RERA, in my opinion, is short term doubtful, but long term very good for the real estate sector, provided the states enact the real estate sector regulator correctly. This sector can be a very good employment and GDP growth provider for a long time, if the reform works out… similar to bringing in SEBI in capital markets.

5 Likes

Cera was doing a time correction for last two and half years years and is now looking like starting next upward journey. Its sustaining above 2900 area which was 2015 high. The results were not so encouraging for June 2016 quarter in terms of profitability. But considering that technical move is quite strong and there is two year under performance behind, the scrips looks intersting.

1 Like

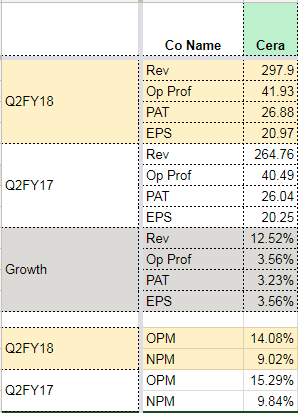

Q2 results:

Hi Sir,

Got this from the exchange filing:

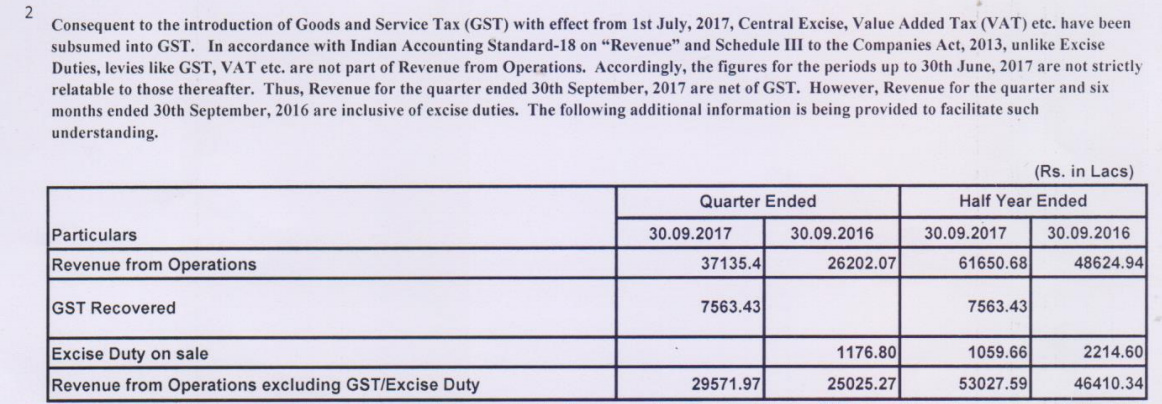

In the light of the above can the revenue growth be considered at 15% ?

Also would love to know your view on this result?

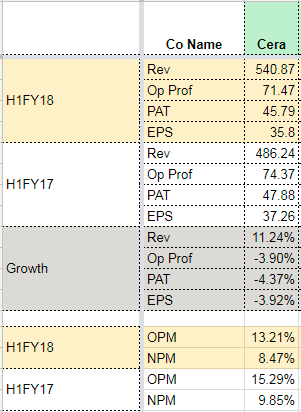

This is the problem for all companies. So, for a like-to-like comparison, it makes sense to compare without GST/Excise. However, that does not change the PAT or EPS, so decent results, but not great.

For companies such as these which depend heavily on the distribution channel, direct discounts / commissions / brokerage should be netted off from sales revenue to understand true sales growth. Often, I have found real sales growth to be much lower when done this.

2 Likes

Thats a good point. I saw pretty much the same in most of the companies. Small sales growth adjusted for GST. but flat eps growth. And everyone is calling it a very good result.

Other thing i noticed. In the previous con calls most of the companies were saying GST will help get market share from the unorganized players etc. Now their response, its too early to say…

1 Like

Looking at Govt and their election oriented agenda, GST rates are changing frequently. Also, in Indian culture, unorganized players have more skills to do ‘JUGAD’ to remain in business. I talked to 3-4 unorganized players in Morbi (hub of ceramics), as per them, we don’t face any issue. Our business as usual and some what better than earlier!

Summary of Concall for Q2 (source: Kotak Securities)

- As per the management, real estate demand is still to improve and will continue to affect their institutional business /and that of the industry. Cera believes RERA is likely to reduce launches.

- We believe launches are already down on account of weak demand which eventually impacts the building material industry.

- While existing demand is likely to be distributed across fewer developers, improvement in launches across industry might take 12-18 months (an additional 12-18 months for demand revival of building materials used for MEP). Focus of such players until then has to lean more towards the retail business.

- Cera has spent around

370 mn in 1HFY18 on capex and has guided to900 mn of capex in FY2018. Part of the capex is for improving the product mix at its tiles JV. - Cera has also started manufacturing zinc based handles (used with faucets), a first in India. The management believes this is a value add to their faucets product and also gives a cost advantage versus imports.

- Cera has again pushed the expansion of its sanitaryware plant (0.3 mn pieces /year) to next year.

- Recently (post 2Q), Cera launched a brand ‘Jeet’ to cater to institutional demand for the affordable housing (sub

2.5 mn/unit) segment. Cera will be outsourcing these products and will be350-500 /unit cheaper versus their entry level product range.

4 Likes

NOTES FROM EDELWEISS CONFERENCE - 01-FEB-18

The sanitaryware segment’s growth has been affected due to pressure from unorganised market and management expects growth to remain muted over the next two-three quarters in the absence of e-way bill implementation.

Management expects growth to pick up in CY19. Government’s focus on low-cost housing is unlikely to trigger demand growth for the segment catered to by Cera as the company does not have any product offering in the low-end segment and will cautiously remain away from this segment as management remains focused on medium end and premium end segments.

