Earnings include high level of other income - is that the JV PAT? Perhaps, that is why it seems to perk up in the second quarter when dividend is paid?

1 Like

Yes. It does include high other income. Yearly Rentals is Rs 1.44cr (As per AR FY15). Since last 2 years performance is largely coming from JV (Champion Dai Ichi Technologies Ltd). PAT from JV went up from Rs 7.5cr in FY14 to Rs 17.8cr in FY15. Other Income in Q2 FY15 was also high at Rs 3.8cr and Q2 FY16 at Rs 5.9cr (so it does seem like dividend paid).

However, standalone performance of the company is picking up nicely. EBIDTA (Excluding other income) stands at 13.5% compared to 8.3% and 6.6% in FY15 & FY14 respectively. In H1FY16, it has done EBIDTA (excluding other income) of Rs 8cr (almost same as FY15).

If standalone numbers are sustainable along with clean balance sheet & very good JV performance, Dai Ichi looks interesting.

Further clarity on capex would be useful. Company has applied for EC. EIA is available online.

Disc - Invested.

1 Like

Can anyone elaborate on the potential of Champion, where it is used and who are its customers (and maybe elaborate on sustainability of it)?

The whole fortune of Dai-ichi sustainable wealth creation rests on the JV - and essentially Champion. All these numbers are too backward looking - I don’t think anyone can take a decent position based on these past numbers or whatever the RoE/RoCE number is.

I tried looking this Champion up, but very little public info is available. Need to have a Oil/Gas industry contact to understand the potential.

1 Like

In my notes after AGM (listed in same thread on July 2015 period on same thread), I did touch upon business of Champion. They provide chemicals to Indian crude oil exploration. The JV can not exports. So income growth is directly linked to crude volume. Crain and ONGC are main customer of the company as per memory. For more details, read my previous note.

Having said that, if we can get some more understanding from industry insider. It would be benefiting all of us to understand the business.

2 Likes

Try looking up NALCOCHAMPION …its a ecolab group company …world leaders “who partner in producing nearly 40 percent of the world’s oil every single day. That’s more than 35 million barrels daily”

Hope this helps

1 Like

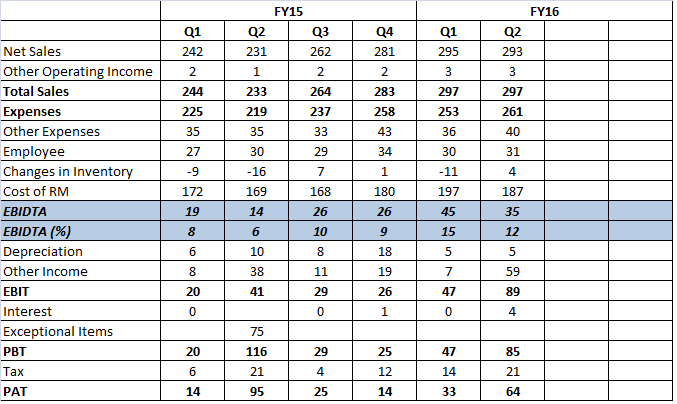

Moderate result by Dai-Ichi Karkaria. Topline growth 3% YOY (expected due to decline in crude price) and net profit growth of 14% YOY.

Sequential profit is showing marginal drop. Opertional profit in Sep 2015 quarter was Rs 3.01 Cr vis a vis Rs 2.94 Cr in December 2015 quarter.

Post Opertional profit, there is has exceptional income hence results are not comparable to sequential.

YOY, result shown marginal growth at net level due to following reasons:

- Decline in Non-Op income from Rs 1.12 cr Q3FY15 to Rs .95 Cr in Q3FY16

- Spurt in Tax from Rs .42 cr in Q3FY15 to Rs 1.03 Cr in Q3FY16.

Overall, no major growth, but quality of income has improved (as shown with lower dependence on non-op income and higher tax payment). Further, March quarter results would be key as we would also get result of Dai-Ichi Champion consolidated (provided once in 12 months).

Overall moderate (not great) results in my opinion.

Note: Hold and sold small quantity at Rs 530 in October 2015

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=3454dcb2-2545-4d6b-80ff-327fb9c34728

2 Likes

Hi can someone please help me understand why low oil price will not impact this business(as mentioned in the thread) since the application of their products is mainly for that field.

As far as raw materials is concerned, most specialty chemical companies follow cost plus model and hence I feel it wont lead to margin improvement.

