A cop to guard house and keep watch is also culprit. Auditors are also equally guilty.

1 Like

small report bank Frauds

1 Like

u check the auditors of major company and u will find common set of auditors under whoes nose all this frauds have reported . auditors role were to keep check on accounts but they themself are in hand in glove with company.

2 Likes

CAn it be a Black swan , in Indian context ??? MONEY Life is really digging out the rats …

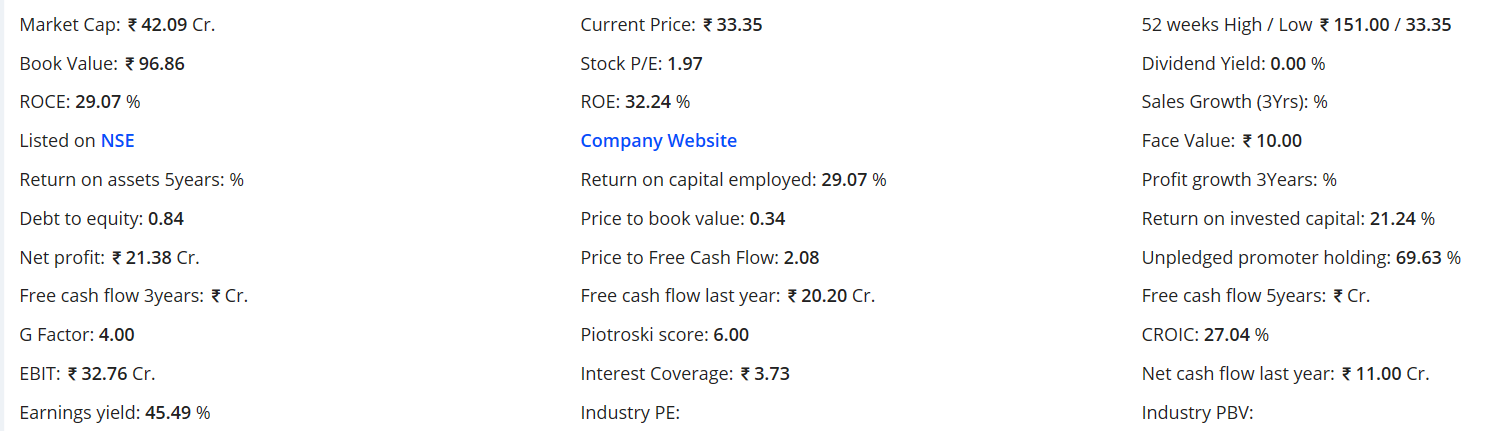

Fundamentally Company looks good

Despite of all the caution people are greed creatures … Rather we should follow the age-old strongest emotion i.e FEAR and cautious about the choices we made … INVESTMENT is not BETTING it is Discipline of following the Process … but sadly we only learn with OWN experience

Disc ; i am not Sebi approved analyst. Tis is not any Buy or Sell recommendation .I haven’t invested in this company in past and not even now

3 Likes

List of Heavy Debt Companies.pdf (671.5 KB)

Did not find appropriate thread for this , hence posting here, Mods please move if its not in right place.

4 Likes

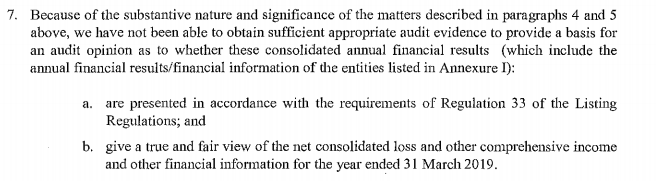

The audit report and notes to accounts for FY19 for Reliance Infra make for interesting reading. I can’t recollect an audit report in the last 10-12 years which has been longer than this one (10 pages for the consol audit report!).

The joint auditors KPMG and Pathak HD & Associates have given a disclaimer of opinion, basically saying that they can’t certify that the accounts show a true and fair view. See exact wording below:

The good thing is auditors finally seem to be have been galvanised by fear of draconian regulatory action into making honest disclosures.

Disc: Not invested. Purely academic interest.

5 Likes

2 Likes

Yesterday I received an interesting and useful email from CDSL giving a list of companies that have not complied with SEBI listing regulations. I am attaching the text of the mail below and uploading the list:

————————————

Dear Sir/ Madam,

SEBI, vide Circular No. SEBI/HO/CFD/CMD/CIR/P/2018/77 dated May 03, 2018 prescribed the uniform fine structure for non-compliance with certain provisions of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“Listing Regulations”) and Standard Operating Procedure for suspension and revocation of trading of specified securities.

