I really dont understand how on earth HIND Copper is undervalued??? It has to generate 6 times of its current profits at-least to say that it is fairly valued. To me its a complete avoid as i can see many better valued bets in market now.

@Mayank_Narula Simply stating the notes from books is not enough dude. It wont apply for every cyclical company on earth?

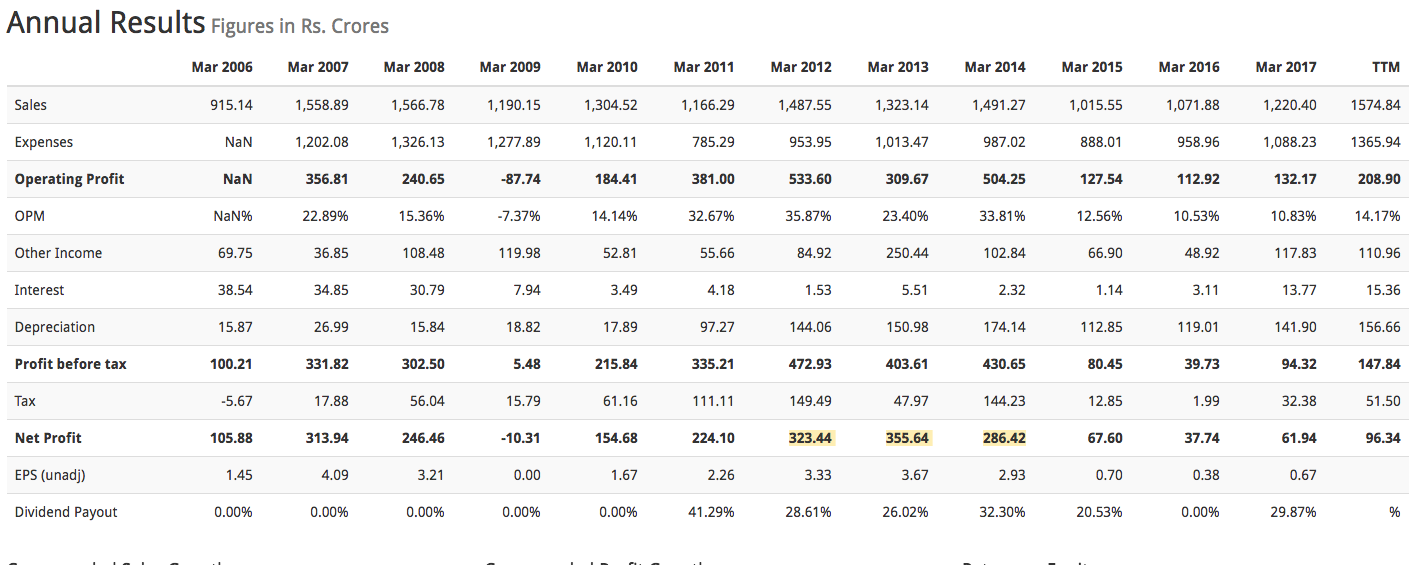

Commodity companies are not valued on P/E basis or an asset valuation basis ( else selan would be trading at-least 10 times of its current market cap). They are valued on the future earnings potential, survival of bad cycle without deteriorating their balance sheet much and cash-flow generation ability. Hind copper have had a bad past even in the past commodity run. Look at their past maximum profits generated or their operating margins. Max. they had 35.87% operating margin. Even if i take that Hind copper is able to triple its revenues in the next two years and able to generate the operating margin at their past peak value of 35.87%, they will still make operating profit of just 1600-1650 which upon removing tax, depreciation and interest costs (assuming no increase in any of these, though in reality its not possible) they will be able to make a profit of 1000-1100 crores which means it is already trading at 8.5-9 times 2 years projected earnings which is not at all cheap in any means for a commodity company.

