotak. Also, the asset turnover for HDFC Bank is 0.08 while it’s 0.09 for Kotak. Higher efficiency. One of the crucial things is to access the quality of loans (quality of the borrower). The nature of lending is critical here. The approach of “Stay and succeed” >> taking higher risks to generate better returns

2 Likes

Several assumptions & Leaps of judgment IMHO

First About RoE getting to 14% - The call clearly establishes the 6 -8 quarter guide path to achieving it. Quote from the con call below.

As far as ROE is concerned, the next 12-months or four quarters will go in dealing

with the COVID-related challenges. We are working towards the 2.2% cost to average

assets metric. Our NIM, barring maybe one or two quarters of dealing with some NPA

or stress book should be in the range of 3.65 to 3.7. We are working towards 110 basis

points of fee. On a steady state, I think our credit cost should be about 50, 55 basis

points. That is how we plan to have a much higher ROA, that is about 110, 120 kind of

ROA and that will lead us to deliver 14% ROE. I do think that we need about four to six

quarters to kind of reach that level

Second - On 4% NPA resulting in wiping out 30% of book value. I think you’re mixing up GNPA with NNPA, not to mention the actual loss to default ratio is less than 20% so far & a majority of the book is secured with the largest ticket item among the NPA’s being mortgages (197 cr) and a third of the AIB book is also mortgages.

Third - The need to raise more capital - Their current CRAR is upwards of 18%. I think they should be good for atleast 18-24 months.

Four - Below is a comparison of various Indian banks just for reference. If you examine it closely (especially among) the smaller banks (which it is) I think it is doing fairly in line so the investment thesis is on a valuation catch up if the management delivers. That is the big If ! You seem to be convinced that Murli wont be up to the task & I think there is a chance he could , its the opposing views that make the market I suppose

I just wanted to set the facts straight.