Investors are requested to kindly take a note that following companies in which you have invested have not made required submissions to the Exchange as per following regulations within the prescribed time limit for the quarter and year ended March 31, 2019.

Reg. 27(2) for Corporate Governance as per SEBI (Listing Obligation and disclosure requirement) Regulation, 2015

Reg. 31 for shareholding pattern as per SEBI (Listing Obligation and disclosure requirement) Regulation, 2015

Reg. 33 for Financial results as per SEBI (Listing Obligation and disclosure requirement) Regulation, 2015

Reg. 13(3) for Grievance redressal Mechanism as per SEBI (Listing Obligation and disclosure requirement) Regulation, 2015

Reg. 76 for Reconciliation of share capital audit report of the SEBI (Depositories and Participants) Regulation, 2018

The Exchange has levied fines and also issued notices for such non-compliances to the companies. The continued non-compliance of such regulations may lead to further regulatory action on the companies which may include suspension.

This communication is being sent by NSE in the interest of investors.

For further queries you can reach to NSE on 1800-266-0058.

—————————————-

Annexure.xlsx (12.4 KB)

13 Likes

DHFL results for Q4-FY19 and FY19 out today. The notes to the results make for interesting reading. Some highlights:

- Results are un-audited and un-reviewed even though it’s been 3.5 months since the end of the financial year. Apparently the audited results will be released by 22nd July

- DHFL has written to borrowers of project loans some 3-4 months ago, in cases where end use monitoring was not done and they claim that they haven’t gotten responses from the borrowers. How would borrowers respond when they are probably non-existent

- This one is the funniest: Apparently cheques were collected from borrowers as repayment, accounted as receipts, but were later not deposited for an amount of 1875 Crores. Who in this day and age uses cheques for such large value transactions and secondly how did the amounts just happen to be a nice round number of 1875 Crores?

- They have reclassified 34800 crores of wholesale loans as held for sale and have taken a hit of 3200 crores as a result of revaluation loss

- Their expected credit loss model is incorrect and they are in the process of rectifying it

- NHB has just woken up to the scandal and issued observations for FY18 in which they discovered that capital adequacy as on 31st March 2018 was only 10.84%, while the numbers reported as per DHFL FY18 investor presentation (https://bit.ly/30y0bGC) was 11.52% for Tier 1 and 15.29% for overall capital adequacy

Link: https://www.bseindia.com/xml-data/corpfiling/AttachLive/44ed265f-cd5f-437c-9afe-e40b78422628.pdf

Disc: Not invested

9 Likes

Thank you.