I strongly believe in the concept of business potential and not just on numbers. So my question to the folks who are gung ho on this is … What changes have the company taken to triple its revenues and increase their opm in the next two years? No one gives any reason … Just simply says copper is in huge demand, futuristic etc. I say buddy its already factored in CMP ( No value at cmp ). These are the companies that we should buy when we see value in them. Even HEG is trading at 80-100 PE so what? It is clearly evident of their future earnings capability and so it does deserve to command this valuation. But what makes HIND Copper a value buy at cmp? To me it is clearly a value trap. At max it can double in three years based on fundamentals. Even if it goes high without generating much numbers simply based these words of future future outlook , it will eventually come hands down.

http://www.screener.in/company/HINDCOPPER/

And the last question to you … what makes u believe it is a multibaggger? Please don’t give the screenshot of Peter Lynch’s page.But give your points that made u buy this.

12 Likes

Well I am not an investor in Hindustan Copper. That was just to corroborate with the thought process of a lot of people here. Investing is not an exact science to clearly forecast the earnings of a company three years down the line. Reasons cited by you may not be good enough to invest in the company, but for other people may be that much is sufficient. I see a lot of linear thinking in your thought process, whereas in reality it may or may not be the case. Besides, nobody is recommending on this forum to buy or sell any stock. We all are here to learn from other people. 100% returns may not be good enough for you, but it can provide enough margin of safety to other people to take a calculated punt.

8 Likes

With QIP not sure what will happen to price in short term

I am a novice but here are a few words.

I agree with you 100% on the run-up that the stock has got despite a poor past performance, but i believe this copper is the buzzword and the EV craze will drive people to buy this stock without looking at the facts. thus from a short term perspective of 1-2 years, it could give a good return, if not a great one…thus, invested a very small amount in this!

How long can we expect this commodity price up moves? Any good commodity stocks with triggers available at reasonable price?

Agree with your points… My 100% returns involved lot of if’s and but’s which are not clear to the market. Regarding recommending the script -> yes, i agree nobody is doing that. But our comments here do make an impact for gullible investors to take a hasty decision and so i tend to be careful on what i write here. To me, still i have never come across any solid rationale from anyone except for saying copper is future and they have lot of assets.

1 Like

If you are betting on EV, then aluminium looks a better bet than copper. It is used more over there.

@jitenp What is your current view on Copper cycle ? Is there much upside left and where in the cycle we might be in ?

Disc: I have a small position on Hind Copper at higher price than CMP taken for learning commodity and cyclical play as an experiment.

Structurally copper is a good bet. I am Long on copper prices. We need to see what grade and strike length, mine addition comes in for hindcopper. With PSu there is always an overhanging risk of capital allocation and govt pressure. This is the reason I am holding tracking quantity of hindcopper. But I see more potential in a private player like Vedanta which could benefit as long as debt is manageable. EV demand is going to keep copper demand intact for many decades unless new supply comes in. Copper mines are far and few. Hindcopper is a fully integrated player with own mines. It can have monopoly in India provided supply constraints from other sources. Private players import concentrate from overseas and refine it locally.

Dont go overboard with the copper theme. Keep a tracking quantity based on your appetite. My allocation to Vedanta is more than tracking quantity. Valuations is based on EV/tonne and copper prices assumptions. The hard bit is to make copper prices guesses over 2-5-10 years.

5 Likes

Vedanta results hit by input cost and raw material inflation. Still managed to do okay.

Commodities - Quarter se Quarter tak

When price realisation are good then top line does well and input cost inflation hits the bottom line.

When price realisation is bad then top line takes a hit and bottom line does better due to falling input cost.

Doubling of current capacity from 1.75mpta

CS on Vedanta. Target raised to 395… I see blue sky for Metals. This rally should go unabated. Short term pessimism is an opportunity to accumulate.

CLSA on Vedanta . Target 422.

