Thank you, I wasn’t aware of it.

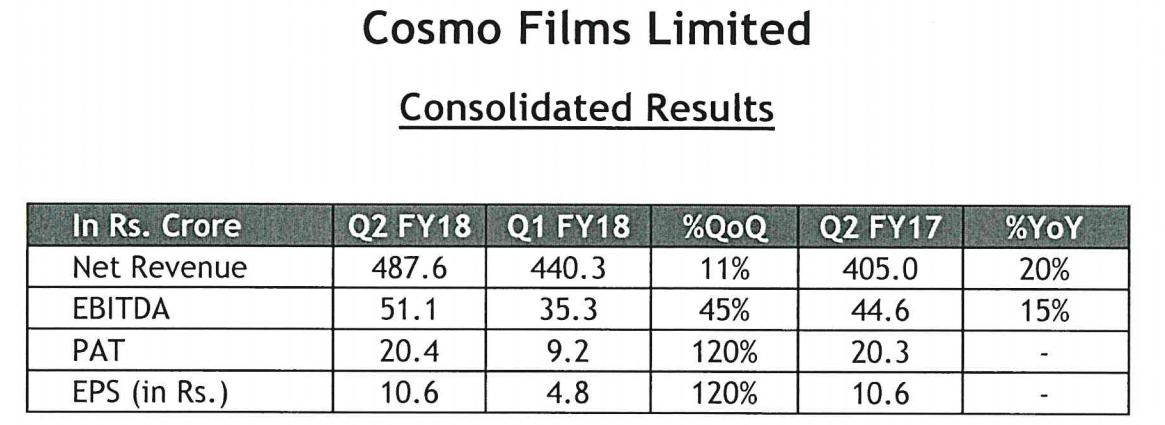

Results came post market on Friday. Looks decent, at first glance (thanks to other income!)

http://www.bseindia.com/xml-data/corpfiling/AttachLive/ecc9d199-7e8d-478a-b659-381298243e56.pdf

2 Likes

Hi Jiten,

What do you make out of the H1 performance? Margins have deteriorated to 7% from 11% last year. Operational cash flows have dried up (was below 30 cr in Fy17), and working capital requirements are increasing with rising receivables and inventory. Payables have reduced sharply in H1. Debt has increased by 250 odd cr due to expansion and higher WC requirements, rising crude will further pressure margins and Working capital.

Topline has risen. But, they are now operating at 95% utilization. Moreover, 50% of this revenue they claim is coming from specialty segment. Do you think specialty is soon becoming commodity?

1 Like

Yes. I was expecting these kind of results. I don’t think they are working at 95% capacity. Cosmo remains a 2-3 years story.

In that sense, I have added more in Uflex, as there is much more value addition there (it’s a actually a packaging company).

Hi @jitenp small question on Uflex. Doesn’t the fact that they have high receivables, especially those greater than 6 months disconcerting for you (especially compared to Cosmo)?

Sachit

From where can we track BOPP BOPET prices?

1 Like

Please let me know any one has update on latest quartely results

Many companies in this segment having the issue of deteriorating OPM, which indicates, most probably, excess supply.

Increasing volumes sales indicates the demand …

It may takes a couple of quarters for the suppliers to pass the cost of expenses to customers…

Hey I have the same query. Also wanted to know where can you track poplypropylene prices ?

How do you check the leverages are in your favor or not??

Leverages are in your favour if

- Operating leverage : Industry level Capacity utilisation is @ historic low & sales are growing

- Margin Leverage : Industry OPM is at historic low because of sudden change in RM cost or currency issues

- Financial leverage : This is dependent upon Debt levels - Idea is to back firms which can survive & generate enough cash to pay back debt …

4 Likes

Operating leverage - basically when sales (industry) had hit the bottom and revival has started happening, right??

Can you expand your thought on each one of these? If we could discuss these with some examples it will be easy to understand and visualize each of the situations.

That will also help us rules out any other possibility if any exists.

