This stock has quite a bit of margin of safety both from a price and quality of business perspective. It is one of 40 companies in the world which have been profitable for over 100 years. Nick Sleep, the famed value investor, always wanted to invest in organisations which have demonstrated this longevity e.g. London Stock Exchange, and has a theis around this. Orgs viz. CUB have deep, innate knowledge of customers, markets, cycles etc which they use the old school way of running business these can never be replaced by Large Language models (AI) etc. Aditya Puri was an old master of doing banking the old way and compounded business at the rate of 18-20%. CUB in my assesment has been very forthright about the RBI observations and change of RBI position regards interpretations of their circulars. This rising tide should be used by banks to clean up their books and confirm to guidelines - will hold good during a rainy day.

Interesting news today of INR 100 crs paid back by Spice Jet to CUB. This transaction was executed by CUB in 2012 when Maran’s were owners of Spice Jet. This puts curtains to perhaps the largest trade done by CUB and gone awry. However, it now has ended well for CUB. There would be reversals of the provisions on the transaction. The key is to observe if all the provisions would be reversed by CUB or they would be used for Agri subvention mismatch or “future provisions” provisions created.

In my considered assessment, this transactions gives CUB a rare confidence booster in playing “not so big boys” game. Do they capitalise on this - only time will tell;

Wonderful data …Expenses which are controllable are stable ( good sign)…being conservative is basic requirement for a bank and CUB is steadfast on the same…restructuring record during lehman is comforting…past is a great indicator for the future performance especially in case of banks…anyways they are gradually making an attempt to get into other areas like retail etc that too in a conservative way ( max 15% loan book in 5 years)…fee income avenues shall rise plus casa also may raise as the suite of retail products increase…using tech to reduce TAT is also great as it improves the processing capacity efficiency…Risks being new CEO selection , track record says that CUB is always good at recruiting CEOs from internal candidates ( very less CEOs in its entire history)…so if the CEO is from outside then it shall be untested waters…

One more important factor to look out considering current loan book mix is - NPAs and their write off percentages - CUB claims that 3% shall be NPAs and only 30% is lost as writeoffs…as long as this holds, I think rest all shall be taken care as time passes…growth is not a concern as there shall always be demand for loans ( its understandable that growth shall not be linear unlike biggies like HDFC etc considering the higher percentage of MSME focus whose business has a factor of lumpiness)…As inflation grows , the working capital requirement for MSMEs should rise as the amount that gets blocked in inventories / debtors etc shall rise…despite inflation if these working capital loans are not increasing , that could have multiple reasons depending upon the nature of business. Other factors could be loss of customers to other competitors. If the competitors are just fintechs / some one who dont understand the lumpines of MSME business prospects, they shall be driven away with time…if competitor is some one who truly understands the nature of these MSME businesses, there there is a prospect of long term loss of market share…anyways with the digitisation and TAT reduction focus, this threat can be somewhat mitigated…Increasing retail focus which CUB is pursuing if successful shall be real game changer as CASA rises as suite of retail products rise leading to low cost of funds which is the ultimate moat in a commodity business like lending…

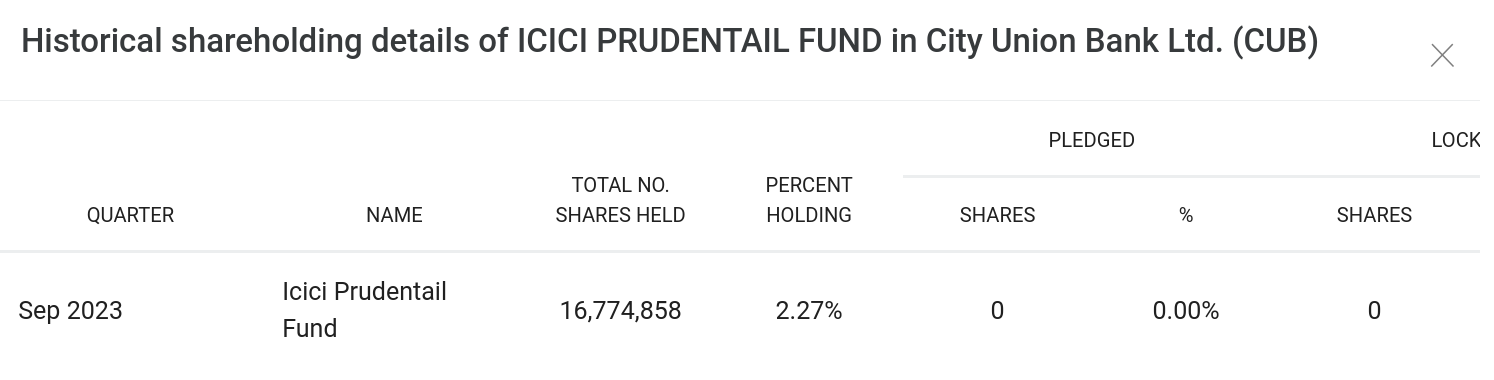

its regular investments by HDFC AMC; as per RBI regulations, any one who wants to increase holdings in a bank beyond 5% needs to get it approved by RBI first.