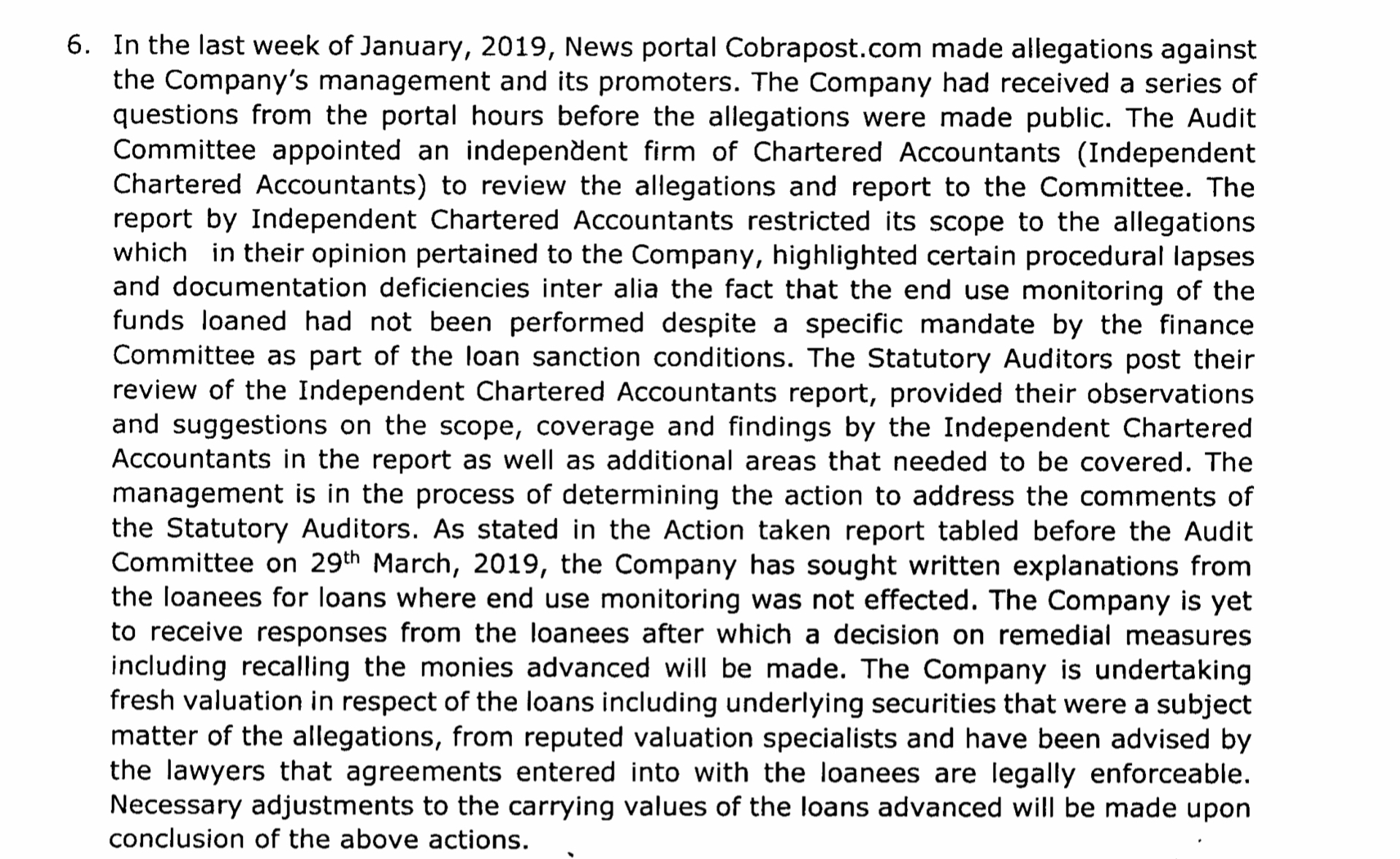

Amongst other things, Note #6 to accounts was indicative of the state of affairs to come:

A report, post Cobrapost, on 29 March 2019 shared with Audit Committee (and not disclosed to shareholders) indicated loans were made for no good reason and the company then suddenly woke up asking the loanees if they are indeed using it for good reason. But no one responded till July 12, taking this visionary firm for a hapless ride. DHFL has said, ‘alright I will wait for some more time’. And then it will decide whether to write them down!

2 Likes

“the company has sought written explanation from the loanees”.

Written explanation for what?For knowing if the loans were used for the purpose disclosed, for knowing how they got the loans without being subjected to “end use monitoring”,or for knowing if they have provided adequate securities…

This is an exercise in futility and meant to further obfuscate the issue and buy time instead of fixing responsibility and initiating due action.

Wonder how Rakesh Jhunjhunwala would feel and whom would he blame for this investment or how inadequate his due diligence has been.

2 Likes

Listed in BSE SME

Rajnish Wellness Ltd

(RAJNISH | 541601)

2 Likes

DHFL finally released the audited results for FY19. Again a really long and interesting read, but pretty much similar to the un-audited results released earlier. One of the current auditors, Chaturvedi and Shah have been the auditors since 2016. It appears that they have suddenly realised 3 years down the line that the books were cooked. I really dont know what to make of reactions of surprise from the auditors now.

Link to the results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/3642f96a-2ce0-49f4-b6f1-2d0b857ecab4.pdf

1 Like

Weren’t they the auditors for Reliance Industries some time back or do they continue to be auditors of RIL?

Chaturvedi & Shah used to be RIL’s auditors for a long time till 2017. They are no longer RIL’s auditors.

The latest fraud in Crompton Greaves Power(CG Power) disclosed earlier this week, a long read and makes other frauds look like a game. Some key highlights (full read below) . Due to this, the company’s debt has balooned https://www.bseindia.com/xml-data/corpfiling/AttachLive/a9c9fc80-29ea-47c4-a6ec-40cf4f1342e4.pdf

- Related parties not identified correctly and advances given to them/writeoffs of loans without approval

- Undisclosed corporate guarantees/letter of comfort given to promoter entities and invoked when they defaulted.

- Unauthorized royalty to promoters which was further assignd to lendors even though company had not accrued provisions

4 Likes

Update on CG Power - https://www.bseindia.com/xml-data/corpfiling/AttachLive/433c7c49-cc13-4932-a519-32da5e6933e5.pdf

Company is now trading at 0.22 of Book Value.