Thanks

You can observe these in all cyclical commodities stocks both consumers of commodities and suppliers of commodities . Read this blog article written in 2014 … http://crazyinvesting.blogspot.com/2014/05/de-coding-crazy-terms-consumer-cyclicals.html

E.g of Supplier of Commodities : Hindalco : 2014 vs 2017

- Operating Leverage : New Al capacity was coming in stream in 2014 - 2015 and gradual increase in capacity utilisation from 2014 onwards - Increase in Volumes

- Margin Leverage : Look at OPM % - Highest was around 20% in 2007 , it dipped to 4.5% in 2014 and gained to 11.7% in 2017 still has potential to gr to 14%

- Financial Leverage : Highest debt levels of 68000 crs in 2014 and no plans of new capacity addition indicating debts levels will start reducing and hence increase higher PAT increases

Same in visible for Mah Seamless , Graphite , Cosmo films etc

3 Likes

concall Q4 Fy17-18 Notes :

Achieved highest ever sales volumes (new BOPP line got commissioned in February last year)

Topline grew 22% ; volume growth at 25%

The management does not envisage production lines to be commissioned in fy’19 (1 line at the maximum)

Government ban on plastic packaging - packaging films that are not recyclable will be phased out

Margins for commodity films are 10rs/kg compared to 14/kg last year. Normalized margins have been in the region of 16/kg. In case of specialty films, margins are 36rs/kg compared to 40/kg last year

Market for BOPET Films – demand – supply is fairly balanced. 85% of the supply is consumed domestically and the rest is exported. Margins have expanded by 10/kg . Time taken to start/commission a new line is more than one year

Specialty films contribute 40% in volume terms and 55% in value terms; intent is to scale this to 75% of topline in the next three years

Pricing in the market is on cost + value addition basis. So crude price wont affect much.

Five new BOPP production lines have come up in the last fifteen months. By the late 2018, only one more production line is expected to come up . Management mentions that this level of margins cannot sustain in the long run, however timing the recovery is not possible.

A confusing comment : management says expect 1 line to come up in next 18-20 months which wont impact as demand is pretty decent. on the contrary they also say no new BOPP line in india. i couldn’t understand if it is in india or at global level.

Global BOPP Capacity – 8mtpa, Indian capacity is 600k mt. Having two lines in overseas market would not have an effect on the margins of domestic players. Due to import duties and freight costs, it is unfeasible to import BOPP films

1 line typically gives you 25,000 tones. Replacement cost for one line is 200-225cr

Crude has an impact on Polypropylene prices. Pricing happens on a fortnightly basis where raw material costs can be passed on the customers.

Margins below 10.kg on commodity films will mean that manufacturers will make cash losses

Capacity utilization in fy’18 has been at 95%; Major part of capex will be incurred in fy’20

Current capacity of the company is 196k tons.

capex for FY19 is will around 25cr for CPP films capacity expansion.

borrowing cost is around 6%.

In my view : margins are almost around bottom.

disclosure - i have tracking position.

2 Likes

pls find the screenshot of BSE website showing fresh acquisitons of the promoters & group to the tune of 2.54cr in the months of june & july. What does it signify. Does this mean that margins have started improving in Q1 2019 from its bottom. Kindly provide your insights.

1 Like

Promoter buying is a good sign, when huge quantities are bought. Here they are buying small amounts. Although many promoters starts buying much before the bottom is created. So can’t be sure if margins will improve in Q1.

BTW Prakash Industries also started producing packaging films. Not sure which one. If they are also in same business. Then margins improvements gets delayed.

Promoter has again made a fresh purchase from the market for the value of 39.96Lacs on 1st & 2nd of Aug 2018.

1 Like

Q1 2019 results out. QoQ topline revenue has grown 3% from 501.98cr to 517.57cr. Gross profit margin remains flat Q0Q around 26%. Margins are still under pressure.

ttop line growing YoY and QoQ is a great positive. But will the market respect the Revenue growth??? Or the market going to punish more for subdued margin???

Latest investor presentation