Hey Nikhil, honestly I don’t have much more to add than what you probably already know. I’m no expert (in fact far from it). So wouldn’t like to offer an opinion. While I do think the industry in general is quite cheap optically, I’m just trying to understand if the returns that the players are currently generating can be sustained. Demand is definitely there and I believe that the additional capacity will easily be absorbed. I’m just trying to figure out if these players can hold on to their current pricing power in the wake of ongoing expansion.

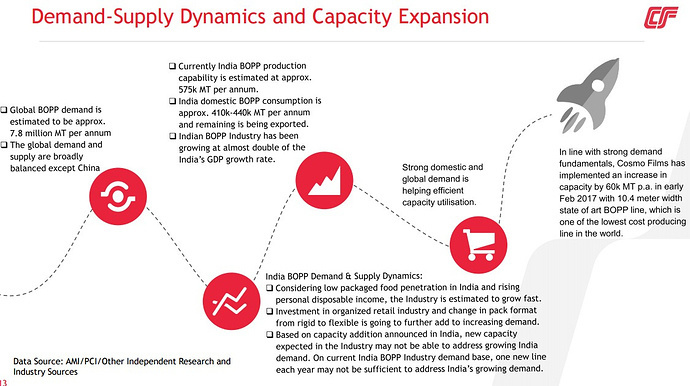

Sachit - This point has been discussed above. I posted a few images which i took from recent presentation from Cosmo. Am posting this again for your convenience. Go through this as this might help you get Cosmo’s management take on demand - supply dynamics.

A DCF valuation shows significant under-pricing. Do you think there’s a re rating expected, once the capex starts churning out more free cash?

The debt /equity is close to 1 now and poised to further increase in the next round of capex. That’s possibly the biggest problem I see with this stock.

Position: invested

Mahesh, This is a capital intensive business without doubt. Usually new line takes times settling down. Immediate few qtrs once the capacity comes online are usually slow.

I remember in one of the interviews mgmt said they will maintain debt equity going forward. SO new apex would be some time away. If you see the borrowings, they peaked in 2014 and was brought down in next 3 years. Now again, they have probably peaked.

A DCF valuation shows significant upside. My calculation shows inr 1300cr vs 800 cr current mcap. Major capex already done, so next couple of years will throw up operational leverage.

What’s the catch here, what am I missing? Am I being too theoretical and missing some practical consideration? The commodity cycle, maybe?

@sajijohn @jitenp I think it is because of the debt overhang - the market usually underprices such stocks. Not sure though.

Thanks Sir. Shall go through this.

Best.

Yes. Cycle is steady now. Few things to look at. U will see that topline growth has been slow for last few years. The main reason is because crude has come off. And their product is a crude derivative. The interesting thing to look at is volumes, margins and bottomline.

Also, the best times to buy these are when RoE is very low, OPM or NPM very low. Which was in years 2013 and 2014. Atleast, thats where I added most of my quantity. Havent’t added anything after that. In bad years you buy and in good years you sell.

Hope this makes sense.

-Jiten Parmar

5 Likes

Cosmo Films among Fortune India’s 25 greatest value creators

1 Like

Cosmo Films will globally launch of its speciality PSA labeling products, black velvet premium over lamination film and top coated direct thermal printable film, at Labelexpo Europe 2017.

http://www.labelsandlabeling.com/news/new-products/cosmo-films-launch-new-psa-films

Why margins lowered ?

Why it’s at such a high valuation and PE as it’s just a commodity play

Jindal poly films is half the Pe but with less debt

Because BOPP prices were lower. This remains a cyclical stock. As mentioned before, never analyze this based on just one quarter.

For me, stock remains a hold at CMP.

-Jiten Parmar

1 Like

My notes from FY17 Annual report -

- Has become largest value added films supplier in India

- World’s largest manufacturer of thermal lamination films.

- Consolidated Revenue marginally declined by 2% from 1616 cr to 1580 cr. Consolidated PAT for FY17 was 89 cr down from 96 cr in FY16. Standalone PAT increased marginally 3% from 108 cr to 112 cr.

- Sales from Subsidiaries -

US - Sales grew 6% tis eyar to 175cr. Losses reduced to 14 cr from 17 cr in FY16.

Japan - Sales grew from 47 cr to 50 c. Though, PAT decreased from 1.42 cr to -.77 cr

Korea - Sales reduce from 47 cr to 42 cr. Losses increased from 4 cr to 8 cr.

So, subsidiaries are still bleeding big time here. Mgmt says they have attaind breakeven at operational level, but i do not see any improvement. - However, sales volume was up 5%.

