Q2 Earnings call Transcript:

Anyone still watching this company? FY20 Q3 was a decent performance but stock price does not reflect that (even before corona virus impact). Any specific reasons ailing the stock.

Numbers are not too bad (except the prudent provisioning)

Good to see company being cautious in new lending at this period of uncertainty.

Dividend 2.5 Rupee declared

Disclosure : Invested

Hello everyone

I have been reading up a lot on the company recently. I couldn’t reconcile myself to why would this company be attractive to a real estate borrower building a group housing society. The company claims that it is able to get 2.5 times collateral for such loans. And yet the company offer such loans at a high irr as compared to banks.

Doesn’t it make more sense for the borrower to instead wait for a few more days or weeks and then get a loan from a bank for a few percentage points lower than what you would get from an NBFC?

Disclosure: invested

1 Like

This is the first time I’m writing on this forum. Read all the 144 replies so far.

I’m a fan of CSL’s Annual Reports and their original content. I’ve seen a few ARs that use generic templates but CSL has been original in detailing the short term headwinds they face.

Sometimes, I wonder if they’re playing to the biases of investors, as they also come from the same investing business being also run by all CAs.

In one post, I saw somebody mention internal accruals as an attractive term for investors and hence managements use them.

Been a fan of how this management has been so restrained and kept their word for all of 5 years, ever since they entered the lending business.

I see it as a positive sign that they don’t leverage at higher rates. The reason I’m here today is because just got their Annual Reports emailed and reading.

I also liked Rohit Gupta’s remarks in their last ConCall. Q1 was decent considering we had the second wave and two full months of lockdowns, of course with their near-50% PAT margins.

Have any VP boarders read the Annual Reports yet? Would like to know the current investment status of expert VP members on this stock and your latest views on the stock too.

Since the company fits itself nicely into most of the evaluation metrics we look for except very few of them, I’m invested and loving it - both the quantitative and qualitative aspects of the company and the management.

Not to forget the moat they’ve been building, their ability to cleverly understand the market, where they have an edge and only bet on areas where the odds are heavily stacked in their favor. This is as Munger as it could get, the one most of us look up to.

This is the first company I’m being so enthusiastic enough to comment on in this forum. I’m sure there may be other companies too.

By the way, would like to know the current investment status and views of expert long term investors and boarders on this stock.

Also, are there any recent developments we should take note of? Touch wood.

By the way, I was also expecting some commentary on how they did well during both the first and the second waves and kept their good performance to date for over five years. Please pour in your views. Thank you.

3 Likes

There’s has been a significant move in the price and a reply has been awaited by the exchange?

It felt good when it hit UC up to Rs. 172.65 last week. Besides the strengths, I think the stock or its underlying business also has some weakness to justify overvaluations.

Much depends on this quarter’s results. The management has been good with their talks even in the last Concall transcript.

I think economic revival may mean some good repayment. However, we have to wait for much to unfold in this stock.

