Target to maintain 16-17% EBITDA margin in current fiscal

The company has conducted a conference call on 14 July 2016 to discuss the financial performance for the first quarter ended June 2016 and way forward. Mr Bharat Mody, strategic advisor of the company addressed the conference call.

Key highlights

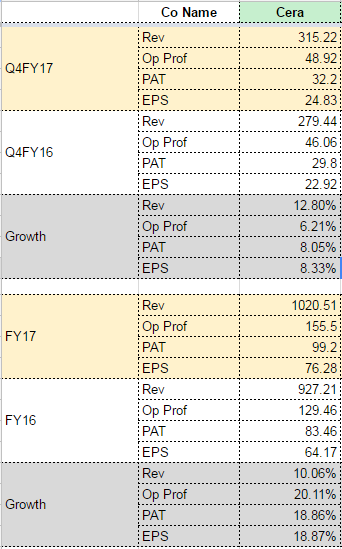

Bathroom products maker Cera Sanitaryware has reported a 36.59 per cent increase in standalone net profit at Rs 21.39 crore for the quarter ended June. Its standalone net sales rose 12.18 per cent to Rs 223.94 crore during the quarter under review.

The Company registered a growth of ~12% (volume and value together) in Q1FY17. The Company clocked ~ 50% of business from sanitary ware division and ~13% from allied products which used with sanitary ware, ~3% from faucets, 14% from tiles and rest is from wellness range of products. On segment wise sales growth, sanitary ware division registered a growth of 12.85%, faucets at 9.35%, and tiles at ~19%.

The Company plans to maintain advertisement expense of 4-4.5% of topline.

The Company revenue guides to maintain same growth this year for current fiscal. The company guides EBITDA margin at around 16-17% in current fiscal.

The Company joint venture with Anjani Tiles (manufacturer of high-quality ceramic vitrified tiles in Andhra Pradesh)has started commercial production from April 2016. It’s reached a capacity utilisation of 90% in June. The Company expects the turnover of ~Rs 95-100 crore from Anjani Tiles in current fiscal.

The company expects demand growth comes for government affordable housing scheme, higher disposable income in the hands of both urban and rural population on account of good monsoons, smart cities, and the implementation of the 7th Pay Commission.

Just a correction - The Company clocked ~50% of business from sanitary ware division and ~13% from allied products which used with sanitary ware, ~20%from faucets, ~14% from tiles and the rest (~3%) is from lifestyle/wellness products.

In my view, Cera has been performing well in the current subdued market and with a pickup in demand, it can grow more than 20%.

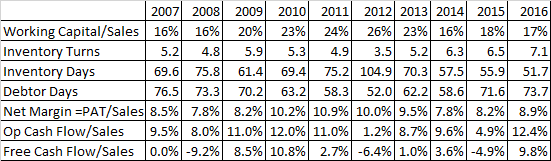

Good observation. They also appears to have increased proportion of consignment sales as receivables (as a % of sales) have been going up for last 3 years and now days sales outstanding is also much higher than Kajaria. All this points to difficulty in pushing sales. Not a good development considering sales growth is the main reason why anyone should buy this company.

● Revenue increased 10.6% y-o-y and 16.7% q-o-q to ₹2,492 mn.

● EBITDA margin expanded by 364 bps y-o-y to 16.6%, as power and fuel cost as a percentage of sales contracted by 175 bps y-o-y and raw material cost as a percentage of sales contracted by 112 bps y-o-y.

● Adjusted PAT increased 40.6% y-o-y to ₹251 mn

● Inventory and debtor days reduced to 51 and 65 days respectively, from 55 and 78 days in H2FY16 (both calculated as per TTM basis).

Q2 Conf Call Highlights: CSL to grow 12.5%-15% this year

CSL reported a 40.6% growth in standalone net profit at Rs 25.14 crore for the second quarter (Q2) of financial year

2016-17, up from Rs 17.88 crore in the corresponding period last year.

Net sales income of Rs 260.98 crore in July-September this year, up 12.5% from Rs 231.98 crore in Q2 during 2015-16.

