A lot of info has already been gathered and discussed above on this thread.

I stumbled on this company by chance and got interested and read through last 7~ years of AR and some basic checks. Gathered some notes along the way for my own understanding and reference.

Please ignore the information if it’s repetitive.

Current Market Cap: Rs. 152 Crores

Introduction:

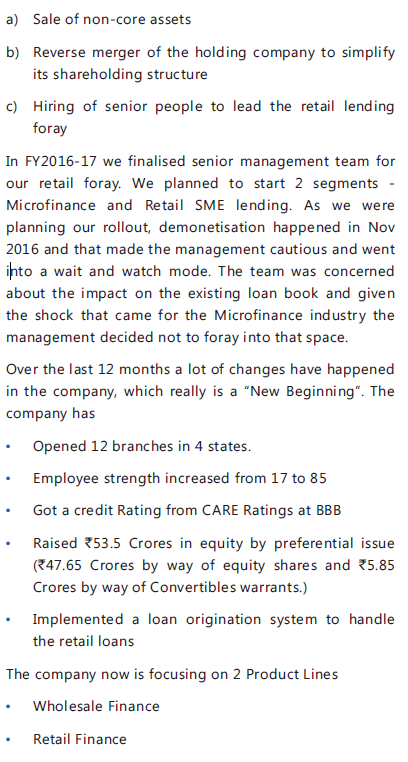

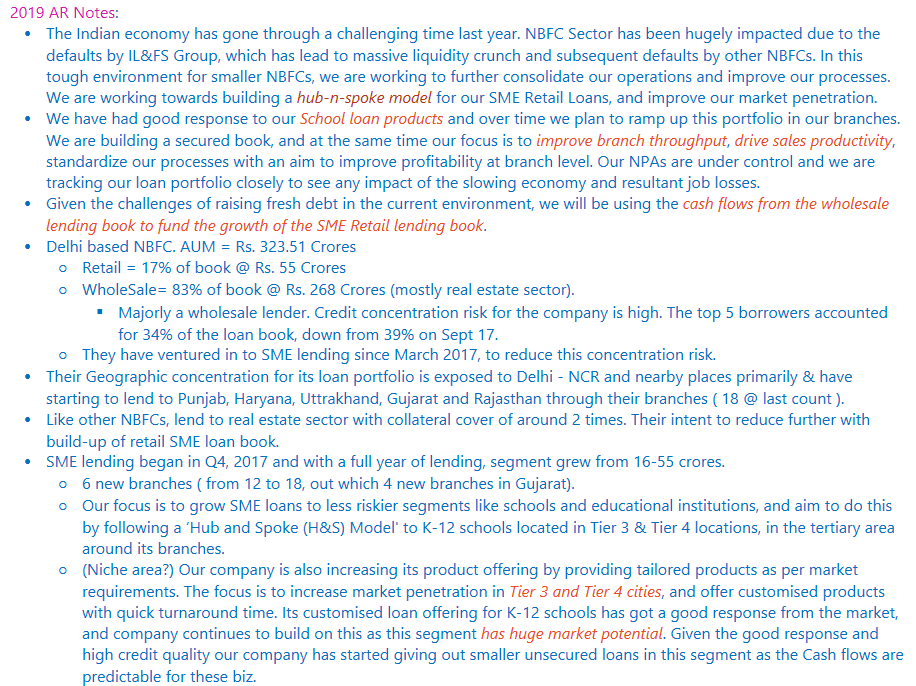

From the latest AR, which is pretty good compared to the past few years AR

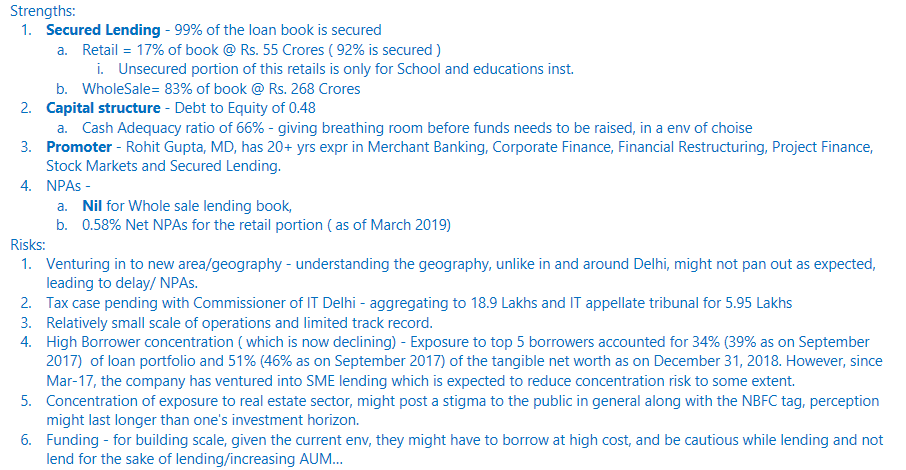

Strengths & Risks:

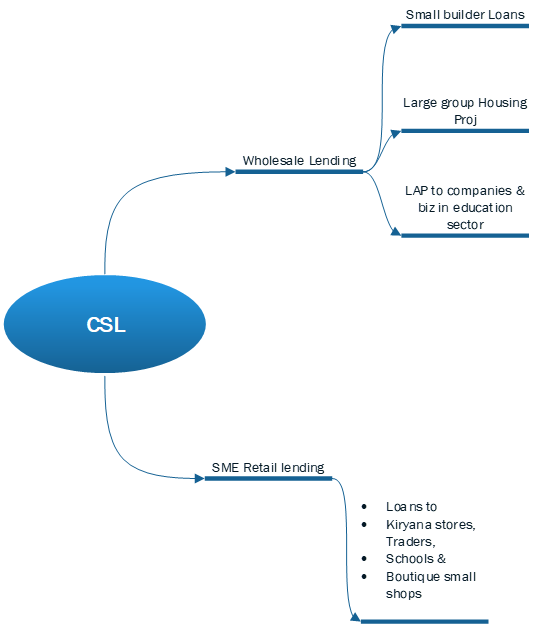

Product lines:

Current biz structure:

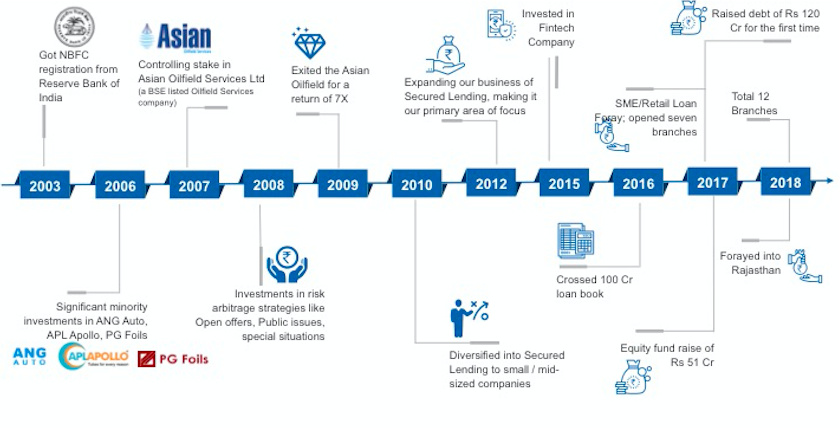

Journey of company:

Opportunity ahead: Large.

NBFC sector, in general, has a long way to go, to help the inclusion of the Indian population and serve the under and un-served population of the country.

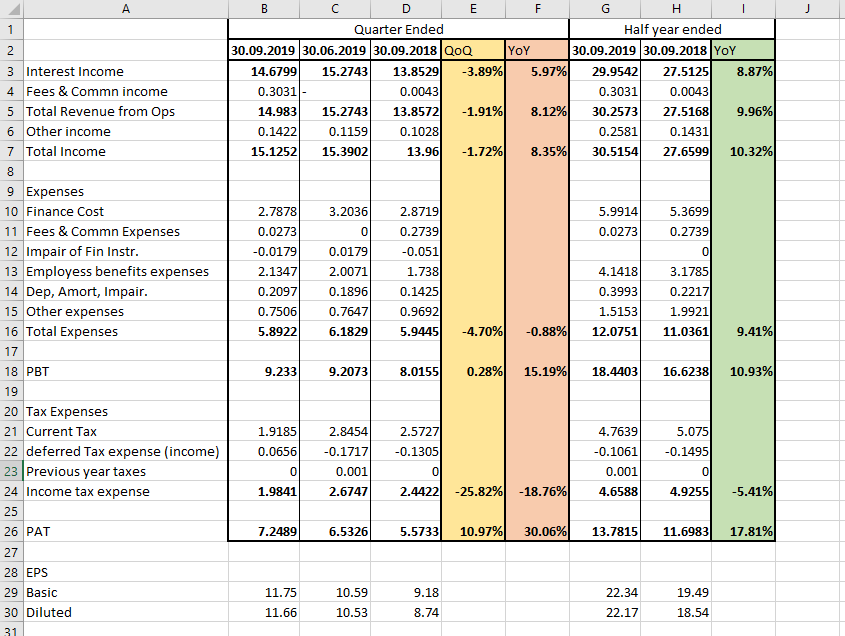

Financial performance:

• ROE (TTM) 12.67, Avg. ROE 5 and 3 years = 12.81 and 13.16% respectively.