Disc:not invested

Over last few quarters, while there has decline in crude/crude derive product prices, Operating margin of Dai Ichi have increased significantly as against decline in crude price.

http://www.screener.in/company/526821/

As we can observe, operating profit margin for Dai-Ichi has increased from 6.02% in Sep 2014 quarter to 12.74% in December 2015 quarter. Partially, the margin increase indicate lower crude price and cost+margin structure of pricing, Absolute operating profit has gone up from Rs 1.40 Cr in Sep 2014 (with assumption that same being conversion margin on crude cost) to Rs 3.46 Cr in Dec 2015. So in my understanding, nearly 2.06 Cr growth in operating margin would be due to higher capacity utilisation, improved product mix and increase in realisation. This would be not one time and would be sustainable in my opinion.

Discl: I have investment in the company and has traded in company in past 3 months and hence may be biased.

2 Likes

I was comparing it to a product sold by vinati called atbs which is used in oil recovery… They have mentioned that the volumes have gone down due to slow down in the sector…will need to dig deeper why this company is not affected

1 Like

Vinati product has application in shale gas exploration. With crude at around usd 40, shale gas players would have some issue. To my understanding, Dai ichi product are mainly for refining and traditional crude exploration. Also, that account for around 25-30 of sales with other enduse being textile, construction etc. So in my opinion, crude price would not have major negative impact on Dai ichi standalone results . Champion Dai ich JV performance may see negative impact.

1 Like

Dai Ichi Karkaria has received EC Clearance for Dahej Plant.

Looks like a positive trigger for rerating.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=d0b176e3-6736-43dc-a8c9-3eb4212ea7bc

2 Likes

While the approval was expected in October 2015 as indicated in AGM, what I like is better late then never. The increase in Crude price from USD 28- USD 45 per barel in last 3 months also assist domestic crude production growth and hence improving outlook of Champion JV. When crude price declined below $ 30, the Indian production of crude also show marginal growth. Demand for Champion Dai Ichi is directly linked to Indian domestic crude production.

Announcement of Q4 result in May would be key event to watchout for. The company declared Champion Dai Ichi consolidated numbers only in March quarter. Hence, standalone+consolidated would decide way forward for Dai Ichi in my opinion

2 Likes

http://www.bseindia.com/xml-data/corpfiling/AttachHis/E6A2FF7B_A2E3_4610_87C5_60A95FA910D1_173344.pdf

FY 16- Standalone profit went up 73% on standalone level(15.5 vs 9cr…without 7.45 cr)… last year numbers included exceptional item of 7.45cr profit from sale of inogent…Consol numbers (without exceptional income)…went up by 25% (22 cr vs 17.5cr)…Champion jv numbers looks down( 6.3cr vs 8.8cr …-29%)…crude prices now recovered to 50…and expected to be in the range of 35-65 (as Shale will not be able to pick up inline with mkt expectations with rising rates in US forcing yields higher…and outages MENA region along with low spare capacities to meet increased demand will keep mkt balanced…)…

Discl: Added small position to track -

1 Like

Dai Ichi Karkaria Result Analysis indicate some major decline in Other Non-operating income. FY16 Consolidated other income is only Rs 4.24 Cr as against Standalone non-op income of Rs 9.03 Cr. If we assume that consolidated number and standalone difference is Champion Dai Ichi number (as Champion is the only significant business which is consolidated), we get negative non-op income of Rs 4.79 Cr which might be due to some reclassification/ receipt of rent etc from Dai-Ichi from Champion.

On a positive note, total operating profit (Sales+ Op Other income- Raw material- Employee- Other expense) for Champion Shown improvement to Rs 16.22 Cr in FY16 as against Rs 13.73 Cr in FY 15.

Sale+ Op Other income+ Inventory Adj during FY16 for Champion is Rs 75.69 Cr as against Rs 76.64 Cr in FY15 (Decline of 4%)

Total operating exp (Raw material+Employee+Other exp) during FY 16 for Champion is Rs 59.47 Cr as against Rs 65.34 Cr during FY15.

So Operating profit for Champion in FY 16 is Rs 16.22 Cr (around 21.43% of Sales) as against Rs 13.30 Cr ( ~16.9%) in FY15.

There has been major drop in other non-op income between Standalone at Rs 9.03 Cr for FY16 while same is Rs 4.24 Cr for Consolidated in FY16. We need to get more understanding about this to get better perspective about Dai Ichi.

However at first glance, Champion Dai Ichi JV number does indicate improvement in operating margin despite lower sales growth.

3 Likes

Hi Dhiraj,

Have you gone through Annual Report FY16 ? Please share your thoughts.

Thanks.

Few Observations…

-

As you rightly pointed out operating performance of JV has improved, while topline has been flattish (this in face of wild fluctuation in crude).