- Consolidated net debt is now 589 cr, Up from 390 cr last year. Net debt to equity is 1.1

- This mismatch (higher volumes, revenue decline) was caused due to lower prices of commodity films along with reduced RM prices.

- Margins were under pressure for most part of the second half (post November) due to demonetization.

- Lower tax outgo due as the company was able to avail tax deduction on the new investment in plants and machinery allowable under IT Act… Investment allowance having an overall impact of 9.8 cr on its tax.

- Specialty sales of the company grew by 20% YOY.

- On consolidated basis, one time Forex losses in its Japan subsidiary impacted the bottomline.

- On domestic front, demonetization impacted it big time.

-

- Company successfully mitigated these negatives to a large extent by increasing the share of value added films (speciality)

- Overseas subsidiaries achieved break even at EBIDTA level in Q4 FY 17.

- Many new products were launched in the specialty segment this year.

- 10.4 m BOPP line which came online in Feb 2017, will be full operational (ramped up to full capacity by mid FY18). The new installed capacity is expected to add an additional 35-40% production volume in FY18.

- During FY17, capex done was 221 cr. In FY16, capex done was 84 cr.

- Also announced 36000 MT BOPET line to be commissioned during Q3 FY19 at a cost of 250 cr (mostly debt). (niche specialty products).

- Subsidiaries are there in Singapore, US, Korea, Japan, Thailand, Netherlands. Being closer to customer helps fetch better margins.

- CRM implemented this fiscal.

- Strong brand visibility initiatives taken during the year to boost exports.Increased from 612 cr to 638 cr.

- Strong focus on R&D. Special BOPP film for cement bags to increase moisture resistance. R&D expenses grew from 4 cr to 8.4 cr tis year.

Noticeable Shareholders -

Anil Kumar Goel - 3.42% -> 3.40%

Kapil Kr Wadhavan - 0 -> .77%

Lloyd George Indian Ocean Fund 0 -> 1.23%

Dolly Khanna - 0.75% -> 0.72%

JM Financial - 0 -> 0.59%

GS 0.77 -? 0.42%

Mgmt Salary -

CMD 1.34 + 3.88 cr (Commission) (no Increase from last year)

WTD 1.25 cr (25% increase)

CEO 2.57cr (25% increase)

Outlook of the industry -

- Packaging industry is expected to show good growth due to increased consumption. Indian packaging industry has registered 15% CAGR growth in last 5 years. Strong momentum is expected to continue. India BOPP capacity is 570k MT, of which 80% is consumed domestically.

- Significant trends are driving rapid changhe due to increased presence of global multinational companies, consumer brand awareness, products with clean label messaging, increase in per capita income, urbanization, growing number of working women,. e-com

- per capita plastic consumption in India is 4.3 Kg. China is 6 Kg, Taiwan is 19 Kg. So, huge scope for growth.

- GST will benefit supply chain efficiency for FMCG companies resulting in cost reduction in terms of transportation. Reduction in cost will make goods cheaper, which is positive for packaging industry.

Key Risks -

- RM price volatility - Usually a pass though, but with a lag

- Forex fluctuation - Hedges, but still a key risk

Specialty becoming commodity - Increased competition in specialty segment

Balance Sheet, Working Capital and Cash Flows -

- Balance sheet has become more leverages this year with working capital rising big times by 115 cr (68 cr rise in receivables) + 47 cr rise in inventory. Hence, CFO reduced drastically from 245 cr last year to 30 cr this year.

This is a key point to ask, as to why inventories and receivables have rocketed in FY17. Also, i think debt fueled expansion would lead to problems later on. Currently debt/equity is okaish at 1.1, but would have liked them to generate better cash flows to fuel growth. They are yet to stabilize the new capacity and have already announced one more capex for 2019 through debt, which is aggressive.

.

2 Likes

My relationship with stock for last few quarters lead to 2 conclusions:

- Raw material price risk will remain and pricing power is missing

- Ability to become debt free looks minimal

Fist point I was more or less aware but it was second point where thesis looked like going wrong based on signals I got. Also, point 1 makes point 2 more and more difficult.

Also, was not happy with some of allegations over promoters which I found while drilling further.

Disc: Exited few months back

2 Likes

Thank u for the info. Can u elaborate on the allegations on the promoters? If true, it is more adverse than point #1 & #2

1 Like

I guess people want distance with name jindal

Which allegations against promoter ?

1 Like

Dont think any outcome has come and looks like coming in near future but then better safe than sorry.

2 Likes