• Current P/B = 0.71 ( Something I won’t read too much in to ), has to be looked at in conjunction with a lot of other parameters.

• Rated BBB in credit rating agency.

• Have a low D/E equity of 0.7 and CAR of 66%

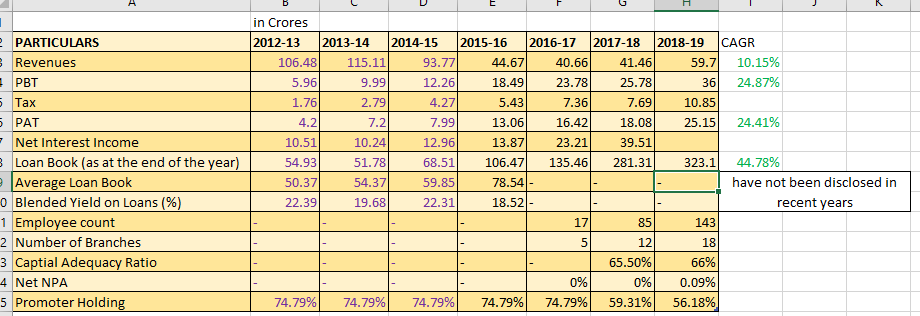

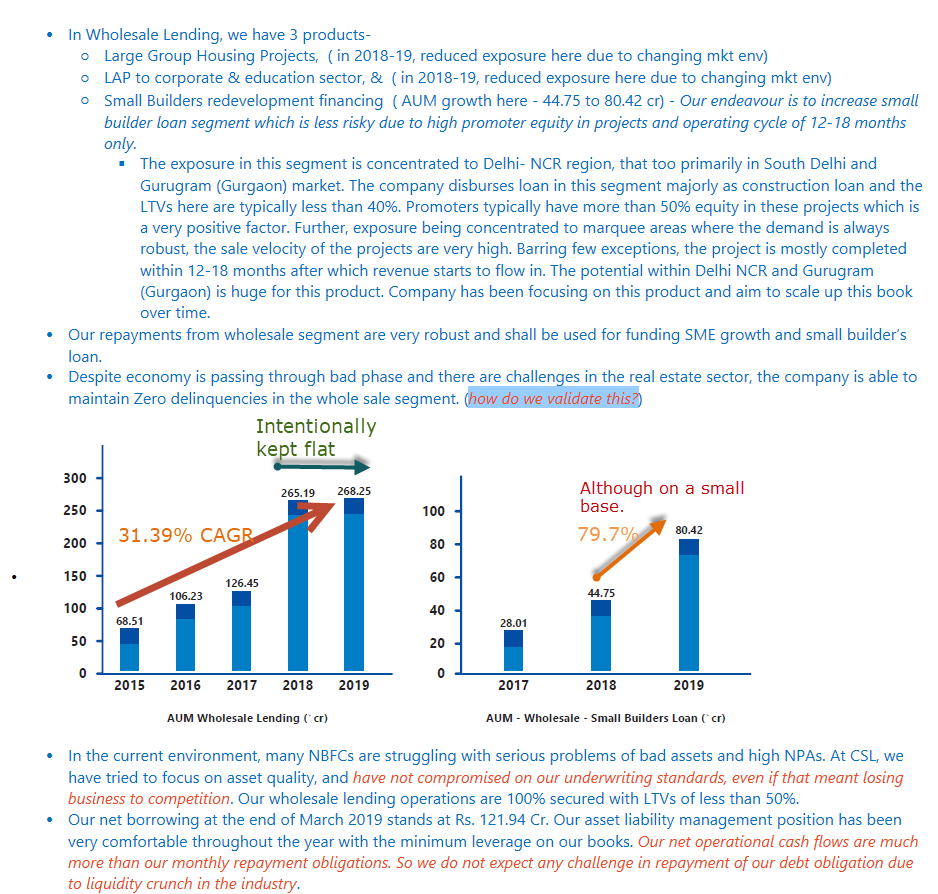

• The below screenshot captures the Sales, PBT, PAT and Loan book growth. In my opinion, we should not look at any one parameter in isolation. Please note the CAGR column is for only when they have consciously lent out money and have moved away from the arbitrage situations, prop investments, etc -

KMP Remuneration:

Note: back in 2015-16, the Promoter salary jumped to 90 lacs from 30 Lacs, which was a significant jump, but at the end of the day with in acceptable range…