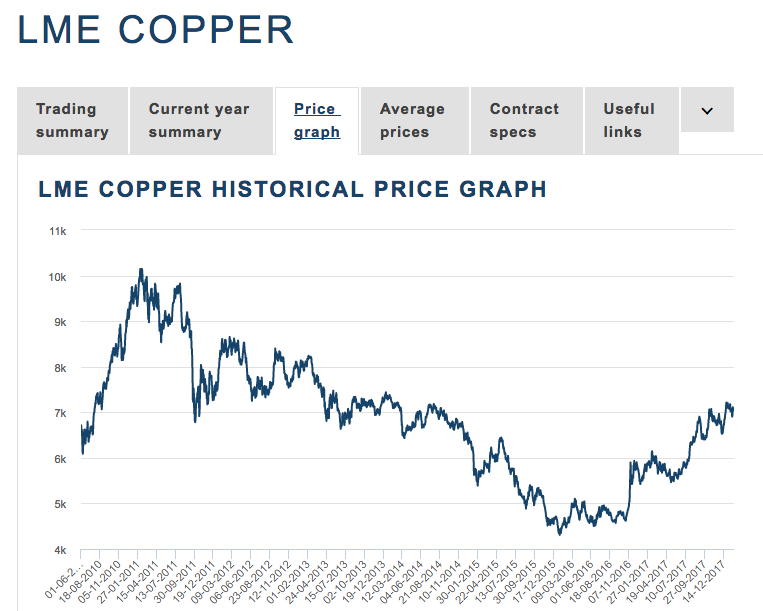

Hind Copper bet is actually a very simple one. Its almost a direct bet on Copper price. This is the graph for LME Copper from 2010 to present.

As you can see prices were good (but declining) between 2010-2014. The same can be seen reflecting in bottomline and margins for hind copper.

The best results were between the same periods (FY12-FY14). You can see the drastic decline between FY15-FY17.

Now coming to the present, the price is on the cusp of where it was between FY14 and FY15 and has been trending up. From here on, any rise in Copper prices will reflect on Hind Copper’s bottomline to a great extent as it did between FY14-FY12. OPM over 30% (almost 35%) from the current 10% levels. TTM OPM is already around 14%.

This is essentially the bet and it in its entirety depends on a synchronised global growth for the next few years. Copper is sort of a direct indicator of growth.

Looks like the results are out for the previous quarter as well. One thing is curious - “Cost of materials consumed” is up 50% both YoY and QoQ. I presume this is essentially energy and probably mostly Crude. So Crude staying low during the copper cycle trending up would clearly benefit Hind Copper disproportionately. If they can land in a sweet spot with volumes when all this happens, we could have the perfect lollapalooza effect. Its too early because there are a lot of assumptions we are relying on.

- Copper prices trending up - Without this, there is no story here.

- Capacity ramp-up in time to benefit from the higher prices (Peak capacity will coincide with peak prices perhaps)

- Crude staying low - Under $70 preferably. Anything under $60 will disproportionately benefit the EBIT by lowering expenses.

- You can only lead a horse to the water.

14 Likes

Thank you for great notes @phreakv6 . Would you please provide the source for LME copper price if one needs to track ?

Thank you @onlish2014 for giving link to track copper prices . I get TableAndGraphErrorMessage on graph ploting as of now in this page. Hope it will get corrected and temporary glitch in the website.

On Hind Copper, I had previously said that after run-up it is not cheap, even after factoring for increase in capacity. In fact, I had booked profits in 25% quantity at avg 98 levels.

This company enjoys a TINA (there is no alternative) factor. Valuation-wise may always have some premium. How much, each one decides on his own.

As far as copper, and in general metals go, I think we are in an upcycle, is what I believe.

10 Likes

any view on LEAD…lead prices at new multiyear HIGH of 169.65 per Kg today…pondy nile worth a look>any one tracking lead stocks.Thanks

2 Likes

Booked all positions in Hind Copper. To buy something else, where I have much more valuation comfort. Purely a rationalization move.