The Company registered a growth of ~12.5% (volume and value together) in Q2FY17. The Company clocked ~ 60% of business from sanitary ware division and ~12% from allied products which used with sanitary ware comprises of PVC Seat Covers, PVC cisterns and some of the fittings which essentially go with the sanitary ware, ~10% from faucets, 15% from tiles and rest 3% is from wellness range of products such as bathroom cubicles, bathroom partitions, Shower panels etc.

*** On segment wise sales growth, sanitary ware division registered a growth of ~8%, faucets at ~12%, and tiles at ~37%.**

The Company earned about 40% business coming from a mass market. The Mid Level - is divided into Upper - Upper and Upper - Lower continued to contribute above 20% business. The Upper - Lower was at ~21%. However the Upper - Upper increased to ~25% where the Company have much better realization, so as the premium market that the Company hold about 14%, 15% presence.

The Company has around 15000 distributors now and aim to add further at least 30% in next three to five years so to reach around 20000.

The company guides to achieve a growth of 12.5%-15% in the current fiscal. The company guides EBITDA margin at around 16-17% in current fiscal.

The current utilization of capacity of Sanitaryware is around ~98% and that of Faucet ware almost about 62%.

The Company hopes to reach to utilize this capacity of Faucet ware to around 80%+ to 90% by the end of the year FY 2017. The Company planned raising manufacturing capacity on Sanitaryware from 3.2 million to 3.3 million.

The company expects with encouraging Govt. policies on housing, more on affordable housing range, and with a good monsoon demand are signalling steadily upward trend in time to come.

I think Cera will get badly hurt because of recent demonetisation of currency. Real estate slow down in short and medium term could adversely impact Cera. The stock price of Cera has massively cracked in last few trading sessions post the news.

This might help in demand pickup if implemented timely…

Prime Minister Modi formally launched ‘Housing for All’ in rural areas under which the government proposes to provide an environmentally safe and secure ‘pucca’ house to every rural household by 2022. In its first phase of the PMAY (Gramin), the target is to complete one crore houses by March 2019. The unit cost for these houses has been significantly increased and now through convergence a minimum support of nearly Rs. 1.5-1.6 lakh to a household is available. There is also a provision of bank loans up to Rs. 70,000, if the beneficiary so desires. The selection of beneficiaries has been through a completely transparent process using the Socio Economic Census 2011 data and validating it through the gram sabha.

Also, one point to consider is the slowdown in real estate will be from premium segment where I think Cera was used much more. The low cost housing with small ticket size under “Housing for all” are less likely to use premium sanitaryware like Cera. Let’s hope for the best though. But surely there are now more variables and ifs n buts that has come off-late.

Cera is actually a middle of the market brand, aspiring to have some market share in the premium segment. With GST implementation also coming in, there is a strong possibility of value migration from small unorganised players to the organised sector.

I am new to investing, however, what concerns me about CERA is the huge build up of current assets i.e inventory and receivables, which together amount to 320 Crores. This pushes up the working capital, when viewed along with the increase in debtor days. Is this normal? Isn’t this an inherent inefficiency in how things are run. Again the cash flows are not impressive, when compared with PAT. I have limited sector knowledge and I was hoping someone could provide some insights and commentaries on these figures.

Based on the latest announcement from the co on the exchanges, HDFC Standard Life now owns more than 5% of the co. The last tranche of shares were added on 30-Mar-2017. Hopefully a good development to have strong long term investors owning large chunks of stock.

Fairly muted results from Cera. Post-demon effect probably came through this quarter. Going forward, things might look up with thrust on low cost housing and RERA in play.

Only Q- for affordable housing play, why Developers will select products from Cera whose products are not in the value for money category. Please correct me I am wrong.

Cera’s perception is on premium play. For 25L or say 30L house, will developers put in Cera products in India?

Could you please explain why RERA would be a positive? I talked to a few friends in the real estate industry who were mentioning that RERA could be negative for business over the next year or so.

With RERA, there would be mandatory disclosure of project details, including those of the promoter, project, land status and clearances. This would increase the credibility of developers and would protect consumer rights as well.