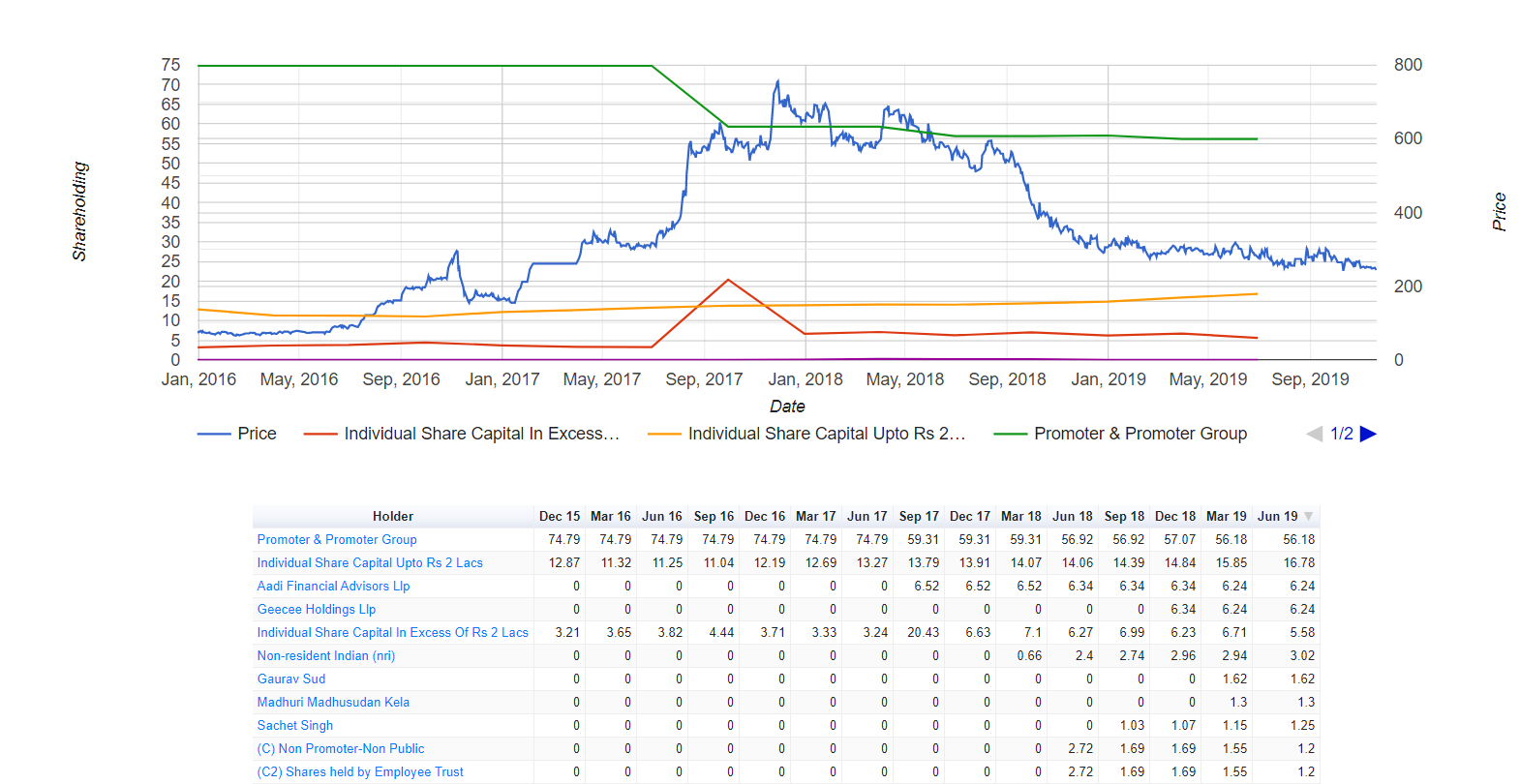

Shareholding pattern:

Promoter holding was at ~75% until they mid 2017, when they issued convertible warrants and equity to raise capital and brought their holding down to 60%. Still a high holding percentage. ( source: Phreakonomics )

Summary:

Valuational Rationale: Although i have seen people regularly use the Price to Book as a good metric to say its cheap or expensive, that is largely insufficient. I have highlighted a few points above in the financial performance section which have been to be looked at holistically…before determining the approx value range for the biz.

I am in the process of evaluating this and will keep this forum posted…

For those interested, here is the much-respected Bharat shah’s guidance on valuing NBFCs - link:Coffee Can Investing | Bharat Shah delves deep into the Science, Math and English of investing

Parameters to consider:

- ROE

- P/B

- derive the Earnings yield.

Using that as a starting point for the yield & consider the below in conjunction and arrive at a value…

-

Capital efficiency

-

Likely growth rate ( with size of opportunity )

-

Credit losses over a period of time

-

account for payout ratios if any ( given that money earnings are their raw material for the business )