Can we expect similar performance or better from Godawari Power & Ispat Q3 results to be announced on 22 Jan 2018?

Thanks Prakash:grinning

Q3 Results attachment.

b8d365d7-d064-4ebe-9cf1-ac1d34d12b5cgodawari.pdf (2.9 MB)

Investing is about looking in front and driving, not at rear view mirror always. An occasional check there is ok, but mostly u must look in the front.

-Jiten Parmar

Very apt for cyclical investing in particular.

6 Likes

Sir

Hote/Hospitality stocks are touching 52 w highs any view on that sector ???

I want to slowly understand things that work in cyclical nature. But the stocks mentioned are Uflex and Cosmo Films which does not look like a pure cyclical play! Commodity kind of stocks generally goes cyclical way!

Ok, checked few pages of the presentation and it looks like the one I want to know more about. It is about commodity kind of subjects. So, Presentation is worth studying.

Hi,

Why Packaging firm is in cyclical? They serve evergreen FMCG then business is there always. Should be little and normal ups and down? Or it is FMCG that does cyclical and Packaging firm is an indirect play so you have bought!

Thanks & Regards,

Satya

Cosmo like companies are highly dependent on crude cycle. Margins working capital get impacted big time with crude swings. Moreover, this segment is highly effected by supply demand scenario. Margins in all commodity companies fall with supply gut. Currently all packaging companies have undergone huge capex in BOPP segment. if you go through Cosmo mgmt’s commentary, you can feel the pain, as specialty few years back has become commodity now.

2 Likes

There could be two way of cyclic effect ,one as highlighted by @Mridul , COGS level cyclic behavior where company is not able to pass the benefit . The second could be demand supply equation of product or service being sold. Usually, in commodity industry where barrier to entry is low and things are going great , everyone expands capacity to meet rising demand which leads to sometimes overcapacity in a stable demand (like fmcg), sometimes overcapacity in falling demand (like infra). Based on extent of mismatches related to COGS,demand , supply and companies/sectors bargaining power, the strength ,weakness n longivity of cyclic industries may differ . This has been my limited understanding .

3 Likes

Correct. It very much depends on supply/demand. And there is oversupply currently. so, margins are impacted. Impact on Uflex is lower as it also has packaging. And it’s the largest packaging company in India.So margins are much less cyclical.

2 Likes

You’ll Want to Read This Living Legend’s Thoughts On Copper

Nalco shareholding pattern on moneycontrol shows following figures indicating - over 100% increase in mutual fund holding of Nalco in last quarter ending Dec’17 over previous quarter.

Holding of Mutual Funds in quarter ending Sep’17 - 56,189,634

Holding of Mutual Funds in quarter ending Dec’17 - 118,304,918

http://www.moneycontrol.com/mf/user_scheme/mfholddetail_sec.php?sc_did=NAC#NAC

Any views on Godavari power result? Is there value still left to add more at current price?

1 Like

Very good results. Based on my calculations, Q4 should easily be much better.

Any fresh views on Hindustan copper? It has its results on 31st. Copper prices have been 10-20% higher than during the last quarter, while hind copper has corrected quite a bit. Seems like a good buy, but need to do a proper valuation.

Disclosure: Invested heavily.

It is seriously under valued. The new normal should be 100-120 range…

Disc: Hind copper small quantity in satellite pf. Holding Vedanta, Maithan Alloys, Prakash Ind. Extremely bullish on commodities now.

Hi Amit, any idea about the impact of proposed QIP from Hind copper? How do you see this move? Will market appreciate this move at this stage?

Price of stock was subdued due to known

Internal reasons! Any thoughts?

Disc: invested well

Do you have any opinion on how the QIP would affect the stock price?

