@jigar_punamiya The company’s main focus was tendering business. In absence of tender business there will be a sales gap. The growth in sales we are seeing right now is because of some tender wins. Some of them are for log term like the tender for South Africa business is for supply of next 3 years. The supply or condoms “green Love” to Safeware is for 10 years starting from 2014. The gap which you see is lack of tender sales in 2013-14.

1 Like

the AGM was pretty good… the future of the company looks good…they r operating in a very large market with less competition & any increase in demand will result in additional revenues for the company… some board members have expressed views regarding hedging my personal view is company should leave dollar exposure unhedged as many companies have incurred huge losses trying to have views on currency markets…& hedging can be done for 3 months revenue but what after that ?? … rubber price fall will surely help…

2 Likes

Linking to my other post instead of double posting:

Cupid results were music to my ears after a rather subdued results from my other holdings:

Salient points:

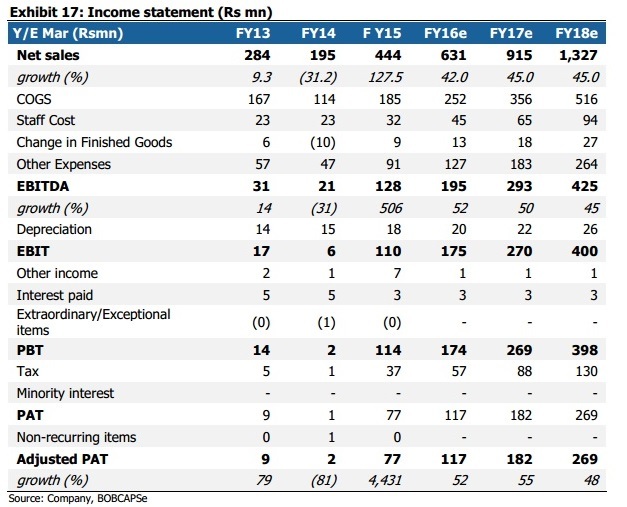

- Revenue growth: 57% YoY and 23% QoQ.

- Profit growth: 140% YoY and 30% QoQ.

- All Pledged shared released.

- Interim dividend of 1 INR per share declared.

- EPS doubled H1 FY16 vs. H1 FY15.

On H1 EPS of 6.41 (FULL year FY 15 EPS is 6.93),

I predict, H2 FY16 to be better than H1 and full year EPS could be around 16-18. I think the full quarterly effect of the new large order may not have been reflected in this quarter but over the year the revenue growth will further catch up.

Quantitative and Qualitative points have both improved and the story could be on the way becoming a secular one.

10 Likes

Amazing set of numbers from Cupid! Apart from the EPS growth, the return ratios going forward is likely to further re-rate the stock. The expected interim dividend too came about. The good part is that the mgt. is open n receptive to share holder inputs. There is also a possibility of the mgt. giving an interim div with every quarterly result from next year.

Cupid has truly warmed the hearts of its share holders! The stock looks to be headed higher.

4 Likes

Chinese government scrapping one child policy would have shrunk the global condom market by quite a bit. There may not be any direct impact on companies like Cupid but I think condom suppliers would become more competitive now.

I agree, really great set of results. The annualised RoCE based on EBIT today is c.58% post-tax, which definitely warrants a re-rating. The interim dividend and strong cash generation also point towards a solid business. The dispatch for the SA contract only started mid-quarter, so Dec will also see some QoQ growth.

Also agree with possibility of further dividend payout.

Do you have any update on current order book and commencing of the lubes business? The latter should help build further revenue trajectory going forward.

2 Likes

Guys I have been tracking this stock for a while. I have been waiting for a good price to enter. However , it is unlikely that we will see a steep correction in this stock . How would you evaluate the stock from a new entrants perspective based on current valuations. My risk appetite is higher than average

Would really appreciate your thoughts

Current year earning should be around 15… on a reasonable PE of 25, it should be trading around 375. The stock looks like undervalued after Q2 result.

2 Likes

The story is getting better day by day !

Looks a safe bet now

disc : tracking position

1 Like

@sagararya At this time i donot see any buying opportunity for multibagger returns atleast 10X in this stock.

- If you see the BoB report on Cupid(Attached screenshot), It says it will have around 26 cr profit(Esti). So you can derive the chart of future projection of profit. As per my view the sales are going to get stagnant after 3-4 years.

2 . The management is saying they will issue dividend every quarter that means the company is not going to invest in further expansion - It is Global tender business so the future orders depend on winning the tenders, Cupid has stronghold in South Africa vs the competitor has in South America(Brazil). Again they may be having territory restriction if you see the news for winning bids in last few years.

- Considering the PE multiple of 30 at that time also, we an get the MCAP of 1000cr and share price at around 1000 . If the company is not able to deliver good number of sales then the share price may also get stagnant.

- You can see the story and stock movement of its closest competitor which is in US. The share price got halved when they announced stopping of dividend payment every quarter

Disc: Not invested. My view may be biased for not to buy the stock at current price. I reserve the right to be wrong.

1 Like

Thanks @nityanandparab. I agree with you. I do not see 10x returns from this stock especially because of the consumers they cater to. As far as my understanding goes, their main clients are NGOs and other Government organizations which is risky and difficult to verify. How prevalent are they in the retail market? I saw they sell on Amazon and Flipkart but they do not focus much on the domestic market which they claim is the largest market. Why have they not been advertising their brand? I think they can position this product very well in the domestic market by advertising. For eg. Emami positioned fair and handsome perfectly and took away the market. I am sure there is not much difference between Fair and Lovely and Fair and Handsome. They just advertised brilliantly. I dont see any advertisements for female condoms and I believe the company that starts advertising first will occupy the consumers mindshare.

Honestly, 3-4x over a period of 4 years is good enough return for me. But I believe, that there can be a lot more potential for growth. I will arrange a meeting with the management and would like to understand his thoughts.

4 Likes

Guys…I was looking at how USFDA and UNFPA approvals are granted to condom manufacturers. Find the link below

This says that the product is run through many clinical trials post which the approvals are granted. Now, this doesnt seem to be a high entry barrier. Also, in the link given below, V.A wow female condom has the lowest price / unit. If they get the necessary approvals, orders for Cupid can dry up. Hence , it is vital for them to enter the retail market. I think the only way this business can grow and command a higher multiple is by being more consumer facing. Looks good for short/medium term. Long term , I am not too sure

1 Like

VA wow price is for 35 million units. where as Cupid price is for 1 million units only. Obviously price will come down with increase in quantity. Check retail price, VA wow price is more than Cupids price

2 Likes

Management interview on CNBC18…

I liked the confidence of the Mr Omprakash Garg. He is hopeful of getting more orders in future & to maintain revenue run rate for several qtrs…

Disc- Invested from lower levels… also added after results

2 Likes

As per him the minimum guidance of revenues this year is about 60cr. The south African order: the shipment started in august so not fully reflected in this quarter. Out of total about 9cr was due to that.

As per CNBC interview, in Q3, the full impact of SA order will be min 9 Cr, so sales in Q3 could be in excess of 22 Cr, which is close to 100 % growth.

With operating leverage and this being high margin order of female condom, PAT can have a super normal growth , it may be close to 6 Cr.

The company and stock seems to be in sweet spot for next few quarters !

The stock is still under-owned and and not fully discovered and this will also benefit it from limited downside as well

Disc : have tracking investment

2 Likes

@sinha 124,

Q2 revenue includes 7 cr from SA order. so, incremental growth of 2 cr is left for Q3.

Read on website that Zimbabawe government is studying trials with female condoms.

Moreover management is exploring markets in South America and Europe.