Thanks @madhavikkutti for the details outlined, from the message above it looks like the future is tilting towards EAF and I am tempted to ask if there is a way to play that theme(EAF) in the listed space

Iron ore prices softening?

NMDC has reduced Lump Ore and Fine prices by Rs 100 per tonne wef 1.3.2018

The present price is Rs 3000/ and Rs 2660/- respectively.

It’s a small cut. Nothing major to be worried of. I m comfortable holding steel mining plays as long as Iron ore stays above 65$ mark on sustainable basis.

1 Like

I believe, the most attractive EAF plays are the ones which we are already talking about - Graphite India and HEG

As per reports, after attending the 23-Feb Graphite Electrode (GE) Industry conference, Jefferies are expecting the prices of GE to be north of USD 10,000 per ton and the current spot prices in China are USD 25,000 per ton. The tight demand supply situation for GE is expected to continue for the next few years and prices will remain at elevated levels. Jeffereies has the latest target price for Graphite India as INR 1,135 and HEG, INR 3,622.

Please refer to what Graftech, world’s second largest producer of GE is telling its unitholders (https://bbu.brookfield.com/en/reports-and-filings/financial-reports/letters-to-unitholders-html/q42017lettertounitholders) after their Dec-17 results: “Given its industrial advantage and strong customer demand, GrafTech has successfully negotiated multi-year take-or-pay agreements for 60% to 65% of its production capacity over the next five years. The weighted average contract price over the next five years for contracted volume is $9,700 per metric tonne, which is approximately double historical average prices (although for a variety of reasons we expect go forward average pricing to be higher).”

Hence, even if we assume a GE price of USD 10,000 per ton and needle coke price of USD 2,000 per ton for FY19, I assume an EPS of around Rs 121 for Graphite India in FY19, which is 4.53 times the TTM EPS of Rs. 26.71.

1 Like

Wondering what is impact on Indian

- Steel manufacturing companies

- Companies whose finished products are steel products and raw material is steel

- Aluminium manufacturing companies

- Companies whose finished products are Aluminium products and raw material is aluminium