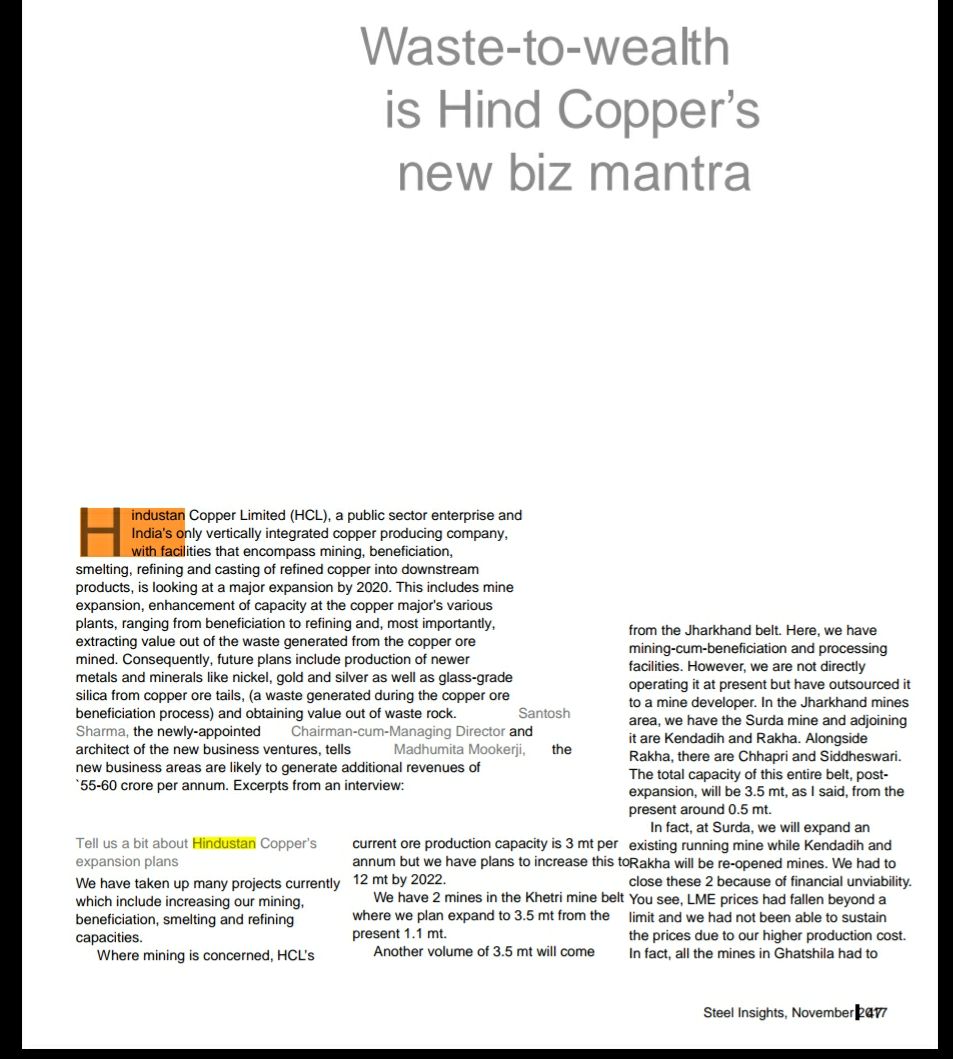

For people following hindustan copper, here is a very good management interview. Management expects 5000 crore revenue by 2020[vs 1200cr last fiscal], and their expectations of copper prices are lower than that off the market[6000 USD expectation vs 7000 USD currently], which means their estimate is conservative and actual revenue could be much more.

Disc: Invested.

Guys, Need you help to identify the loopholes in my analysis for Hindustan Copper.

Above posts talks about Revenue targets of 5,000 Crore by 2020. I will take that as baseline.

Now to achieve this revenue they are planning a QIP and maybe some equity dilution happens next year as well depending on the need.

Overall lets take 5 % dilution overall till 2020. Which makes total umber of shares around 97 Crore.

Currently their net profit margin is between 5 to 7 %. Lets say by 2020 due to economics of scale they expand their margins and achieve 15 %.

With above details EPS comes around 7.73. That means currently its trading around 11.5 FY-2020 PE. For a cyclic play IMHO this is just ok.

My Questions:

What the things based on what we are expecting multibagger returns going forward ?

Are we expecting huge increase in copper price from current levels ?

If we have to assume copper prices hovers in current range ( +/- 10 %) , do you still see value in Hindustan Copper for next 3–4 years ?

Looking forward to hear from you.

Disc : Tracking position in Hindustan Copper.

I really dont understand how on earth HIND Copper is undervalued??? It has to generate 6 times of its current profits at-least to say that it is fairly valued. To me its a complete avoid as i can see many better valued bets in market now.

7 Likes