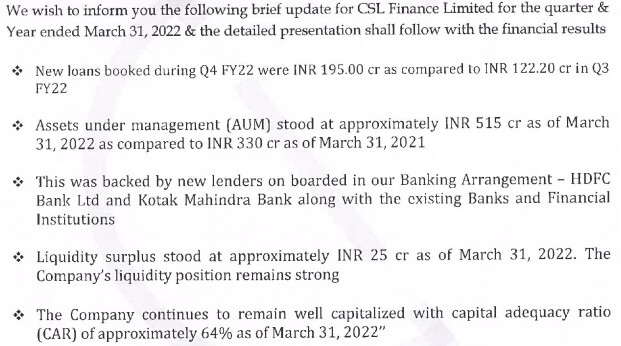

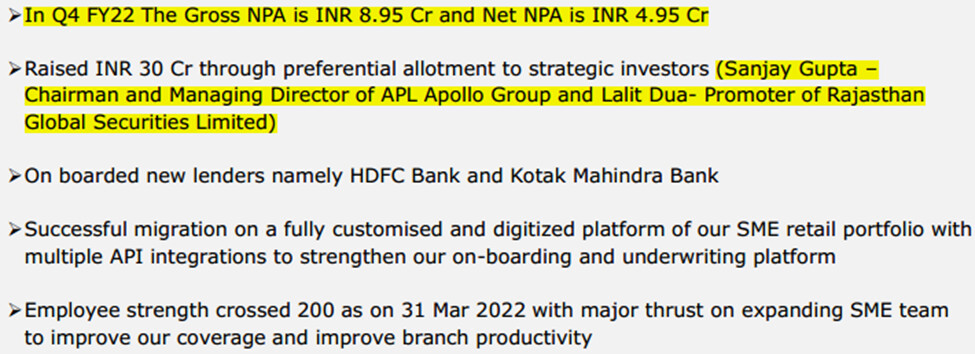

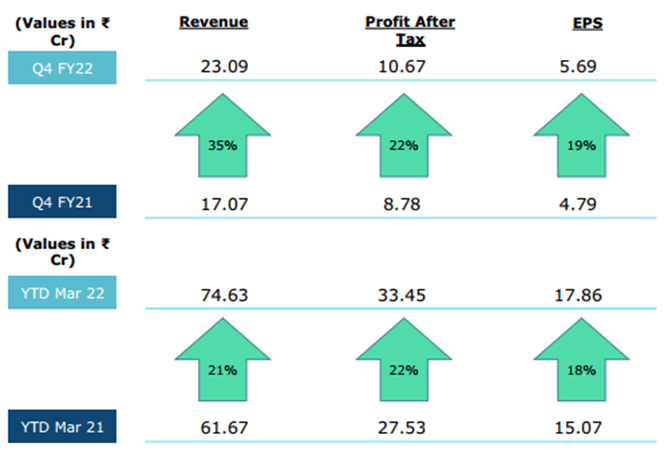

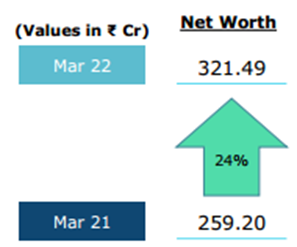

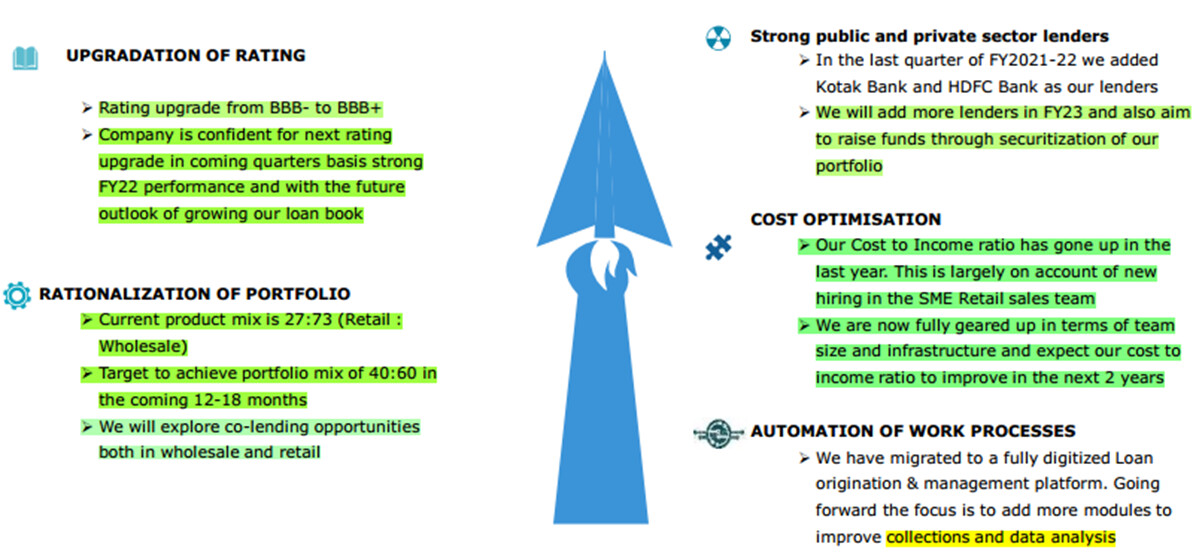

Business Update as of 31.03.2022

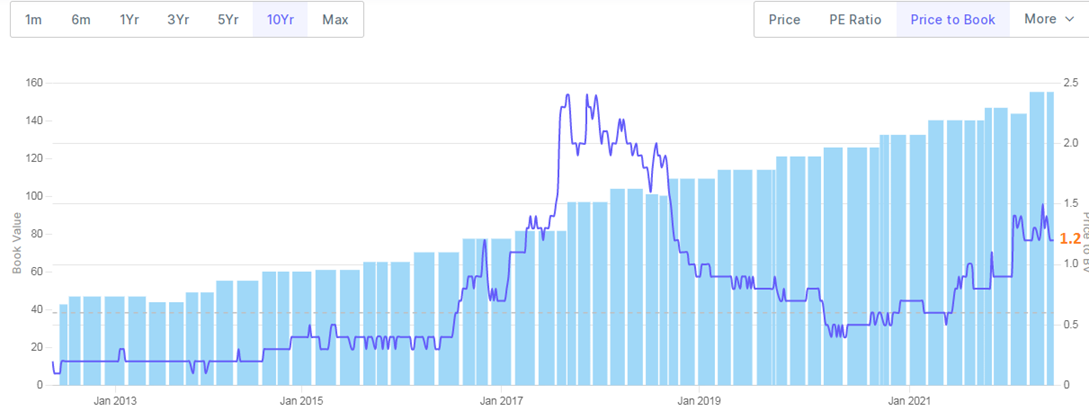

Still deeply undervalued

Invested since February last year.