1 Like

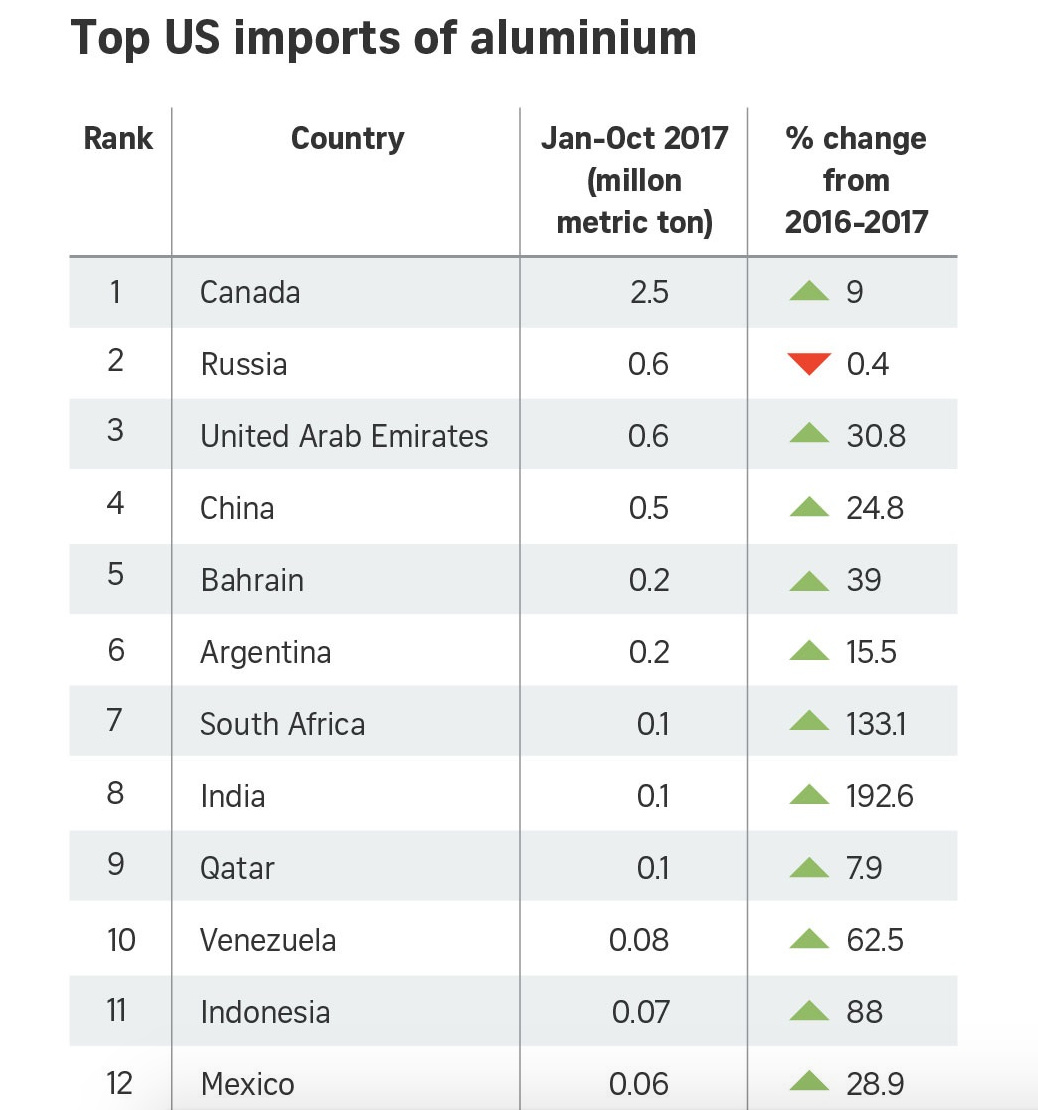

@madhavikkutti Thanks for sharing the article. I can see that Aluminium imports from India to US has increased by 192 % in the last year. Do you think with this new tariff will impact NALCO’s or other Aluminium exporter’s share price ? @jitenp may be you can also share your views on this one ?

1 Like

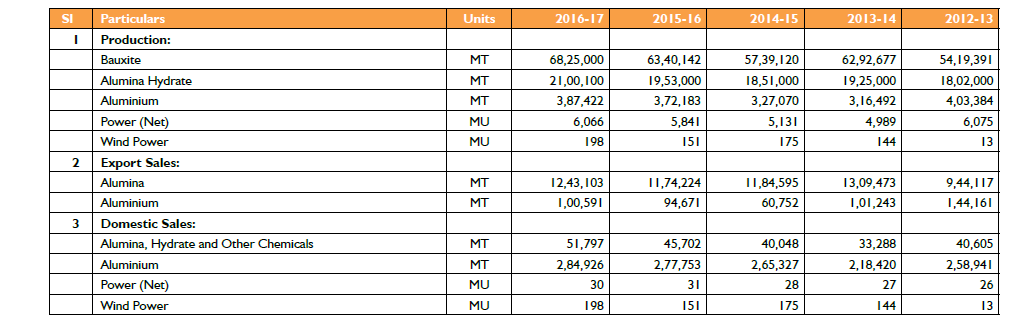

These are 5-yr. figures for NALCO.

It seems India is a net importer of aluminium. Or is it that the deficit is overcome by recycled metal. But it is clear that exports of aluminium from India to USA are only a small fraction of its total aluminium exports.

Source: Annual Report of NALCO 2017.

3 Likes

Hi @SD007, As per the following article, the impact will be minimum: https://www.google.co.in/amp/s/www.indiainfoline.com/article-amp/news-top-story/president-trump-considers-approving-harsh-import-duties-on-steel-and-aluminum-products-118022600022_1.html

In fact, it should be positive for Hindalco. Its US subsidiary Novelis is likely to see a sharp growth in both realization and volumes owing to the new protectionist measure by the US government.

1 Like

US aluminium Futures show a long term bullish trend

Thanks @madhavikkutti for the pointers.

From your above table in the earlier post, assuming Graphite India negotiates the price to USD 8000 per ton and needle coke to USD 1600 for the future contracts the EPS comes upto 88, taking this figure into consideration the Forwad PE for FY19 comes upto 8 which looks pretty attractive from a valuation standpoint,

I believe you are also on the same consensus from an investment point of view, am I right in my interpretation.

