As highlighted earlier , i think what cupid has is a good product in which it has managed to develop expertise at a technical level, however what it lacks ( in my view) is marketing it properly.

The govt based revenue stream is an optionality, but they need to create a market at a consumer facing level. That ofc is a tough tough job entailing steep costs and giving up of fat margins that they enjoy on govt orders, but it needs to be done.

There is also the question of raw material volatility which is significant in this line of business and that has to be mitigated. I like Cupid for what it has managed to achieve but they need a good ad agency and some gumption to grow their product.

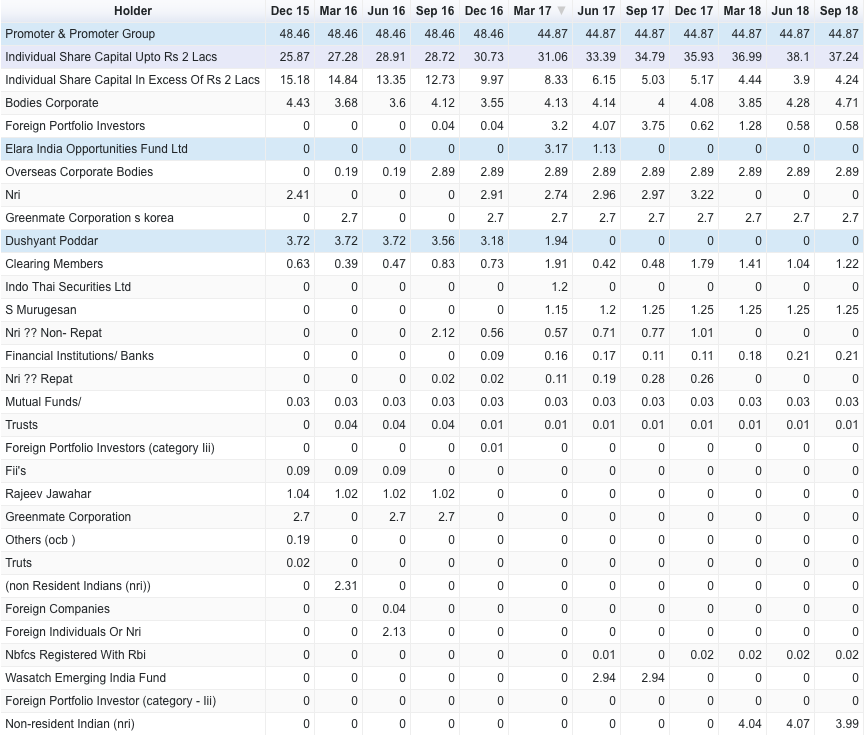

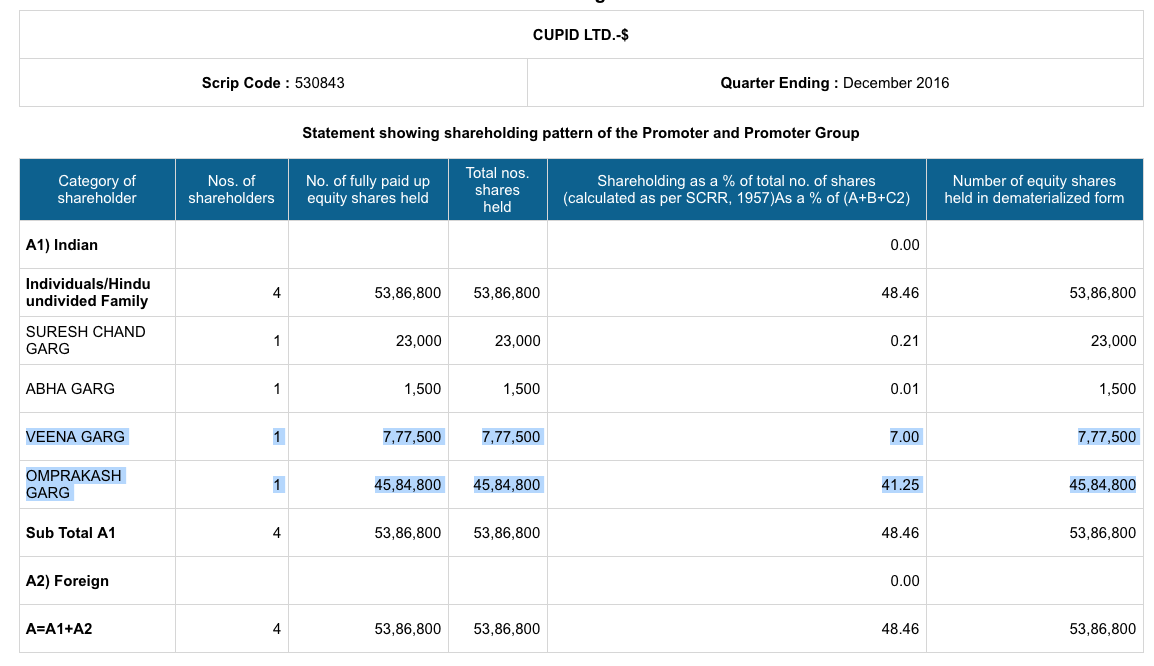

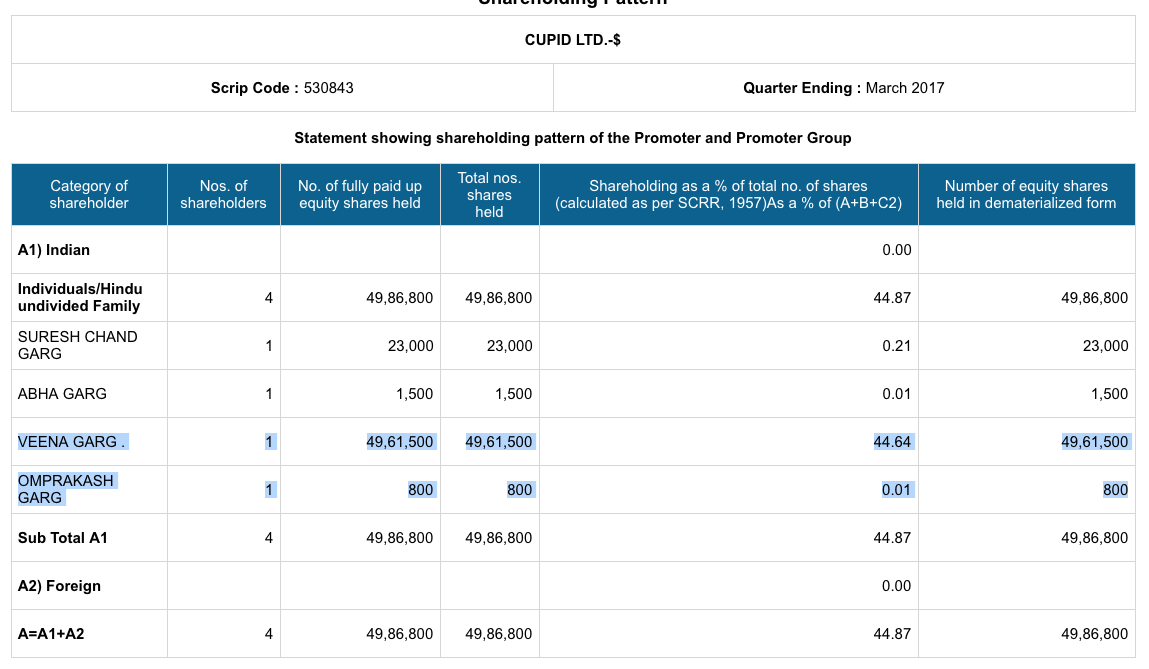

Promoter holding in Dec '16 was 48.46% and in Mar '17 was 44.87%. During this period Mr. Omprakash Garg transferred almost all his holdings (41.84 lakh shares) to Veena Garg and also sold 4 lakh shares to Elara India Opportunities Fund.

It must not have looked too bad as the shares were transferred to his wife and the other portion was picked up by an institutional investor. However, considering this was done in an euphoric bull market, I suspect the idea was to dispose off this 4 lakh shares at valuations the promoter considered excessive. End of March '17, Cupid was trading at 330.

This is precisely what happened as well because Elara sold 2/3rds in the next quarter and the rest in the quarter after that. This I think is disposal on behalf of the promoter. I know most will see nothing wrong with it, as there is nothing illegal in it. But if this was done by promoter directly through market transactions, it would have raised eyebrows immediately. Doing it this way was the in-thing last year as promoters of several companies, especially microcaps offloaded through similar means on unsuspecting retail.