Over the past two-three years, Cera’s revenue growth was also supported by Parryware losing market share due to management focus on “Roca” brand. The company has plans to launch another brand in premium end segment in sanitaryware to garner market share in the high-end category.

In the faucets market, Cera has a minuscule share (~2%) and continues to focus on driving growth in this segment as it sees huge potential to tap revenue in this category on the back of robust distribution. Though margins in faucets are marginally lower than sanitaryware, due to outsourcing, it adds to return ratios.

In the tiles segment, Cera believes that focusing only on the soluble salt segment was not so favourable and there is a possibility of expanding the product offering in other segments like vitrified tiles. This segment, however, continues to post losses and a recent increase in gas cost is likely to put further pressure on margin. The company also suffers on account of location disadvantage.

Cera will continue with its outsourcing strategy and focus on brand and distribution, which helps the company enjoy higher return ratios. It has capex plans of ~INR2bn over the next three years funded through internal cash flow generation.

4 Likes

Team,

Any observation with regards to the price fall, apart from the E-way bill impact mentioned above in the thread?

Results, Chinese imports, Pricing Pressure. low profit growth.

I am very interested in knowing from one of the senior boarders how they currently view this company after a correction. I am talking in reference to the art of valuation thread where several boarders look to identify how they would exit a company(book partial profits or exit completely) and what would make them reenter after a steep correction. I think Cera’s example would be a good one to take up since a lot of senior boarders have had it in their portfolio since long. Have any of the boarders who made decent returns on this stock bought more during this recent correction??

regards

I bought into Cera after the correction (I didn’t have it before, though). I think the 35%+ correction is quite justified, but perhaps a little overdone. I think the correction happened due to a combination of factors like overvaluation, industry headwinds and RM price increase. A triple-whammy, if you will. But that’s precisely why you get such good stocks at a discount. Good investing, in my opinion, always comes with an initial discomfort. If you’re investing in a stock and thinking “I’m very comfortable investing in this”, then you’re probably not going to earn much out of it.

I do not know when Cera’s headwinds will go away. I’m not clairvoyant. But I think the current prices provides enough Margin of Safety for a short term discomfort and a long-term reversion to mean.

2 Likes

Asking a theoretical question.

It is believed that over the long term, the growth in share price mimics the growth in EPS.

In corollary, if the share price growth is < EPS growth, then an increase in share price is likely. And V.V.

In case of CERA, a great company with RoCE > 20% and low debt, has grown EPS @ 25% CAGR… Whereas, share price has grown 38% CAGR (2008 to 2018)

Based on this can one view this stock as still somewhat overbought, inspite of the recent 38%correction

1 Like

Theoretically, there are other factors affecting share prices in the long run.

There is PE expansion and PE contraction that plays out. This expansion or contraction is based on forward expectations.

In the long run, I believe that, Share price can not grow if EPS does not grow… Rate of growth in share price can be higher or lower depending on forward expectations.

It may not hold true. If there is expansion in EPS, but share price is not increasing at a same pace, that means forward expectations are low and share price is adjusting to those levels. It may also not hold in case of value traps, commodity companies etc.

This factor can not determine that the company is overbought or not. It was a relatively unknown company before. If you see 2000 to 2018, the disparity will even be larger. There are numerous factors that have changed since - More brand visibility, management quality has been proven, new products (tiles, JEET - affordable brand, packaging division), increase in capacity, proper capacity utilisation, inhouse technology (cera has very good in house research), sanitaryware/faucets (taps and fittings), kitchen sinks, mirrors and other accessories, isvea italia (Premium / Italian range of sanitaryware) etc.

So, I feel that company’s share price has improved faster than EPS due to company specific factors. However, to invest at current prices, one need to take a view of future outlook. If my expectation is that the company can continue to perform as it was doing before, it may be a good buy… however, bears can say, there is more competition (kerovit by kajaria, even Jaquar is coming.)

Disc: Invested

3 Likes

In Cera… following are the points of concern

-

YoY DSO appears to be increasing, not at an alarming rate, but increasing nonetheless. Trade Receivables is increasing at a faster pace than the Sales.

-

YoY FCF is lessening.

-

Sales Growth has slowed down. Slowest in last four years.

The point I am trying to make is that there isnt reason enough for one to expect a PE expansion in Cera, except the general exuberance in the market, considering that Nifty is trading at PE 25, whereas the average PE is around 17.

1 Like

Yoy sales may not be the right number. Previous year figures were inclusive of Excise whereas as per IND AS current year figures are exclusive of GST.

FCF has decreased due to investments in Tiles, faucets, jeet brand etc. These are all new business company has started in past 1-2 years.

I believe they will pay off in long term and FCFs will return to normal levels as these new ventures take off.

1 Like

An important aspect is I think the competitive dynamics has started to change in the industry. Today, if one sees, all ceramics players are getting into sanitaryware and all sanitaryware players are getting into tiles. Kajaria has come out with Kerovit, Somany ceramics has a new line. Asian Paints has also recently got into the game. Add to that, the fact that gas prices have not really been very supportive. These are not short term challenges. These are long term trend changing factors.

Short term challenges like the ones mentioned above are also there:

- Slump in real estate sector

- Overvaluation combined with lack of growth continues

Disclosure: I have been invested in Cera for over a decade. Sold entirely sometime back. Having said that, I could be wrong in selling and may buy back if the facts change.

6 Likes

Agreed completely that sector competition has increased multifold. I work in real estate sector and handle purchase side of the company. Currently we have got quatation from Cera , Kerovit, jaquar, American standard , Roca, Grohe & hands Grohe. Competition has increased mutlifold in sanitary and bath fitting and buyer powers has increased ,both Indian and international brands are competing for the same market. Observing same trend in tiles.

1 Like