-

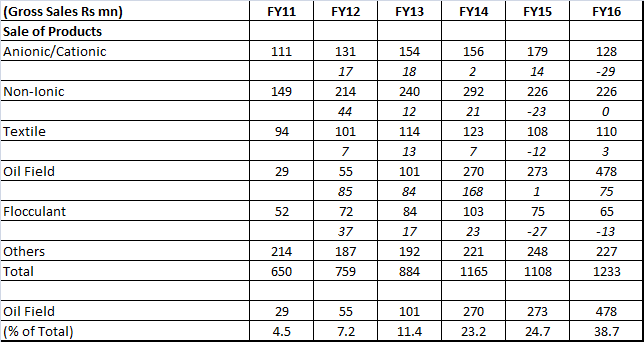

On Standalone numbers Oil field now accounts for 39% of sales in FY16 (from mere 5% in FY11). Other segment have been largely flat.

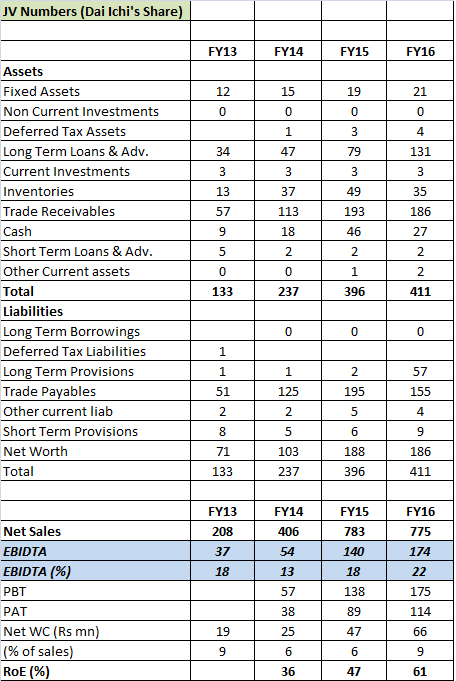

- JV business looks very asset light model with high RoE. Does sales of Rs 78cr on Rs 2 cr FA with PAT of Rs 11.4cr.

Disc - Invested.

3 Likes

Thanks for sharing input. Prima facie good development is stable dividend income from JV would strengthen the other income of the company.

Also, new capex in Dahej, would give more clarity about growth for next 3-4 years. Let us see how much is capex and funding requirement. I shall try to attend AGM to get answer on same.

On negative side, after 3 years of more then 50%, JV has stabilise on topline. Although expected, but even growth of 10% would have been much better then flat top line in my opinion.

I am out of station for next week, so would be able to revert only next week.

3 Likes

Tomorrow is AGM. Venue map given in annual report

Please let me know in case anyone has question to ask to management. Not sure whether would get chance. However, would try to get as much as information as possible.

I shall be attending AGM. Let me know in case any other member is attending.

3 Likes

Notes from AGM on August 4 2016, based on discussion with Mrs S F Vakil in reply to queries of shareholder. Please note that I have invested in the company and my views may be biased. There is also possibility of some misunderstanding at my end while writing notes. Investor are expected to do there own due diligence in case they intend to invest in the company

Abbreviation: Dai Ichi Karkaria (DIK), Nalco Dai Ichi (NDI)

Nalco has largest units in Jurong Island, Singapore. Why they source material from DIK?

Jurong Plant is Ethyxilisation (not sure about spelling) plant while they also need other specific chemical, which are sourced from DIK.

The FY16 margin of DIK and NDI are due to decline in crude prices? Are margins sustainable? Do need to pass on decline in input cost to customer?

While margin are sustainable, there are been increasing pressure from the oil explorer to demanding discount, Even after discount, during FY17 the company expect margin to remain in current range. The company’s supplier keep 25-30% of benefit of decline in price to itself and pass on balance benefit to the company, Similarly, DIK also attempt to keep 25-30% of lower pass benefit and pass on balance to the customer. Hence margin are intact.

What has been volume growth in NDI? Growth in NDI was almost flat during FY16.

NDI budget for FY17 is to reach sales of Rs 200 cr. Given the tough market, NDI may face challenge to achieve same.

NDI would not export chemcial and would service only Indian oil exploration market. Currently BG and Cairn are two large customer of NDI.

DIK faced some problem in polyacramide plant at Kumkumbh. Any JV explored in that plant?

Poluacramide plant stared with Japanese technology. The peer have capacity of around 30,000 tpa while DIK has small scale of operation with around 600-700 tpa (a kind of pilot plant, it started as a pilot plant). DIK also hae issue of access of RM. So in case it get a partner who can offer RM access, it may consider JV in future.

DIK sales in construction chemical has been slowed down? What is share of same.

The segment wise sale of DIK was under:

Oil 45%

Construction: 10-12%

Textile: 25%

Paint, Metal cleaning etc: Balance share

Construction chemical demand is expected to pick up from Q2/Q3 FY17.

