My position remain as my last disclosure. I hold only tracking quantity to access AGM, with no trade in last one year on this company.

On previous post, I did indicate that I generally like business generating cashflow rather than asset sale. While assets sale can cure credit profile for the company (which has large capex funded with debt and kind of operating losses due to not able to productively use new plant), in my opinion, the company would be interesting to look only when Dahej plant break even and fully utilised. This is my view and I may be wrong in future.

Any idea on the extent of damage caused by the fire in Nov 20. The company took an impairment hit of Rs 50crs on its books. This looks high compared to Rs 170cr spent on setting up the facility.

One of the two units of Dai-Ichi at Dahej was damaged which led to temporary shutdown of operations. The other unit was not damaged and is operational now

Recognized impairment of 49.32 cr. Out of this 43.26 cr was towards property plant and equipment, 5.81 cr towards inventory and .25 cr towards other expenses

Operating the other unit at full capacity and also outsourcing some production on job work basis until the re-installation of the damaged unit is complete in order to meet demand from customers

Yes, the topline has grown after a long gap and operating margins have improved too…may be gradually things are coming back for the company after having faced several challenges in past couple of years.

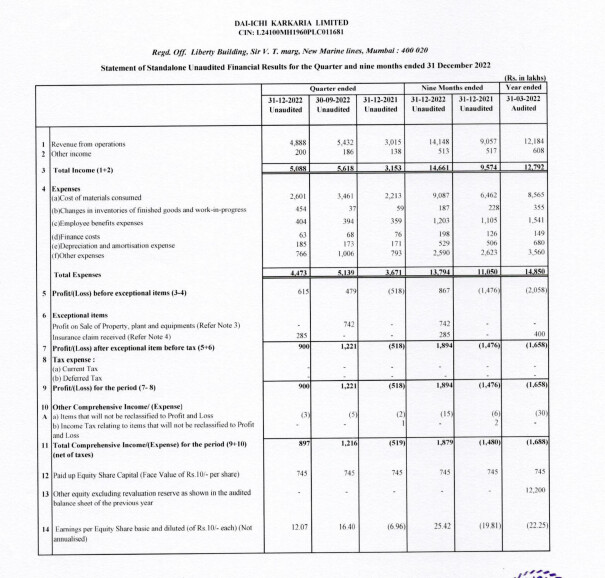

However, it is important to note that there is an other income of 7.42 Cr on the back of profit from sale of Pune land.

Regards,

Yogansh Jeswani

Disclosure: Tacking Position

Other Income is Just 2 Cr and that much amount is quite consistent in most of the quarters. I am considering excellent because company has reported positive EBIDTA for two quarters after reporting losses in many prev quarters.

Look at line item 6. It has got 2.85Cr as exceptional item. So total other income component is 4.85Cr which is significant.

Yes, the company is back to profit after several years of losses. I am just trying to point out that normalized profit would be much lower.

The other income component has been high especially in last 2 quarters but the good thing is they have begun reporting operating profit after a long time. To me it seems to be a company which went through temporary headwinds that have lasted quite a few years now.

Had they not moved out of Pune there was very little scope for growth. I am keenly watching this company but the management does not seem to interact with the shareholders.

I recently sent them an email requesting the management to share insights on business outlook, future growth plans etc through an investor presentation for the benefit of shareholders. I also enquired about the time taken to achieve full capacity utilization and the EBIDTA margins that they expect to sustain going forward.