| Narration | ICICI | Kotak | SBI | HDFC Bank | DCB Bank | IDFC |

|---|---|---|---|---|---|---|

| Net Interest Margin | 3.67% | 4.58% | 3.12% | 4.20% | 3.75% | 4.65% |

| Gross NPA | 4.38% | 2.26% | 4.77% | 0.81% | 1.96% | 1.33% |

| CASA Ratio | 41.80% | 58.90% | 45.15% | 43.00% | 23.00% | 48.31% |

| CASA vs Liabilities | 24.88% | 40.17% | 34.57% | 33.04% | 17.53% | 26.16% |

| Credit Deposit Ratio | 83.79% | 80.70% | 62.00% | 85.15% | 87.67% | 126.06% |

| Fresh Slippages - Quarterly | 471 | 264 | 237 | 0 | 0 | 0.00% |

| Tier 2 Capital | 1.39% | 0.60% | 2.77% | 1.30% | 4.06% | 0.51% |

| Net NPA | 0.63% | 0.50% | 1.23% | 0.09% | 0.59% | 0.33% |

| Yield On Advances | 8.44% | n/a | 8.16% | 0.00% | 11.19% | 0.00% |

| Capital Adequacy Ratio | 18.04% | 24.90% | 14.50% | 18.90% | 18.32% | 14.33% |

| Tier I Capital | 16.65% | 24.30% | 11.73% | 17.60% | 14.26% | 13.82% |

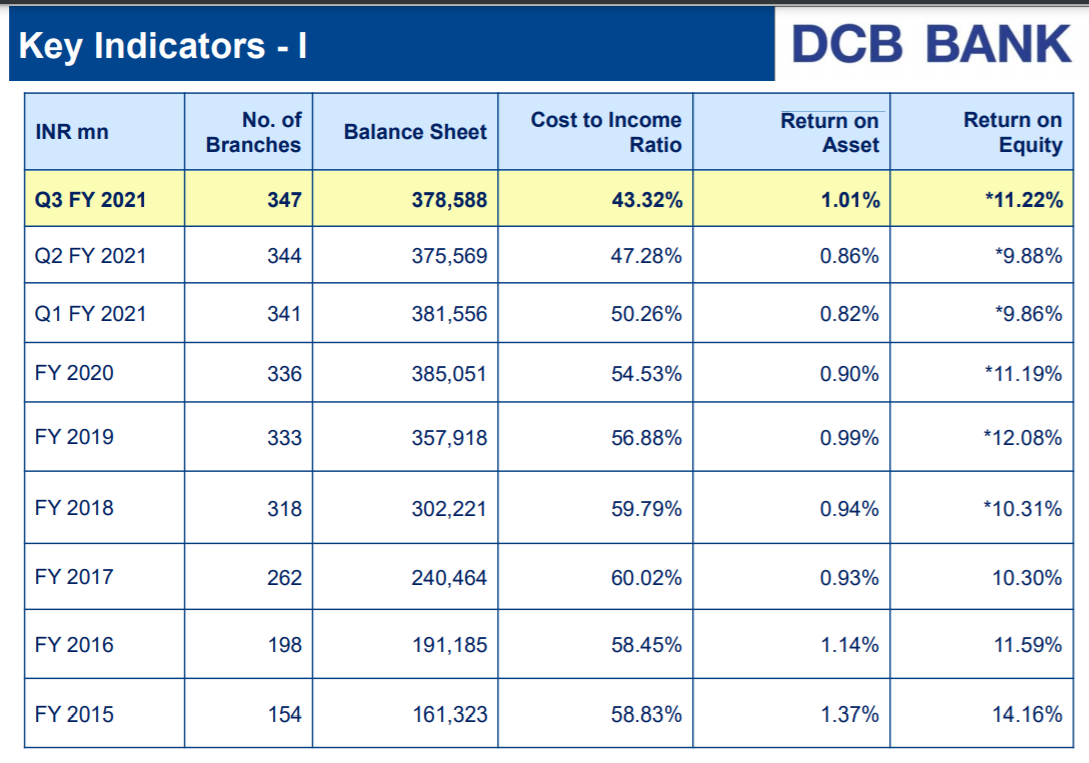

| Cost To Income Ratio | 40.52% | 47.00% | 54.47% | 36.10% | 43.32% | 79.20% |

| Price / Earnings | 25.33 | 36.11 | 27.79 | 10.61 | 82.00 | |

| Price / Book | 3.43 | 5.75 | 4.84 | 1.01 | 2.27 | |

| RoE | 9.46% | 13.67% | 16.53% | 10.36% | 2.75% | |

| 3 Year Earnings Growth | 13.00% | 20.00% | 21.00% | 19% | N/A | |

| Market Capitalization | 421,639 | 386,503 | 852,989 | 3,465 | 34,864 | |

| Total Assets | 1,377,292 | 443,173 | 1,580,830 | 38,505 | 149,159 | |

| Book Value | 121,757 | 67,135 | 176,358 | 3,421 | 15,404 | |

| Leverage | 11 | 7 | 9 | 11 | 10 | |

| RoA | 1.13% | 2.22% | 2.14% | 0.88% | 0.28% |

Disc Invested Since April

4 Likes

DCB Bank trading below book value again. I feel the risk-reward from these levels is extremely favourable. It is trading at a significant discount to not only its peers (other reasonably efficient small banks), but also its own historical averages. This when most other good banks, large and small, are trading at close to or even above long term historical averages.

If the cyclical uptrend that everyone is expecting comes, the valuation can reset pretty quickly. Looks like one of those heads I win, tails I don’t lose much stories

6 Likes

In this interview https://economictimes.indiatimes.com/markets/expert-view/we-should-be-able-to-double-the-book-within-3-years-murali-m-natrajan-dcb-bank/articleshow/63895038.cms the management guided towards doubling the loan book by FY21, which they have not been able to achieve. Although it is most likely due to Covid, but should this be taken as a case of aggressive guidance?

3 Likes

I am new to DCB bank, was going through the latest investor presentation and the the CoF is 6.61%

How can they be competitive in the mortgage loans that make up 40%+ of their loan book? Bandhan bank with a much lower CoF said in the latest con-call that their affordable loan division(erstwhile gruh finance) is facing still competition from public sector banks. They operate in western india and must have overlap with the DCB bank customers. Wouldn’t be a big red flag as they would not be able to offer competitive rates to 40%+ of their loan book?

https://www.dcbbank.com/pdfs/Investor-Presentation-Q2-FY2020-21-31-Oct-2020.pdf

2 Likes