Dahej Plant:

Dahej plant shall be on stream from Sep 17 with cushion of couple of month. So realistically start by December 17. DIK would spent further Rs 100 Cr by Sep 17. The company would use Rs 40 Cr of investment and balance would arrange term loan. Nearly 50% of capacity at Dahej plant would be for oil. The management when asked about Oil becoming obsolete, replied that they do not see same happening at least for a decade. Balance 50% of capacity of Dahej would be for other applications. DIK also want to increase products in personal care industry as that is stable high growth end use sector from Dahej plant for which research is underway. Dahej would be mutlipurpose plant (expect for oil chemicals capacity), which can easily be migrated to other end uses. DIK has competitive advantage of being in India which provide access to input at cheapest cost. After total capex of Rs 170 Cr in Dahej plant, DIK would expect peak turnover of Rs 300 Cr which would be achieved from 3-4 years of commencement of Dahej plant.

In Dahej, oil chemical capacity is expected to be around 1.000 tonnes per month. Margin from oil chemical business would continue to remain at FY16 levels. After Dahej, within 3-4 years, the company would achieve sales of 300-400 Cr which would have better margin due to higher scale. Further, any further development/value addition capex would be marginal after the greenfield set up of Dahej is operational.

DIK Sales and profit guidance

Conservatively, the company expect to reach sale of Rs 130-140 Cr for DIK. Exports would continue to drive growth in oil chemicals mainly in Middle East and Iran market. The company has almost fully utilied capacity and scope for growth is only from oil related chemicals. So oil chemical would continue drive

growth till Dahej plant is operational. The margin would be remaining at same level as for FY16 (assuming input cost remain stable at current level)

NID terms with Cairn are finalised?

NID contact with Crairn extended thrice. The contract is expected to be finalised by November 2016.

Why there has been service tax interest being paid?

The company has provided for service tax interest for some dispute about rent received and not paid in cash. There has been litigation about same and in case DIK gets favourable judgement it would reverse the provision.

Karaswadi Land:

The maharashtra government has taken back tranche of Land for Road expansion. DIK has filed objection as the compensation received from the government is lower than the prevailing market price. DIK is aware of residential and commercial development in surrounding area of Karaswadi and may take call after considering various factor about land development. Currently, the plant is operational on the site. There was a suggestion by shareholder to monetise the property to fund Dahej expansion. The management said they would consider it but did not give any commitment on same.

Relationship between Nalco and Dai Ichi (Why Nalco need Dai Ichi):

Dai Ichi research skill, local manufacturing and logistic are key contribution to JV which is why Nalco, despite being large chemical company, not going on its own.

In past, Becker has partnered with Dai Ichi and subsequently parted from Dai Ichi. It faced major challenge of logistic to service to the customer and still facing problem in India.

Government initiative of Make in India also give Dai Ichi being a local manufacturer competitive advantage vis a global players. So Lower cost, access to raw material, logistic support, local manufacturing and chemical skills are key contribution from Dai Ichi to JV partner and hence would continue to remain key partner for Nalco India.

Beside JV, Nalco also source many oil chemicals from Dai Ichi. It provide specification and DIK develop product as per specification. DIK also leverage of its product development capacity has increasing developing new customer in Middle East and Iran and optimistic about future growth.

Further, despite global competitive market, Nalco has used service of DIK to provide it customise products for non-NID products. DIK has also pioneered certain product development in oil chemicals based on customer request and specification which would work as entry barrier for competitor and also for customer as switching over would not be smoother on availability.

Does the company margin expansion is driven by increase share of oil chemical business?

The increase in margin was partly due to higher margin in Oil chemical business and partly due to scale of operations. Typical textile chemical demand is around 2-3 tonnes while Oil chemical supply is generally on container basis. Hence, the margin of DIK has increased with higher share of Oil chemicals. Currently, Oil Chemical capacity is around 600 tonnes of per month (with current production 400 tonnes per month, expected to increase to 450-500 per month in couple of months). At 600 tpm, the company would have monthly sales of around Rs 12 Cr (so annualised sales of 140 Cr which would be peak level without Dahej).

Discl: I continue to hold share in DIK and no change in my position in last 30 days.

6 Likes

Are you still tracking it? If yes, could you please share the updates on the progress of the construction of Dahej plant. What is the impact of fall in oil prices? The third quarter pat is significantly lower compared to the first & second quarter, any specific reason you know of?

I continue to hold my share in Dai Ichi. No update from Dahej on my side. Anyway the management generally meets only in AGM, at least as per my knowledge. One can evaluate risk profile and other opportunities and take appropriate call.