An excellent earnings call with Dr. Kamakodi, CEO of City Union Bank. Always great to listen to him though it was an average quarter for CUB. Thoughtful and clear presentation and answers. https://www.youtube.com/watch?v=y85PIlDDRiw.

A few takeaways:

Q3 - Slower growth (deposits up 5% and advances up only 2%) but expected to improve. FY24 growth guidance lowered to below 10% from 12-14% earlier. ROA at 1.49% in Q3 FY24 (vs 1.69% in Q2 FY24 and long term avg of 1.5%). Net NPA and GNPA are lower, provisions lower. NPA recoveries are better than slippages. Cost-to-income ratio at elevated levels (48%+) due to automation investments (with BCG), to be higher for two more quarters. NIM and Net Interest income lower with cost of funds higher. One-off FITL (Funded Interest Term Loan) impact in Q3 on NIM - portion of unserviced interest income reversed due to restructuring during Covid period. PAT for FY24 expected to cross 1000 crores for first time ever. Growth triggers for Q4: Unwinding of KCC book (gold loan degrowth of 4000 crore) is over - some growth will possibly come from there (once the product is restarted), automated lending will support some growth (first phase over, sanctions for <3 crore loans can be done within 48 hours. 2nd phase for <5 crore loans expected in Q4, 3rd phase for <7.5 crores loans after that. Also supporting better measurement of probability of default, increases capacity to process more loan applications). 8-9% growth in Q4 maybe optimistic. Deposit growth target - to match credit growth, no challenge with raising deposits if required. Want to increase RoEs back to 15% as before. Asset quality levers have helped PAT growth and keeping credit costs lower. Benefit of this visible for a few more quarters. SMA2 numbers are almost lowest ever (2.38%). Insignificant impact of TN floods - a few operational issues in branches. Does not expect any material impact due to the floods. Bond yields have softened but not enough. If yields soften further (he didn’t seem positive it would), some profit booking opportunity will be there. Credit demand areas - MSME borrowers for solar energy, capacity expansion needs (better, but not great). Textile export sector - some sluggishness. Credit proposal requests are getting back to pre-covid levels. He didn’t sound gung-ho though about overall credit demand, cautious optimism as the TV analysts would say.

Is it a good bet to place on CUB now as they are continuously improving their NPA and their NIM is also getting somewhat better and it is undervalued compared to its peers. Their future plan is also good .

I believe CUB is a good bet. Their Asset quality is the only problem few quarters ago and now that is trending well. System Implementation is going well and they are all set to grow lapn nook in FY25. I expect them to cross 200 levels within FY25.

I am invested, and I believe there is reasonable margin of safety at this level. It’s a well run bank, but traditionally conservative. There is geographic concentration risk given 50-60% (if not more) of their branches are in TN. They are trying to cautiously increase retail lending besides the technology improvements for faster MSME loan approvals. They are also slowly adding branches in a few other states. We have to see how well they execute across these areas. MSMEs/traders (who are their main customers) are still not borrowing much, but I think we are past the worst there and it should improve. If lucky, it can improve fast, but even otherwise, we should see steady growth. From a broader macro perspective, given the high level of personal loans in the system, I am currently more comfortable with conservative lenders like CUB who do not have such exposure and with the larger private banks.

They have taken higher provisions (at least partly to boost their PCR, it seems like) which has impacted profitability. But other than the increasing cost of deposits (which every bank is struggling with), most of the other metrics seem quite fine. They have maintained NIMs, strong growth in fee income, good growth in advances, CASA hasn’t gone down (not much anyway), and an unexpected slight improvement to their cost-to-income ratio for some reason.

The stock’s not done much and it’s been on a downtrend of late. But I like these results. Not fantastic, but in the current environment, it seems quite good. Not sure if I am missing something. Any additional thoughts would be welcome!