Note from AGM on July 17 2017, based on discussion with Mrs S F Vakil in reply to queries of various shareholders. Please note that I have invested in the company and my views may be biased. There is also possibility of some misunderstanding at my end while writing notes. Future investor are expected to do there own due diligence.

Dahej Expansion: Dai Ichi is expecting spent Rs 168 Cr on Dahej Expansion. Of these nearly 60-70 Cr would be spent on Land and building/utilities while Balance Rs 100 Cr is on Equipment/Plant. The mean of finance for the project are from Internal accruals, Divestment of certain liquid investment and loan from Axis/HDFC Bank for 5 year tenure (Debt of around 100 Cr). The company aim to reduce interest cost minimum.

It has Three major plants being under implemtation for Dahej. The first one is for oilfield chemicals which is expected to commence production from November 2017. The second plant is Ehtoxylation (thanks @ananth for correcting my error in first draft) which supply to textile chemicals which is expected to commence from February 2018. Final plant which is multi purpose plants which would commence from March 2018. Full capacity would be achieved for first plant and second plant within 3-4 years, whiile the multipurpose plant is expected to reach 85-90% level within 18 months of commencement.

The company would also be shifting Kasarwadi Reactor (part of the plant is dated and would be discarded once Dahej plant in operational). Objective to move to Dahej to get into Pertroleum complex with continuous supply of Ethylene from RIL.

Dahej plant has imported technology for Ethoxylation which has been introduced first time in India (Technical support from Swiss company which is world leader in the area). The company expect real impact of Dahej plant to come from FY19 and FY20. It has three type of production processes. This advanced technology may help company in exports.

It plans to working with partner to get long term contract for enhaced production. The product strategy would be predominatly with Oil. However, the company intend to launch new products in Agri and Construction chemcials. Superplasticier are used in Bridges which need higher strength concrete. Over period, Chemcial share in total sales expected to increase from 7% currently to 10% in medium term and 15% in long term. The company supply also construction chemical to cement company which it expect to get good business. Oil chemicals include whole range of chemical to produce crude.

2-3 blocks are kept vaccant for future expansion. Currently 3 plant are implemetation and the company can can add two more plant in future depending on demand.

In FY19, total incremental depreciation and Interest charge would be Rs 10.5 Cr and Rs 9.5 Cr per annum respectively. Interest cost would reduce by Rs 2 cr per annum with repayment over 5 years.Depreciateion would be stable at Rs 10 Cr under SLM for next 5 years.

From April 2018, the company would have only two plants, Dahej and Kurkumbh (very small plant with 11-12 Cr sales). Kasrwadi plant would be shifted and would be closed over a period.

Total sales Rs 300 cr which would achived over 5 years. It inlcude Kasarwadi shifted capacity as well.

Land at Kasarwadi usage would be considered by Board at appropriate time. The company has not done valuation of land. This is freehold land. Karaswadi has around 15 Acres land.

Kurkumbh In past, it attempted to have JV with Foreign partner for Acrytronile which was not success. Hence, Kurkumbh could not reach to large scale. The company is open if it can get appropriate parnter supplying Acrytronile, it may consider JV in future, but nothing is currently under discussion. Kurkumbh Land is MIDC leashold land, with 9 acre land.

Crude Price Dai ichi gets two benefits from lower crude prices. Lower crude prices also reduce raw material as same being crude derived. Lower price of crude also make crude attractive resulting in higher volume vis competitive products.

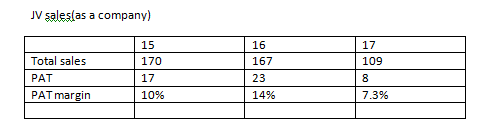

JV Nalco: JV in oilfield business servicing Oil production. The company has been working with Nalco for 5 years it was earlier with Becker. While the crude prices are under pressure for last couple of years, it may increase and stabilise over 3-4 years period to USD 70 levels. Despite crude price volatility, due to specialist process and product, Dai Ichi is relatively insulated from the volatility. During FY17, One the large customer (Probably Cairn), give contract for Oil chemicals to competitor which adversely impacted performance of the company. However, given the superior product quality, the company expect same business to come back in FY18. Shell and British Gas are other two major customers for Nalco JV. There were request about product mix sales between various group for the JV. The MD was reluctant to share this information as it was bound by confidentiality with JV partner. The company has won same tenders in past 16 years due to which the managment is optimistic to get business back. There are few chemical company which can considered to comeptitors.

JV buy raw material worth Rs 8 Cr from Dai Ichi Karkaria. Most of raw material are sourced from Nalco champion. Commoditised products are sourced from Large players.

Process: Global player like Crane invite worldwide tender. Tehcnical evaluation is promient parameter and then they are compared on price. Indian refining player generally give more wieghtage to price.

Wage settlement: Majority workers have accepted. Some has not accepted and matter is under Supreme Court. Over a period, many workers have retired which reduce work force size to less than 50. As per MD, the company is exempted from Union activities in case no of workers are lower than 50, which is now being the case. Hence, do not see major issue with respect to legal suit in Supereme court. Salary in P&L provide for all wage related laiblities.

Other discussion points

The company is moving to SAP along with GST from July 2017 which has resulted in increased efforts for the company. Overall GST is good for the sector.

Digitalisation of the company would be managed by MD’s daughter Ms Meher.

The company does not have any accident in past histrory. The company has undertaken safety audit.

From FY18, Sales of Nalco JV would be added only profit share would be added in line with Indi AS.

The company is fighting two cases, one for Octroi and Wage suit which resulted in higher legal charges.

The worli peropery is currently used by company as the current place was not sufficient with increased activities. the rent were also not good. so the company using its CJ Tower property as its office.

Concentration from Oil chemical is high. The company would try to diversify from construction and agriculture sector.

The company has rectruited 2-3 people which would be working from Dahej and focus would be to develop new products.

The new plant has flexiblity to change product mix. The company can increase paint related products. In case of textile chemical where it is not remunerative, the company may slowly change product mix in favour of other products.

FY18, sales projected is around Rs 160 Cr (from Karaswadi plant with limited contribution from Dahej). In FY19, Kasarwadi would be close while Dahej would increase utilisation, so expect Rs 170 Cr sales. The estimate are conservative considering teething problem and also time taken to develop new market and customer. Hence, the company is conservative in project.