Once again thanks for the pointers.

Guys…unsolicited advice. Don’t use p/e multiples with such extreme cyclical companies. 8 p/e is cheap but not for cyclical company. Cyclical company is considered cheap when no one wants to buy it (when it is barely managing).

P/e will skyrocket if after 3 years it cannot sustain this profitability. So employing p/e to value these companies is a recipe for disaster unless one knows when to jump out of ship before it sinks.

One should rather use normalized earnings with such companies to determine valuations.

10 Likes

Dear @Mridul, Thanks for the opinion on this.

While P/E is not perceived to be as an effective mechanism for valuing the cyclical stocks, I doubt if normailzed earnings can either be used to understand the right valuations of Graphite India, considering the “special” situation in which it is in currently. Please let me know if my understanding of the “normalized earnings” itself is right.

I can calculate the normalized earnings by taking an average of the earnings of the company for the past say 10 years, assuming that it went through one complete up-down cycle over the past 10 years. However, will the above figure help in the case of Graphite India? The unprecedented rise in the price that we have seen recently cannot be attributed to its regular up/down cyclical trend, but due to a special situation, which is China crackdown on pollution.

As per reports, whatever China has done on pollution is an irreversible process and the crackdown is likely to continue in future also. Also, as per reports, Graphite electrode shortage is likely to continue for the next few years (at least for 5 years) for various reasons.

Graphite India’s average EPS is Rs. 7.26 over the past 9 years, when I believe it has seen one complete up/down cycle. How do we make use of the above figure as a guideline to determine whether the stock is currently undervalued or overvalued with its current TTM EPS of Rs. 26.71? This question becomes even more relevant especially since I have estimated very high EPS’s of Rs. 88.3 for FY19 (if we assume GE price of USD 8,000) and Rs. 285.2 (if we assume GE price of USD 20,000). Also, there is an expectation that, similar earnings may be repeated for the next many years also.

Sorry to ask one theoretical question, but I think it will help in getting my doubt clarified a lot. What if the company did really achieve an EPS of Rs. 285.2 in FY19, which is more than 10 times the current TTM EPS? Don’t you think the stock price would increase significantly, especially since there is an expectation that the same EPS may be reproduced over the next few years also? Or, will the stock price not increase, fearing the very low historical normalized earnings of just Rs. 7.26?

Your valuable thoughts on this will be appreciated.

Normalized earnings, by definition, are adjusted to remove the effects of seasonality, revenue and expenses that are unusual or one-time influences.

P/e is not the right measure, i will tell you why. Look at metals now…imfa is at 4x, earnings potential still intact till steel cycle is up. Still why it has been hovering around 4-5x from quite some time? It is because may be it has attained sort of seasonal peak after which they have to go for capex to grow by volumes rather than realizations.

Better indication for such cyclicals to determine peak valuations is EV/EBITDA. Just peek into history to determine max multiples and the conditions existing then.

With extreme commodity one can never be sure. So time for entry with good MOS is import. I would not comment specifically on graphite as this is again a special situation. Length of cycle can vary, but i would look for margin of safety from here. If u r sure it can improve earnings from here or utilization is not at peak., And global supply won’t be back, well take your call. There can be other issues when a sector makes extreme money…other related industries may struggle leading to issues. It cannot be defined as every instance is different with different triggers

2 Likes

Thanks Mridul. GE represents only a small share of the input cost for the steel producers. Hence, I think, steep pricing by the GE manufacturers is unlikely to bother the steel industry much. The struggle could instead be on whether the EAF producers can manage to source sufficient GE (due to its shortage) so that their production is unaffected

Correct. Mridul. My philosophy has always been to sell at about 6-8 times peak earnings, in case of cyclicals. Or atleast, be very alert. Definitely never buy at these.

2 Likes

Graphite electrode market to reach 2 million ton by 2020,now it is 1.7 million ton.out of 1.7 Mt,china has capacity of around half of that but China has got limited UHP electrode manufacturers (UHP electrode is most preferred in EAF).Now China wants to go for quality products and also China is planning for 13℅ EAF which is now 5℅.so export from China that also of UHP is going to be limited