3 Likes

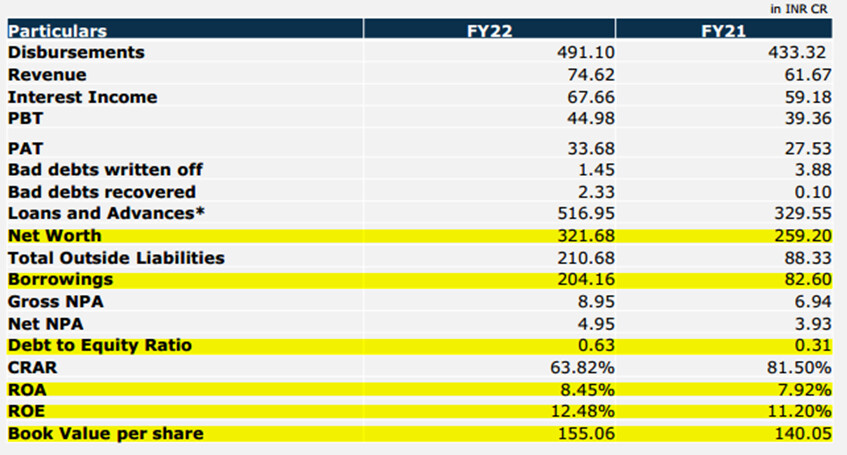

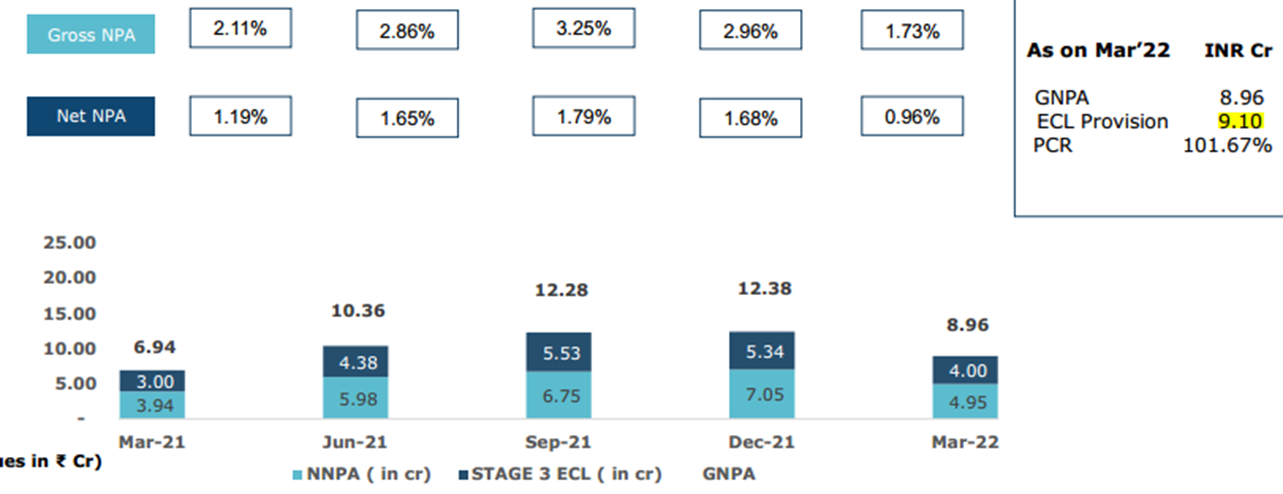

Good set of numbers from Q4FY22

| Q4FY22 | Q3FY22 | Q2FY22 | Q1FY22 | Q4FY21 | Q3FY21 | |

|---|---|---|---|---|---|---|

| GNPA | 8.95 | 12.38 | 12.27 | 10.36 | 6.94 | 5.10 |

| Provision | 9.10 | 9.41 | 9.21 | 8.70 | 7.84 | 7.52 |

Valuation:

2 Likes

Hi Folks, anyone tracking this company? FY24 growth has been strong and management is indicating for strong growth as economy is picking up. Promoters are also buying shares from open market.

Thanks

3 Likes

Promoters have knowledge about the local real estate market in Noida and Delhi, but beyond this they are not able to expand so far, their retail book is not expanding, branch network in other states is not expanding like other NBFCs. They are good in wholesale but retial section the growth is not good.

Was invested, kindly do your deligence …

2 Likes

Company’s loan book tenure as stated in Investor presentations for Wholesale book is 3 years, Mid-size LAP - 3 years and SME is 6 years. But when we see and disbursements vs loan book, company’s book runs down almost 100% every year and company has to disburse almost equivalent to their loan book. I understand that there will an element of prepayment in the business and book will not retained in book for 3 or 6 years, but with current rate, their book rundown is much higher than microfinance companies.

Anyone knows why their book runs down such a shorter period, when other SME related lending companies have much lesser run down per year

2 Likes

CSL finance has recorded a 42% growth in net profit to reach Rs 16.8Cr in the 3rd quarter. Company has a mcap of close to 1000cr and available at roughly twice the BV. Leverage ratio is quite low at 1.09x. Number of branches was at 29 as of Q2, company is targetting to reach a branch count of 50-60 by end of Fy25. Q3 GNPA at 0.40% and NNPA at 0.24%.

Disc: Invested.

csl.pdf (3.1 MB)

1 Like