How many of you see value unlocking in this special situation ?

The restructuring scheme includes amalgamation of CESC Infrastructure, Spencers Retail and Music World Retail with CESC; demerger of power generation undertaking to Haldia Energy; demerger of retail undertaking I (as defined in the scheme) of the company and retail undertaking 2 (as defined in the scheme) of Spencers Retail to RP-SG Retail. Further, the scheme includes demerger of IT undertaking of the company to RP-SG Business Process Services.

As per the scheme, Spen Liq will be amalgamated with RP-SG Business Process Services and New Rising Promoters will be amalgamated with Crescent Power.

The scheme includes reduction and cancellation of the existing share capital of Haldia Energy, RP-SG Retail and RP-SG Business Process Services. Further, it includes reduction of the face value of the equity share of CESC from Rs 10 per share to Rs 5 per share and subsequent consolidation of two equity shares of the company of Rs 5 each into one equity share of Rs 10 each.

The equity shares of Haldia Energy, RP-SG Retail and RP-SG Business Process Services will be listed on Calcutta Stock Exchange, BSE, and National Stock Exchange of India, post effectiveness of the scheme. The shareholders of the company will get shares in these listed companies in the same proportion as their holding in the company.

Post restructuring, in addition to the IT undertaking, the RP-SG Business Process Services will house various other ventures of the group, inter alia, property, entertainment and fast moving consumer goods business. As part of this alignment investments in/by Guiltfree Industries and Apricot Foods will also be held by RP-SG Business Process Services.

It’s indeed a very complex arrangement of proposed demerger and will needs regulatory approval before it goes through. Any timelines management has given to complete this?

CESC_Q4FY17_Result_Update.pdf (657.4 KB)

Attached analyst report may help to understand it further down to details with corresponding numbers of each of the businesses involved in the demerger process.

It is fully valued at 910 for de merger.

Hello @s11, Do you have breakdown of the valuation.

CESC (ongoing business) Rs 528

Net Cash & Liquid Investments Rs13

Dhariwal 32

Haldia Rs 105

Firstsource Rs 86

Mall Rs10

Spencers Rs 137

My ballpark numbers for the CESC demerger are as follows:

CESC (existing power business) - 12,500 - 16,500 cr. FY 17 PAT of 750 cr x 10% growth assumed for FY18 x 15-20 PE. The distribution company can actually be re-rated at more than 20PE as it is the only listed discom. The genco may be at the 12-15 PE range.

Spencers - 3300 cr. (2200 cr - 4400cr) FY 17 is 2000 cr x 10% growth x 1.5x Price/Sales (1-2x P/S)

CESC Ventures - 1000 cr. 55% of FSL marketcap of 2300 cr is about 1250 cr. Holding co discount of 30% would give about 900 cr. Add another 100 crs for other businesses liek Quest Mall, Real Estate etc

FY18E market cap for me is around 18,000. Current market cap is 13,000 cr.

Disclaimer: I may be wrong and my calculations. I have a vested interest in CESC. I am currently invested.

I agree with your figures however i feel the Spencer valuation at 3300 Crores is a bit on the higher side as Future retail growing at 12% is valued at around 1.2 P/S but if they improve their negative margins and bring it to positive territory,it will be justified

Spencer’s retail is going to be debt free after the demerger.

Can anyone please tell the exact record date for the demerger?

It has not yet been announced. We will have to wait for official announcement from the company.

ok. Thanks for that. 01-Oct-17 was supposed to be arrangement date subject to some approval.

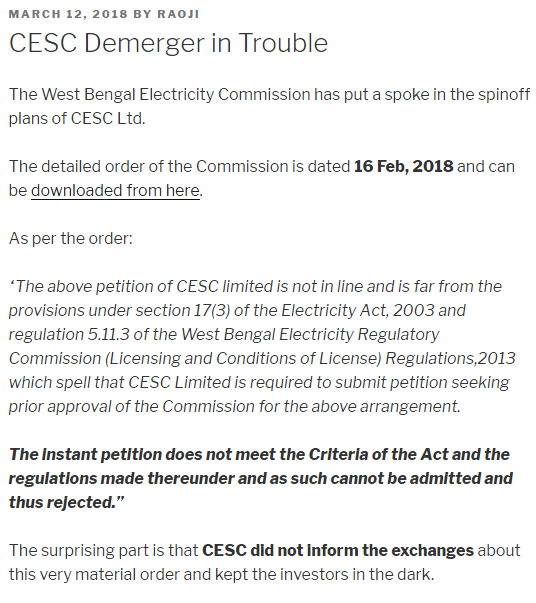

An interesting article on CESC Demerger.

The data related to net profit is wrong… we should consider profit attributable to owners of the company part only, which is 1004 cr vs 691 cr. EPS data is alright.

Any reason why recent fall ? on CESC.?..just normal market reaction

Please help if you have some info

Latest article on CESC Demerger

Based on the sum of part valuation, total value of the four businesses comes to Rs 1,325 per share. On Tuesday, CESC’s stock closed at Rs 876 on BSE. At this price, the stock is trading at one time price to book value and analysts expect it to touch 1.3 to 1.4 times close to the demerger.

Read more at:

//economictimes.indiatimes.com/articleshow/64864982.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

While this delay in fructifying demerger scheme of CESC (announced 16 months back) may have tested the patience of few market players, it does offer necessary time for folks like us to understand /extrapolate valuation matrix and then take a call. Thought it was good time to revisit the valuation hypothesis

-

Power Generation: More of an annuity business. Can be valued around Rs.6500 cr (10 times normalized Profit of around Rs.650 cr)

-

Power Transmission - P/E of around 14-15 times will give around 9000-9500 cr of valuation. (considering scarcity premium)

-

Spencer- 1.5 times sales will value this business at Rs.3000 cr

-

CESC Ventures-

(a) First Source (55% stake): Around Rs.1500 cr (40 % Discount to Current Market Cap ).

(b) Mall- Around Rs.150 cr being 0.5 times BV

© FMCG - While management has targeted revenue of Rs.500 cr for FY 19, better to ignore the same for valuation purpose time being.

All these add up to estimated valuation of around Rs.20,000 cr post listing of all entities vs present market cap of around Rs.12500 cr. Have assumed listing by FY 19.

While someone might argue whats the big deal, I agree it is not. However in such uncertain volatile times (leading into elections etc) such special situation (value unlocking) themes (not only CESC) does give me some valuation comfort.

Key Risks: Further Regulatory delay, adverse market condition at the time of listing.

Views invited.

Note: Above estimate is subject to error and biases. It may or may not materialise.

Discl: Invested (>5% of portfolio). May add/exit any point of time.

@1.5cr Experience teaches us that there will always be some uncertainty here or there. Investment decions are to be made without knowing all the facts / complete picture. It is because of the uncertainty regarding approval , market has not yet re rated the stock. Delay or uncertainty like these present opportunity for persons like me who believe in d story/ theme ,to add on.

Thanks.