See how the retail shareholding has moved in this company for eg. from 25% in Dec '15 to 37% in the recent quarter as big fish like Dushyant Poddar and Promoter/Elara offloaded heavy chunks onto them. That is a clear sign of distribution I think.

The company may have a decent business on its hands but it helps to understand what promoters themselves think of their business outside of what they say in interviews and concalls and nothing speaks more than actions like these.

The promoter himself is going to sever ties with the business soon and if I’m not wrong, mentioned in one of the earlier Concalls that he’s just in as an Acting CEO until they find a new one. Once again, if I’m not wrong, he has plans of settling in the US once that’s done (I can’t remember where I read this, but I’m sure I did).

In any other context, it would make sense to raise a question to the CEO regarding this. In this context, I don’t think it does. Heck, even if the CEO sold 10% more, I don’t think it would matter.

By the way, Mr. Garg is very honest and forthcoming. You should either listen to one or several of his Concalls or ask someone who’s visited the AGM in person.

In the earnings presentation, they’ve mentioned that theyre not going to be equity partners in the JV. The concall will need to throw more light especially becoz the JV was being touted as a future move to corner revenue.

I’m tempted to strike down the valuations from 190 cum bonus to around maybe 120 ex bonus assuming zero growth.

If they meet the expected order completion for H2 of Rs. 51 Cr, even assuming this Quarter’s low Net Margins (20%), that’s a bottom-line of Rs. 10.20 for H2, making the yearly Net Profit Rs. 19.02 or about 12% Growth YoY. Of course, if being the operative statement.

Since fortnight r so, company is pushing ads about female comdom religiously once in a week. Looks like B2C is catching up. Things vl take time 2 think, crystallize n implement. Lets see 6 months down d line, how this change in strategy is working out.

The following are required to happen in my opinion:

Mr. Garg should sell out to a strategic partner and remain on board as a mentor given his age, physical challenges and no family succession. Shareholders should demand a timeline.

Fresh young blood, dynamic CEO, CBDO and well connected directors to be installed.

Tap fiis and mfs by issuing more capital and expand capacity. The addressable opportunities are huge in this business.

Alternatively get acquired by a bigger shark. Mr. Garg is mostly in the US where he can scout for a strategic buyer like the one that edged out Cupid in the tender this time.

My analysis was mistaken. I assumed that the 100 odd crores order is the beginning of a new growth trajectery. Mr. Garg had mentioned that 20% cagr will be there for several quarters. Plus the balance sheet was good, PE wasn’t that high. At that point, it was a buy. But Basant Maheshwari exited. Clearly second level thinking which I couldn’t then see.

Any thoughts?

We as shareholders should individually write to push for the above to enhance market value. Else at this rate, the company deserves a market cap of ~150 crores {(14 cr earning power x 8 PE for zero growth but good npm and roe) plus 28 crores for the balance sheet ( this is a random number from me to round off market cap)}.

Not too sure about the amount of ‘second level’ thinking here. In hindsight (and even otherwise) it was clear when this stock moved from ‘value’ to ‘growth’. Even on this forum, it seems that several people exited after Cupid’s initial growth spurt on the basis of a lack of clarity about future growth. On other forums too, questions about future growth and lack of promotor ambition have been key sticking points.

I for one grossly underestimated the execution risk when I bought in mid-2017, thinking that new product launches would quickly pick up. I ignored the thought that the ‘old’ promoter might have just had enough action for one life time already.

I agree that we shareholders need to organise and send a message to management, but the key question is: will they listen? If Yes Bank can find a CEO in 3 months, something is clearly wrong with Cupid for it to have taken 1+ years.

Old age isn’t the issue, how old are Buffett n Munger… Physical challenges and succession are.

Order book grows with time. It isn’t that lack of orders prompted exits by the gurus. In b2b, orders flow in with time and mainly connections more than quality. U think African tender is based on quality? That too government order?

I think the gurus saw then, what is worrying me today.

The relevant question is: how do we avoid such pitalls in future?

I bought at 190 odd levels cum bonus taking that as a fair value. But it seems to me that 190 too is a premium price.

Shareholders should ask and write tough questions respecting this management with integrity. Whether they listen or not is another issue