A storied investor has been pulled up by the court. Prem Watsa, often called the Warren Buffett of Canada and with large investments in India, was found by the Montreal court to have shortchanged shareholders.

Mr Prem Watsa, who is otherwise an epitome of supreme confidence was found to be on the defensive and forgetful. "the judge said, adding that the court also found “that Watsa often appeared to be on the defensive and when pressed on crucial factual elements, the witness hastily took refuge behind ‘I do not remember’ or the like.”

Some of his transactions in India also elicited similar questions.

6 Likes

Some common themes we have seen before -

- Connection with politicians, HDIL born after rules changed

- Promoter seen more in page 3 than business page

- High and unsustainable debt

1 Like

Talwalkar is a classic case for fraud and con artist in action- promoter siphoning investor money but very convincing and showing how genuine they are.

The funny story is when the stock price crashed in July-19, the promoters came to ZEE News on 24 July and stated that they were not aware of what happened and who sold them and what caused the crash. He also reiterated the fact the company is AA rated. Within two weeks company was declared default by the credit rating agency and could not pay few (3 to 4 cr) of interest on their loans. This rating shows the quality of the rating agency and the supreme quality (?) job they are doing.

If the rating is reduced by a notch, it is understandable, but AA to default within two weeks is fishy- from promoters as well as from credit rating.

I have been an investor in Talwalkar for 5+ years and believed (foolishly) that they are saying. I was about to exit, within a couple of weeks as, I have made up of the mind and about to exit, but the crash happened, and I ended up getting an experience instead of investment returns. To quote a sage “Experience is what you get when you do not get what you want”

Some of the value picker members( @zygo23554 and @Marathondreams) were spot-on in detecting something fishy and warn fellow investor, but I failed to act on it in time. Hence I deserve rubbing my rose for decades to come and vows not to repeat the same mistake.

The story started first when management stated their intention to sell properties worth 120 cr, which were recorded as assets on their balance sheet. After debating for a few quarters, the promoters created a financial engineering marvel by doing spin-off- splitting one company into two separate companies.

Talwalkar Better value fitness (lifestyle) and Talwalkar Health clubs (Gym) with an assumption that a lifestyle company will be loaded with debt and other company (Gym) will have less debt. However, after the spin-off, they loaded the Gym company again with debt. In FY 2019, they increased the debt of the Gym company by whooping 50% in 12 months.

The spin-off took around 4 to 6 quarters, and the company was listed sometime in March 2018. Considering that the lifestyle company to be listed in March 2018, one would have expected financial results of the lifestyle company to be published with a later date (say Dec 2017). But they published the result of the lifestyle company all most two years back and never published recent result despite investor (myself included) asking them for latest result. As a result, in March 2018, the only result which was available for lifestyle company was March 2016. This should have a first sign to smell, which I did (partially ) and existed the lifestyle company.

Little did I know that they would launch a full-scale drain on company’s financial on Talwalkar Gym. Here I forgot to act on the wisdom of a Warren Buffett - “You cannot make a good deal with a bad person”. If their intention were somewhat scrupulous for one company, it could very well be same for other companies in their portfolio as well.

Some other Key points:

-

Promoters started building an empire- buying company across health- yoga chain, Gym in Chennai, Mumbai, online business, nutrient business and even ventured in Srilanka. As this was not enough, they won a master franchise for a gym in 5/6 different countries in east Asia.

-

They have choreographed 20% PAT growth for many many years. Respected value picker member as had raised the timely flag of it as I had to rub my nose, so it happily ignores it.

-

When the lifestyle business was listed, there was confusion if it was a gym business or lifestyle business. In fact the listing price for lifestyle business happened as if it was a gym business. For some days, there was confusion which was gym business and which was lifestyle business.

I was thinking of writing this on Talwalkar thread, but the thread will join the history book. But the current thread is the right places in my view as others will keep referring the story at a later date and hopefully learning and avoid similar fraudulent activity in future (History does not repeat but Rhime).

I am sure many people are aware that Motilal Oswal has lost money in Manpasand beverage. Mr Ramdeo Agrawal is very candid about it, and in one of the interview, he was reflecting on Manpasand investment. MOSL smell some fraud in the company but hoped that it would go away, but it didn’t and end up in history book. Mr Agrawal said if he senses a fraud, it is worth running away from the company the moment you know, even if you sell 100 bagger potential in the stock.

Moneylife has done the exceptionally well job of describing what’s happened. Highly recommended.

17 Likes